Wall Street’s relationship with Trump is evolving. At the start of his current term, when he was playing with the US tariff system, everything he said moved the markets. Today, tariffs have completely lost their force in the market and Trump has moved on to being a warmonger instead.

His attack on Venezuela did not move the markets, but it boosted his confidence and made him easy prey for Israel’s Netanyahu, allowing him to embroil the US in a war which does absolutely nothing for America and has certainly damaged Trump’s mid-term election prospects beyond repair.

The US/Iran war has reached a stalemate with both sides closing the Strait of Hormuz and both sides seizing commercial ships in the vicinity. What is interesting is that while the price of North Sea Brent oil has now climbed back above $105 per barrel, the S&P500 index has made yet another new all-time record high.

Investors are clearly looking beyond the oil price to the excellent results and predictions coming out of S&P500 companies, and especially the “magnificent seven”. Consider the chart:

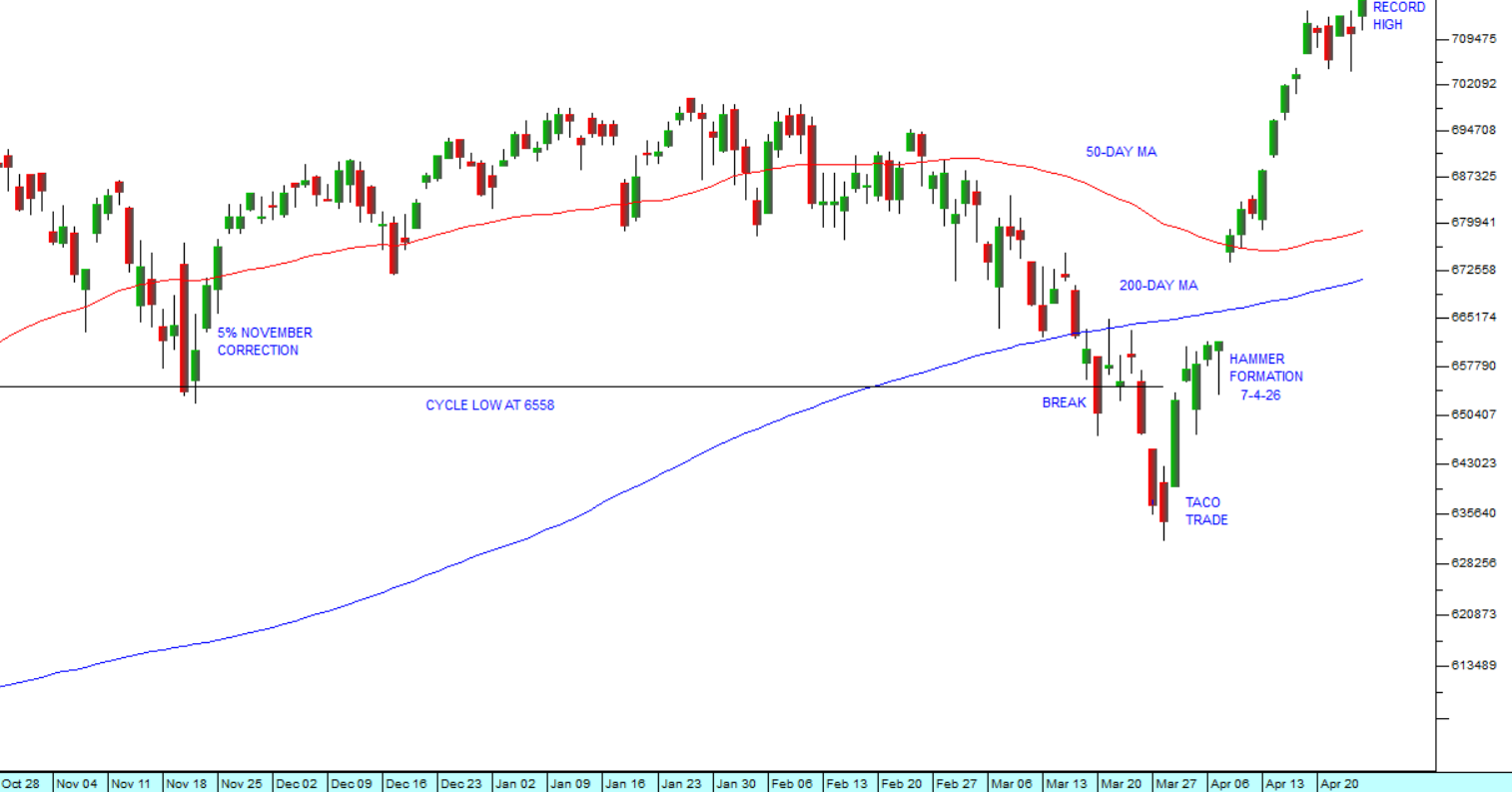

S&P500 Index : 28th of October 2025 - 24th of April 2026. Chart by ShareFriend Pro.

S&P500 Index : 28th of October 2025 - 24th of April 2026. Chart by ShareFriend Pro.

The chart shows the previous 5% correction in November last year and then Trump’s Iran war correction which broke to a lower low and created the opportunity for a TACO trade. You will note the important hammer formation on 7th April 2026 which gave a clear early warning that a strong recovery was coming. Note also that the 50-day moving average turned upwards again, away from the 200-day – indicating that a death cross had been averted.

The general investor perception is that the Iran war is a temporary phenomenon which will be resolved one way or another relatively soon. The primary impact of the higher oil price, while negative for the economy, has been to seriously erode Trump’s MAGA support base. It is also having the effect accelerating the movement away from fossil fuels towards renewables.

There is now concrete evidence that somebody in Trump’s camp has been profiting massively from his announcements on the war in Iran. There are three clear instances of insider trading in the oil futures market coming immediately prior to his announcements:

- On 23rd March 2026, a $500m short placed 15 minutes before Trump announced a delay in Iranian strikes.

- On 7th April 2026, a $950m short placed immediately before Trump announced the US-Iranian ceasefire.

- On 17th April 2026, a $760m short, placed minutes before the opening of the Strait of Hormuz was declared by Trump.

The Commodity Futures Trading Commission (CFTC) is investigating these trades.

MAGA has been blithely unconcerned about the fact that Trump is inter alia a convicted criminal, a rapist, an inveterate liar or that he and his minions have been engaged in blatant insider trading. MAGA is, however, very much concerned about the price of petrol (“gas”) which has remained stubbornly above $4 per gallon since the war began.

At the same time, the stock market is bracing for the biggest wave of initial public offers (IPO) in its history with SpaceX, Open AI and Anthropic all planning to come to the market later this year. They are endeavouring to raise a total of $3 trillion led by SpaceX’s $1,75 trillion offer. Open AI is looking for about $1 trillion and Anthropic wants $380bn. What is interesting about this is that all three companies are currently running at a loss. Space X, particularly, reported a loss of $5bn last year on revenues of $18,6bn.

This almost looks like the start of a top-of-market listings boom. Investors are losing sight of the underlying fundamentals and focusing only on blue sky potential. With its latest all-time record high last Friday, the S&P500 is now trading at an historical price:earnings ratio (P:E) above 30 – which must be compared with the median average for that index of between 15 and 18. In other words the index is discounting a substantial increase in earnings for its component companies.

Can that be justified? We believe that it can. There is little doubt that the productivity benefits of AI have only just begun to impact the profits of S&P500 companies – let alone other emerging new technologies like humanoid robotics. We believe that the bull trend will continue – but your best defence against a market collapse remains your stop-loss strategy.