The news from various sources that the US is preparing to send thousands of marines and large quantities of military hardware to the Middle East is unsettling markets around the world. Combined with Iran’s efforts to disable oil production in adjacent countries in the Persian Gulf, these 2 factors have caused the S&P500 to fall 1,5% on Friday last week and brought it closer to a correction (generally accepted as 10% below the high point).

The evidence is that Trump and America are getting ready to put boots on the ground in Iran with the idea of the protecting shipping passing through the Strait of Hormuz. The Iranian coastlines on the Persian Gulf and the Gulf of Oman will be very difficult to control and protect because they are overlooked by the Zagros mountains and the Central Iranian range. These mountains, which have many cave systems, will be ideal cover from which small groups of Iranian commandos can constantly harass the invaders in the coming months.

In these troubled times the JSE Overall index has so far fallen 14,3% - twice as much as the 7,2% fall in the S&P500. This is as you would expect given that South Africa is a leading emerging market and our currency reflects the general worldwide shift towards risk-off. The imminent rise in our petrol price on 1st April could be as much as 25% or R5 per litre. This will push our inflation rate up and probably cause local interest rates to rise.

What is surprising in this scenario is that markets and especially Wall Street have not fallen further. This is because the tech companies in the US are still attracting enormous investor interest and there has been substantial “buying of the dips”. The general opinion of overseas analysts is that shares will bounce back from this correction before the end of this year.

Is this a reasonable assumption? In our view the short answer to the question is, “Yes”. Trump is well known for backing down and not sticking to anything when the pressure on him rises. In this case he is already coming under enormous pressure from both external sources and internally where his popularity has never been as low. With the mid-term elections due in November, he must be increasingly aware of the dire consequences of losing both the House and the Senate. If he puts boots on the ground in Iran now, he will certainly still be getting a steady flow of body bags back from Iran by November. And we believe it is unlikely that his efforts will make the Strait of Hormuz safe for shipping. But he is Trump and therefore totally unpredictable.

In these troubled times, there are relatively few companies which are not touched in some way by what is happening in the Middle East, and especially by the rising oil price. Mobile Telephone Networks or MTN as it is known is one of those companies. It describes itself as a “...pan-African mobile operator with the strategic intent of leading digital solutions for Africa's progress”.

In its most recent results for the year to 31st December 2025 the company reported service revenue up 22,9% and data revenue up 37,7%. Fintech revenue rose 30% and the company reported a 5,6% increase in total customers to 307,2 million.

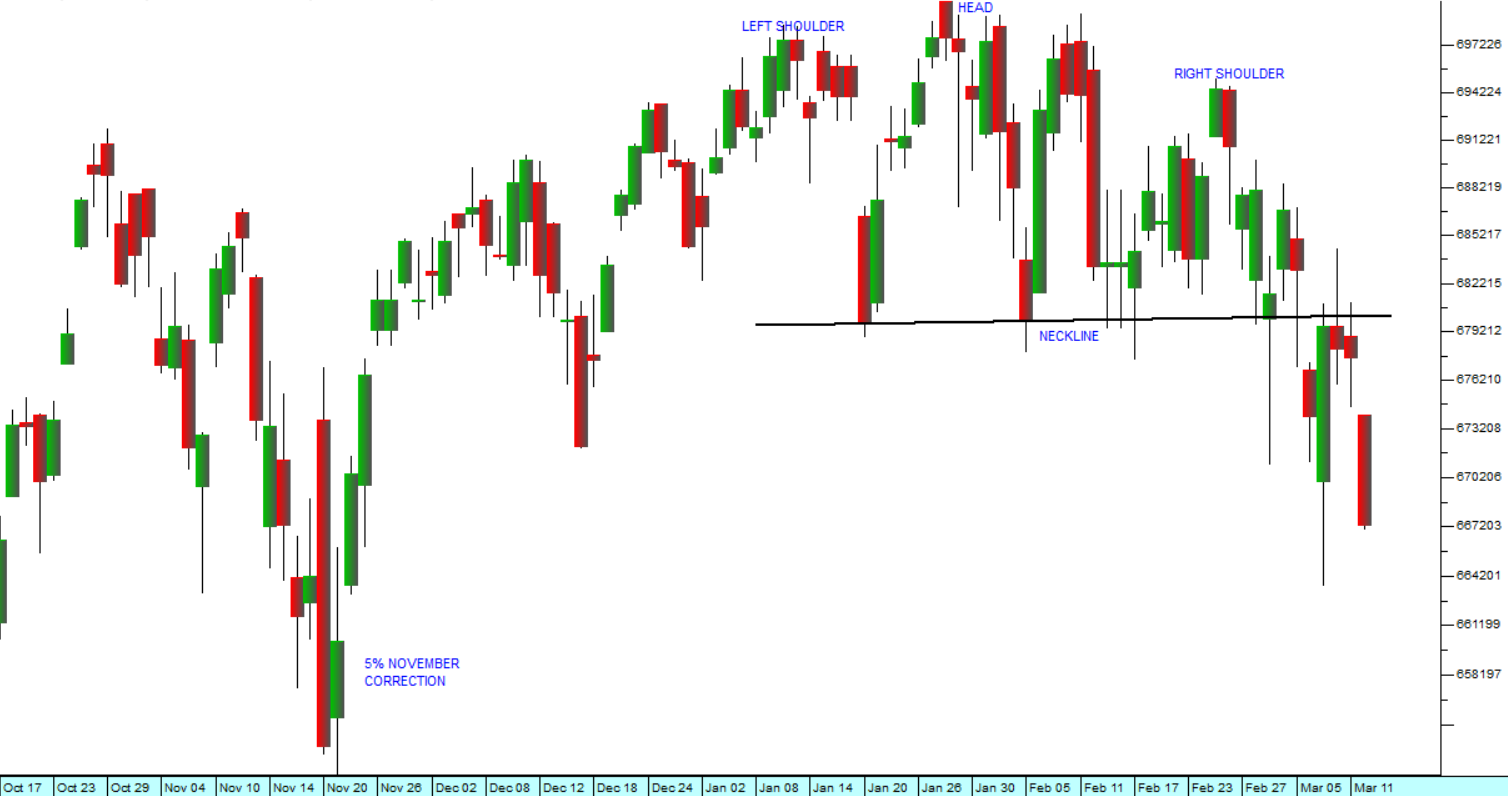

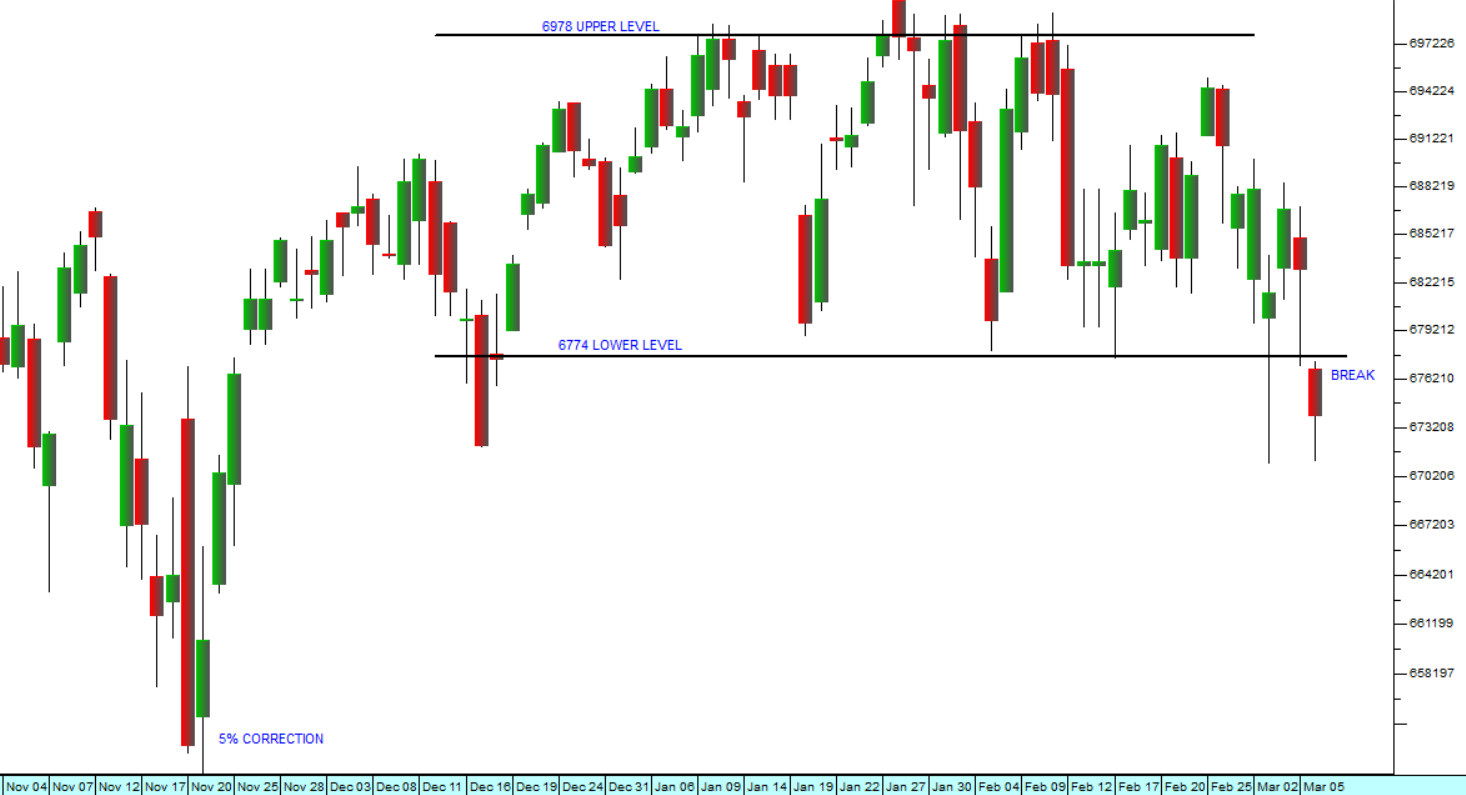

Technically, the share was in a sideways market from March 2024 until the beginning of 2025. It then entered a strong new upward trend. Consider the chart:

MTN (MTN) : March 2024 - 20th of March 2026. Chart by ShareFriend Pro.

MTN (MTN) : March 2024 - 20th of March 2026. Chart by ShareFriend Pro.

We added MTN to the Winning Shares List (WSL) on 15th January 2025 at a price of 9729c. Since then, it has risen to 19155c – or about 88%. While it has certainly felt some of the fall-out from the Iran war, its business is in Africa which should be largely unaffected.

So, we see this sell-off on the JSE as a buying opportunity to pick up high-quality shares at bargain prices. MTN is one of those shares, but others include Clicks which has now fallen even further due Trump’s war, but which was already heavily oversold.

Buying shares at a time like this can be scary, but remember our maxim:

“If you don’t feel the risk, then you are probably not going to make any money”.

Your ultimate protection in all of this is, of course, as always, your stop-loss strategy.