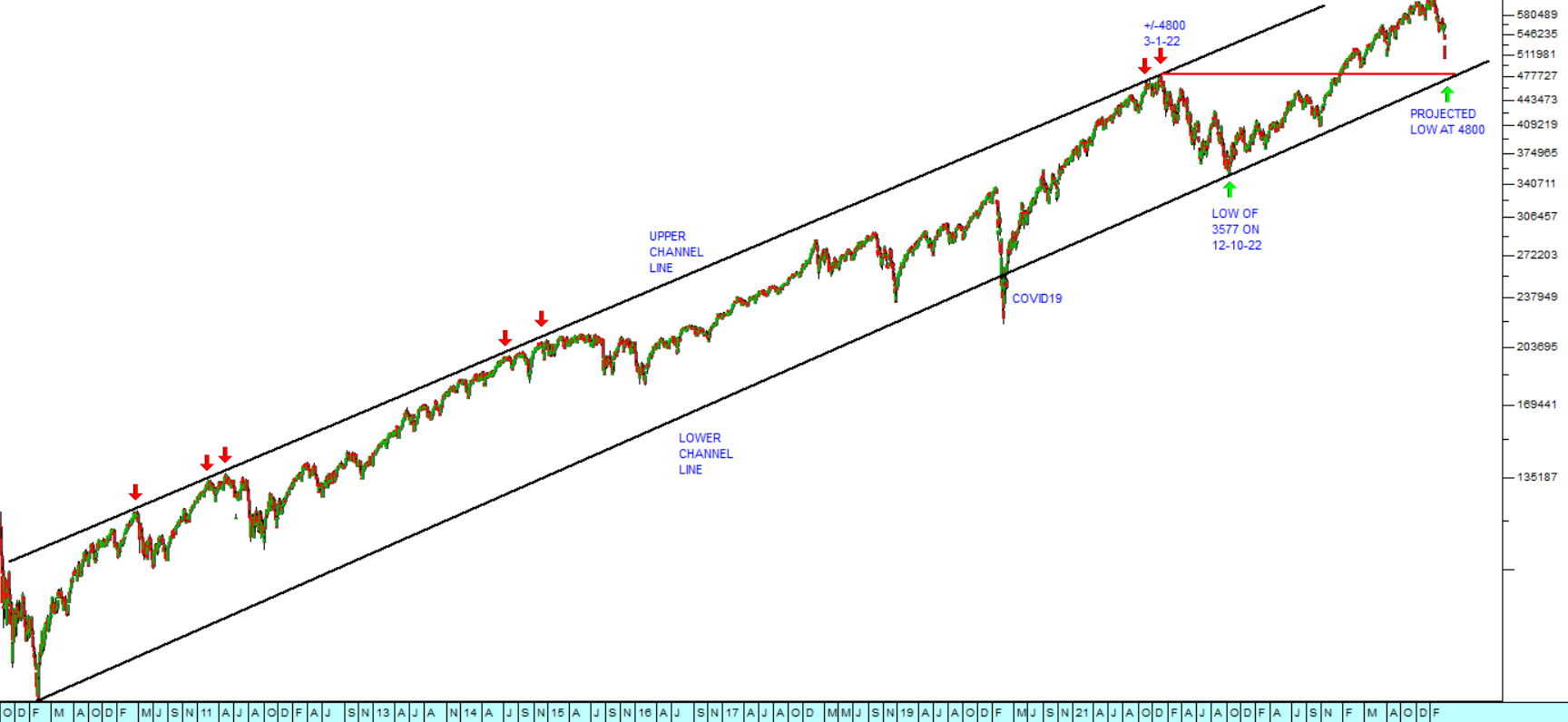

The Economy

19 June 2019 By PDSNETThe state of the economy of the country obviously impacts on share prices over time. In this regard, private investors need to consider five inter-linked variables – the inflation rate, the level of interest rates, the money supply, the balance of payments (BOP) and the business cycle. These five factors are alternately impacted by and impact on the strength of the rand against other currencies and especially the US dollar. The monetary policy committee (MPC) of the South African Reserve Bank (SARB) meets every two months to adjust monetary policy and especially the level of interest rates to balance its two opposing objectives of price stability and economic growth. The level of interest rates is alternately increased or decreased to stimulate the economy or reduce inflation. So the MPC is always either putting its foot on the accelerator (dovish policy) or the brake (hawkish policy). But monetary policy can generally only have a mild impact on the economy over a period of months. It cannot overcome the type of structural problems which are besetting the South African economy. Those structural problems are really three-fold:

- The civil service, including the state owned enterprises (SOEs) and municipalities, is far too large, corrupt and very inefficient. This has led to a massive and growing wage bill which this country can no longer afford. It also causes endless bureaucracy which impedes business at every turn.

- The labour market is too heavily balanced in favour of employees and against employers (i.e. businesses) with the result that employers avoid employing people at all costs leading to high unemployment.

- The level of government indebtedness has become unsustainable – this, of course, includes the debt of municipalities and SOEs. The high debt levels mean that there is now very limited room for programs to provide service delivery or improve infrastructure – which, in turn, is leading to virtually continuous service-delivery protests across the country.

DISCLAIMER

All information and data contained within the PDSnet Articles is for informational purposes only. PDSnet makes no representations as to the accuracy, completeness, suitability, or validity, of any information, and shall not be liable for any errors, omissions, or any losses, injuries, or damages arising from its display or use. Information in the PDSnet Articles are based on the author’s opinion and experience and should not be considered professional financial investment advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional. Thoughts and opinions will also change from time to time as more information is accumulated. PDSnet reserves the right to delete any comment or opinion for any reason.

Share this article: