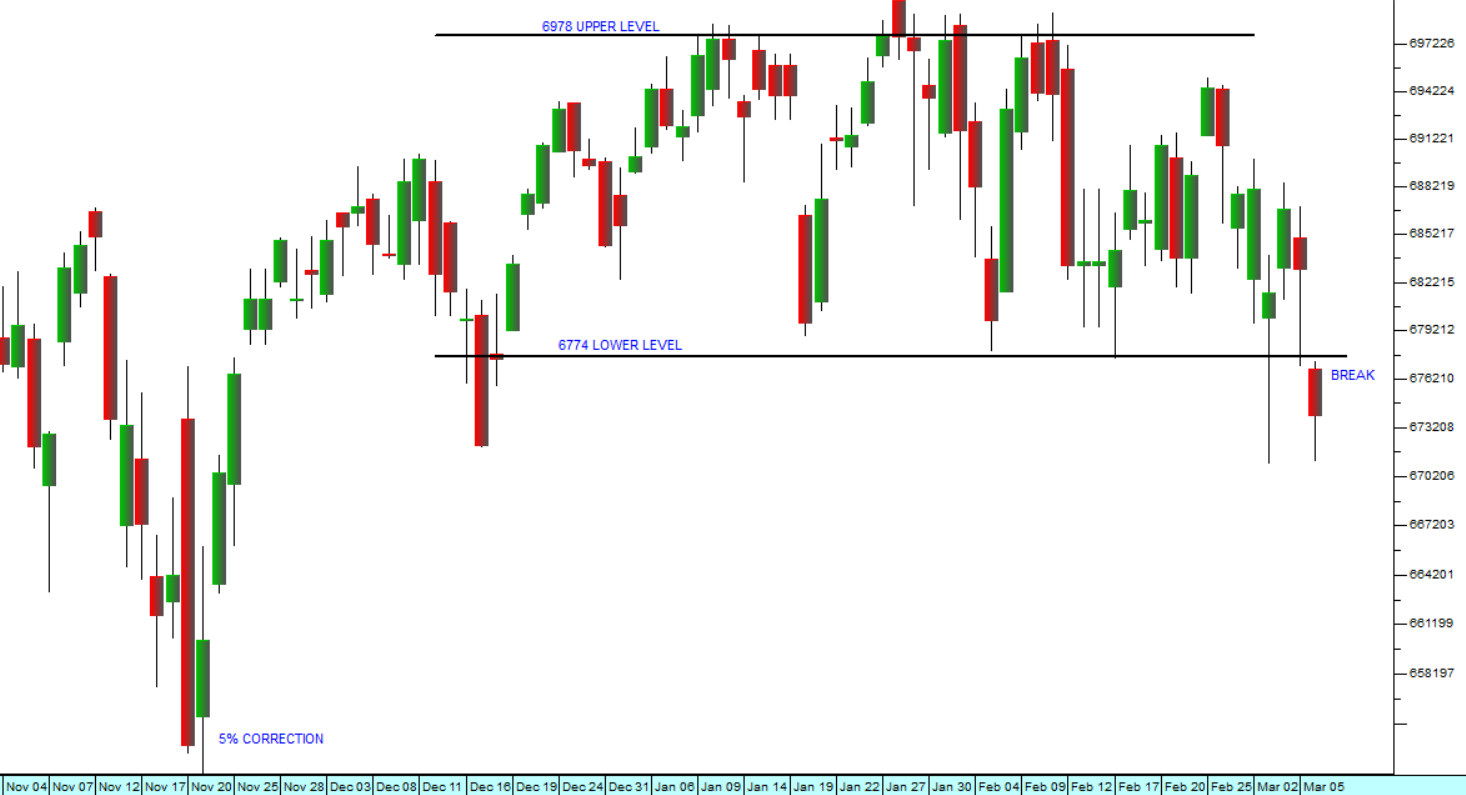

Are we teetering on the edge of a major bear trend? After Friday the 13th of March 2026's S&P500 close at 6632, Wall Street is now down 5% from its all-time record closing high of 6978.6 on the 27th of January 2026. This down-move is similar to the 5% correction which occurred in the first three weeks of November last year and it is evident that there is still considerable bullish sentiment in Wall Street, just waiting for their moment to buy the dip .

Into this mix, Oracle (ORCL) delivered strong Q3 FY2026 results on March 10, 2026, beating estimates with $17.2 billion in revenue, driven by a 243% surge in AI infrastructure demand. This demonstrates that the underlying strength of the AI boom in the US is still alive and well. If the war situation in Iran can be resolved, it is clear that the stock market will continue up to new record highs very quickly. Consider the chart:

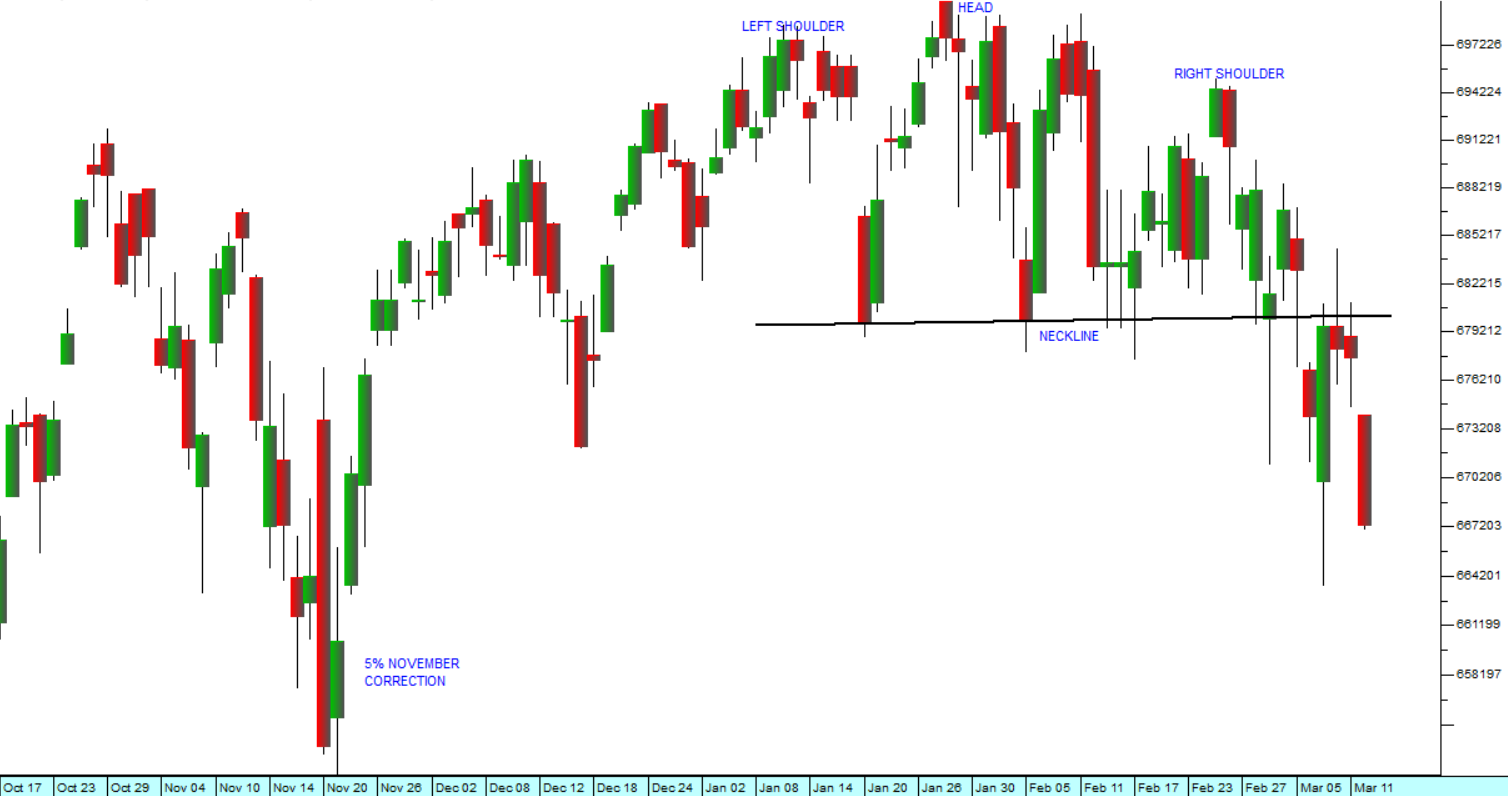

S&P500 Index : 17th of October 2025 - 13th of March 2026. Chart by ShareFriend Pro.

S&P500 Index : 17th of October 2025 - 13th of March 2026. Chart by ShareFriend Pro.

The chart shows the November correction and what some technicians are now suggesting is a head-and-shoulders formation. In our view, the formation is not particularly convincing, but after Friday’s move there can be no doubt that the index has broken strongly down.

Most of the problem comes from the jump in the oil price which has seen North Sea Brent rise to above $100. This is very good for Russia and Putin, while being very bad for Trump. The US Secretary for Defence, Pete Hegseth, seems to think that the problem is easily solvable, but we believe that it may be extremely difficult.

Normally, about 20% of the world’s oil passes through the Strait of Hormuz. This narrow sea passage is relatively easy to attack and control, and it is Iran’s only strong pressure point in its war with Israel and America. Its navy and air force have now been systematically eliminated by strategic bombing. The new leader of Iran, Mojtaba Khamenei, has specifically said that he will not allow any ships to pass through and that he will use the rising oil price to put pressure on Trump.

The problem is that to open the Strait will require boots on the ground in Iran. The Israeli/US forces will have to clear a corridor at least 30km wide along the Iranian coast adjacent to the Strait to prevent the firing of missiles and drones against passing ships. They cannot do this from the air. Having boots on the ground means incurring casualties.

Trump probably began this war in order to draw attention away from his problems with the Epstein files. He has however landed himself with a new problem – the rising price of petrol in America. His approval ratings have fallen to an all-time low and the November mid-term elections are looming large. The price of petrol has risen by 20% since the start of the war. On the other hand, his tax cuts will begin to impact in April resulting in refund cheques being paid after the tax-filing season ends.

On Feb. 7, 2026, Chasity Verret Martinez won a special election to fill a vacant seat in the Louisiana House. Martinez is a Democrat who took 62% of the vote in a district that had given Donald Trump a 13-percentage-point victory in the 2024 presidential race. And her win came a week after Democrats seized a Texas Senate district that had supported Trump even more strongly.

While these results are not conclusive, they are a strong indication that the Republicans will lose their control of the House and may even lose the Senate in November. Trump knows that, if he loses both Houses, he could easily be looking at impeachment – so suddenly control over the shipping passing through the Strait of Hormuz becomes critical.

How should you as a private investor respond to this situation? Our advice is not to panic but to monitor your stop-loss levels closely and act on them when broken. We believe that the situation will be resolved and that some degree of normalcy will return sooner or later. When and if that happens, we expect stocks around the world to bounce.