Kore Revisited

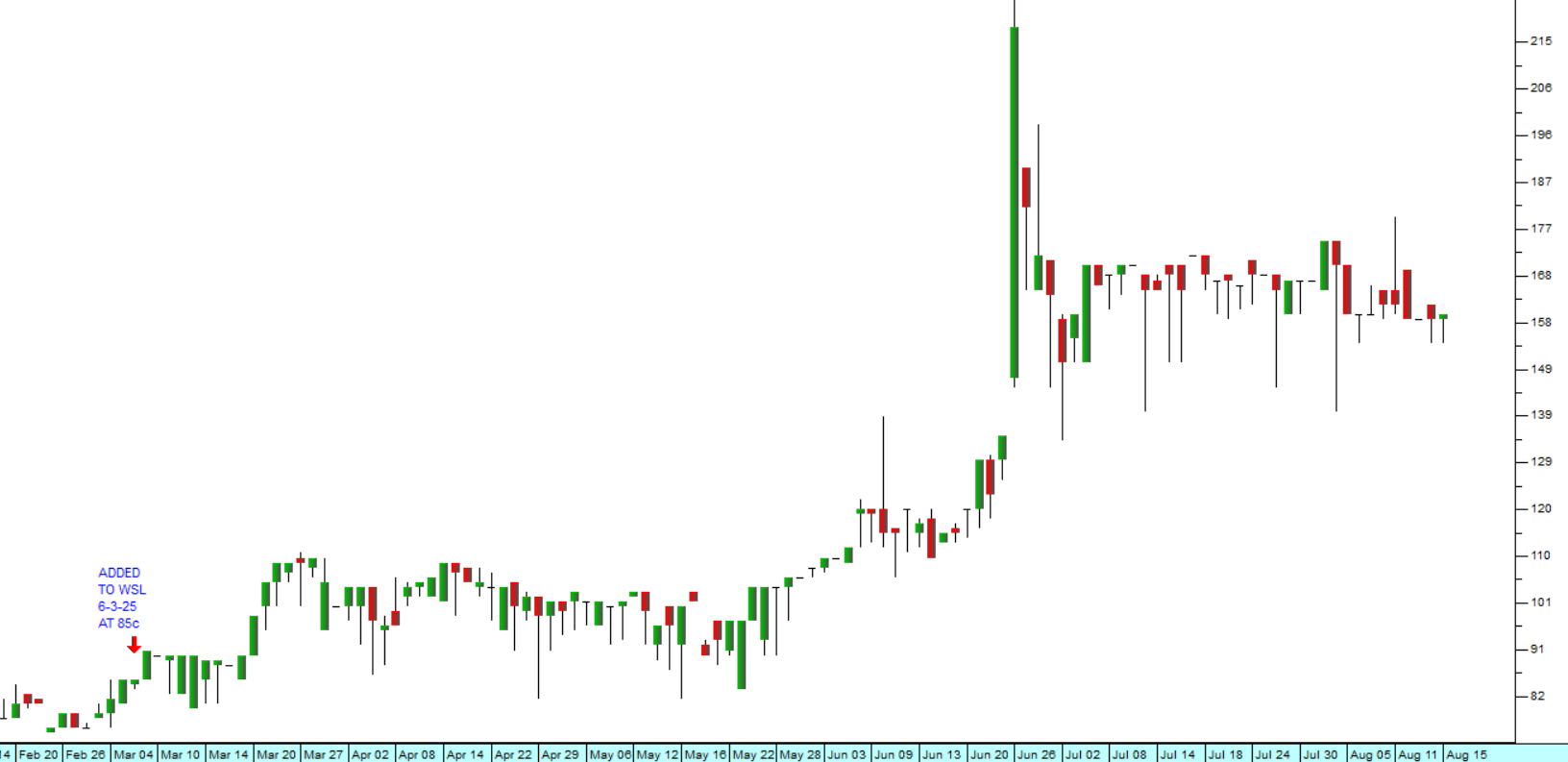

26 May 2025 By PDSNETKore (KP2) remains at once the most exciting and most risky investment on our Winning Shares List (WSL) at the moment. We originally added it to the list just over a year ago on 16th May 2024 at a price of 20c. It subsequently rose to a high of 83c on 3rd October 2024 and we published an article about Kore on 14th October 2024.

Since then, it has been going through a period of profit taking as speculators, who bought the shares when they were below 20c and did not want to wait for the potash project to come to fruition, sought to take profits and so avoid the significant risk which is still a major part of the investment. Consider the chart:

The period of profit-taking came to an abrupt end on 23rd April 2025 when insiders again began buying up loosely-held shares ahead of a cautionary announcement. That announcement came a few days later on 2nd May 2025 and the share has subsequently risen to a new cycle high of 84c (16-5-25).

As indicated in our article, the risk in this share is significant because the mine is located in the Republic of Congo (ROC) and because the mine is only expected to begin construction next year – and that construction is expected to take 43 months so the mine will only begin to produce some time in 2029. Despite this, the potential profitability of the Kola project is compelling.

The mine will cost just over $2bn to build and is expected to produce 2,2m tons of potash per annum over an expected life of 23 years. As indicated in our previous article, the cost of production is expected to be $62 per ton against a price which can be as high as $350 per ton. This makes the mine one of the lowest cost producers in the potash market and makes it immensely profitable once it begins producing.

One of the biggest risks in a venture like this is the availability of sufficient funding to complete the project and bring it to production. In this regard, the company is listed on the JSE, and the ASX in Australia and the AIM in London. It has been selling shares to raise capital and in March 2025 it sold 455,7m shares for 1,7 pence each to raise $10,1m – which it still held in its bank account at 31st March 2025.

Over the time that Kore has been on the WSL up to last Friday (23-5-25) it has risen 290% in 373 days giving it an annualised return of 383,78% per annum.

From an investment perspective it remains highly risky because of:

- The mine’s location in the politically volatile Congo.

- The mine only expects to begin production in 2029.

- The fact that it is dependent on the international price of potash.

Obviously, as the next three years passes some of those risks will decline, culminating in it becoming a producing mine. Even then, however, it will still face the risk of being a commodity company in a part of the world which is known for sudden political upheavals. Dividends can only begin to flow in 2029 at the earliest, so prospective investors have to be very patient.

The government of the Congo is a 10% shareholder and has been very supportive of the project which it also expects to be a major source of tax revenue, but anything could happen in the Congo over the next three years. With high risk comes high potential return.

DISCLAIMER

All information and data contained within the PDSnet Articles is for informational purposes only. PDSnet makes no representations as to the accuracy, completeness, suitability, or validity, of any information, and shall not be liable for any errors, omissions, or any losses, injuries, or damages arising from its display or use. Information in the PDSnet Articles are based on the author’s opinion and experience and should not be considered professional financial investment advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional. Thoughts and opinions will also change from time to time as more information is accumulated. PDSnet reserves the right to delete any comment or opinion for any reason.

Share this article: