The Confidential Report May - 2026

So, once again, we ended this month with another new all-time record high on the S&P500 at 7209. Technically, the index has now broken well above Trump’s Iran war correction, generating a perfect TACO trade in the process. Throughout that correction we wrote 4 articles urging you to treat the correction as a buying opportunity. Consider the chart:

The chart shows the support on the S&P at 6538 created by the lows on 10th October and 20th November last year. Trump's Iran war correction briefly broke below that level before recovering strongly to a series of new record highs. You should note the hammer formation on 7th April 2026 which gave a clear technical indication of strong upward trend which followed. Note also the 50-day and 200-day moving averages which have avoided a death cross with the 50-day turning firmly upwards again.

The S&P is being driven by the solid quarterly results coming out of the S&P500 companies, especially the Magnificent Seven. So far, the blended (actual and estimated) growth in earnings is over 15% - making the first quarter of 2026 the sixth consecutive quarter of double digit increases in profitability. S&P Global reported strong Q1 results, with adjusted EPS of $4.97, beating estimates of $4.82. Total revenue for S&P Global increased 10.4% from a year-ago.

It is becoming clear that investors regard the massive increases in AI-generated productivity in the US economy as being far more important than negative of the rising oil price. One can only imagine how high the S&P would have been now had the war with Iran not happened and oil prices had remained at around $60 or $70 per barrel. Consider the chart:

The chart shows the progress of North Sea Brent oil over the past two years. What is immediately apparent is that oil was firmly in a downward trend before the problems in Iran began. It had broken down through support at around $72 per barrel and $60 per barrel prior to the January riots in Iran. These riots enabled Netanyahu to persuade Trump to begin his attack.

It is our opinion that once the war in Iran is over, the oil price will continue its downward path. This may not be for a while. In fact, Brent prices above $100 per barrel are stimulating the move away from fossil fuels worldwide. In a few years’ time we will see the oil price dropping to much lower levels, perhaps as low as $10 per barrel. The falling cost of energy, added to the productivity gains of new technologies, will, in our opinion, be one of the great drivers of the continuing bull market. The progress of the S&P500 shows that we are not alone in this perception.

Trump’s Iran War

Talks between America and Iran failed, and Trump has ordered a blockade of the Strait of Hormuz by the US navy of all ships coming from ports in Iran. The failure of the peace talks organized by Pakistan has had the immediate effect of pushing the North Sea Brent oil price back up to as much as $120 per barrel. The Americans used their bunker-buster bombs to destroy Iranian underground missile silos close to the Strait, but this does not seem to have reduced Iran’s control over the Strait.

Two American destroyers apparently passed through the Strait with the objective of commencing de-mining of the area to make it safe for shipping with Trump supposedly stepping up the de-mining operation. However, Iran is boarding vessels and running sea drones and small boats out of caves along the coast. Some commercial ships have managed to pass through the strait, but very few.

Our view remains that to control the Strait, America will have to put “boots on the ground” – which will inevitably result in casualties. Despite having moved thousands of marines to the Middle East it now seems improbable that Trump will begin a ground war. With petrol now costing as much as $1,30 more than when he started the war, Trump has been steadily losing his MAGA support base. Iran, for its part, has said that it is ready to repel any invasion by US ground troops. In our view, US ground troops would probably eventually be successful in taking control of territory around the Strait of Hormuz, but at a significant cost in terms of body bags going back to America.

There is much speculation about the value of the war in Iran both from an American and an Israeli perspective. Both Netanyahu and Trump have seen their approval ratings drop since the war began and both now face critical elections in the next six months. The IMF is now indicating that the impact of the war on fuel prices will certainly reduce growth across the world in 2026 and the effect will become worse the longer the high price of oil continues. In our view, the war was always ill-conceived, and the consequences were never properly evaluated from the outset.

Like most wars it began with the idea of a swift decisive victory resulting in regime change in Iran. Instead, it has become both protracted and expensive. Iran’s political leadership has effectively survived and hardened – despite Trump’s rhetoric. This is very similar to Russia’s invasion of Ukraine, and it now appears likely that both Trump and Netanyahu will ultimately lose power as a direct consequence. Iran, on the other hand looks set to emerge more united and stronger in the Middle East.

The ceasefire announced in the Iran war on 8th April 2026 was never going to hold. After an initial sharp drop back to around $91 per barrel, North Sea Brent Oil has since jumped to as much as $124 before settling back to around $108. Notably, this appears to be yet another instance of Trump being forced to back down on his deadlines and potentially accepting the Iranian’s revised peace offer. Their original 10-point plan basically gave them everything that they wanted. It has become another example of a successful TACO (Trump Always Chickens Out) trade.

It seemed unlikely from the start that the ceasefire, which included the opening of the Strait of Hormuz, would work - mainly because Israel does not feel bound by it and Netanyahu appears to have no real interest in ending the war. His attacks on Lebanon have continued. Any moves towards a lasting ceasefire will benefit banking and precious metals shares while property shares will also benefit from the prospect of lower interest rates.

There is now concrete evidence that somebody in Trump’s camp has been profiting massively from his announcements on the war in Iran. There are at least three clear instances of insider trading on the oil futures market immediately prior to his announcements:

- The 23rd of March 2026 - a $500m short placed 15 minutes before Trump announced a delay in Iranian strikes.

- The 7th of April 2026 - a $950m short placed immediately before Trump announced the US-Iranian ceasefire.

- The 17th of April 2026 - a $760m short, placed minutes before the opening of the Strait of Hormuz was declared by Trump.

The Commodity Futures Trading Commission (CFTC) is investigating these trades, but insider trading is notoriously difficult to prosecute.

America

It is evident that Wall Street is being supported by the above-estimated profits being reported by S&P500 companies. This effect has been sufficient to push the index to a new record highs well above 7000. For example, Morgan Stanley reported a 36% jump in investment banking revenue in the first quarter. Its revenue from equities trading increased by 25% and fixed income was up 29%. The negative of higher fuel prices has so far been insufficient to significantly constrain quarterly profits and investors have been gambling on an early resolution to the war in Iran.

As of 1st May 2026, the projection was that the profits of the S&P500 companies would come in about 27,8% above the previous year with 83% of companies beating earnings estimates and 78% beating revenue estimates. Overall, analysts expect to see earnings up over 21% for the year. Continued strong spending on AI infrastructure and rising corporate earnings are pushing the market to new record highs – and we expect this trend to continue in the immediate future. Obviously, the rising price of fuel is a major negative, but it has clearly been insufficient to dampen the enthusiasm on Wall Street.

In the meantime, non-farm payrolls increased by a whopping 178 000 in March month this year and unemployment fell back to 4,3%. This is massively better than February’s loss of 133 000 jobs and analysts’ estimates that jobs would increase by just 59 000. The health care sector alone added 76 000 jobs while construction added 26 000 jobs. Over the past four years the rate of job creation has definitely been declining – but that is what you would expect given the relatively high and rising level of interest rates over much of that period. But the strong employment market in America showed the inaccuracy of fears about a massive loss of jobs due to AI efficiencies and any suggestion that the economy was headed into a recession. But, of course, all of that was before Trump engineered an enormous $1.30 increase in the petrol price.

At the same time, the Federal Reserve Bank (“the Fed”) reported that core inflation (excluding food and fuel) increased by 0,3% in March 2026 to 3,2%. Headline prices on the other hand rose by 0,7% showing that the inflationary effects of the rising oil price are beginning to impact. Fuel and food prices took the inflation rate up to 3,5% and this does not yet reflect to full impact of the jump in oil prices. These numbers still put inflation well above the Fed’s target of 2% which probably means that there will be no further reductions in rates and there may even have to be as many as two 0,25% interest rates increases by year end. Everything depends on the war in Iran. If it is resolved quickly, then the Fed will be able to continue reducing interest rates in due course, but if it continues and oil prices remain high then rates will certainly have to go up. Our view is that sooner or later Trump will be forced to confront his dwindling popularity with voters and make a deal with the Iranians. The November mid-term elections are just five months away.

The Commerce Department also reported that gross domestic product (GDP) growth was 2% in the first quarter of 2026 – up from the 4th quarter of 2025 when the growth was just 0,5%. This is below analysts’ average forecast of 2,2% growth – but this, together with the jobs number for March still point to an economy which is growing rather than stagnating. The impact on AI appears to be a re-organisation of the labour force rather than the wholesale loss of jobs which some analysts were fearing.

America is bracing for the biggest wave of initial public offers (IPO) in its history with SpaceX, Open AI and Anthropic all planning to come to the market and raise massive blocks of capital in the process. They are aiming to get investors to contribute a total of $3 trillion led by SpaceX’s $1,75 trillion offer. Open AI is looking for about $1 trillion and Anthropic wants $380bn.

What is interesting is that all three companies are still running at a loss. SpaceX reported a loss of $5bn last year on revenues of $18,6bn. Open AI has Chat GPT while Anthropic runs Claude, so both are participating in the AI business explosion. At the same time, Wall Street has been making new all-time record highs – so making public offers like this makes sense right now. It is a great opportunity for companies to create vast quantities of permanent interest-free capital.

These three listings could easily be the start of a listings boom in the US as investors desperately strive to buy into the high-tech boom. The Magnificent Seven (Tesla, Nvidia, Amazon, Apple, Alphabet Meta and Microsoft) have been dominating the S&P500 and now account for about one third of its total valuation. They generated 43% of its profits in 2023, 37% in 2024 and 25% in 2025 – so the percentage is declining as the share market boom broadens to other S&P500 companies. Their share of the S&P should be compared with the remaining 493 companies in the index which together accounted for minus 1,3%, 7% and 11% in those same years. The dominance of the Magnificent Seven is clear – but it also increases the systematic risk. Private investors need to take a position on the future of AI and its impact on corporate profits. Our view is that we are just at the beginning of this technical revolution and that productivity levels and profits will continue to rise.

A great measure of Trump’s growing unpopularity has been given by the “No Kings” protests in America which drew an estimated 8 million people in more than 3200 events. These events, which are essentially, anti-Trump events, have been growing in size. They received a major boost from the widespread opposition to Trump’s war in Iran and the sharp rise in the price of petrol. In our view, the size of the protests bodes well for the Democrats chances of winning both Houses in the November mid-term elections. They may even be able to get sufficient votes in the Senate to get Trump impeached and removed from power.

In this regard, the victory of Peter Magyar in the Hungarian elections has been a major blow to right-wing politics and fascism worldwide. It is especially bitter for the Trump administration and Vance who went to Hungary specifically to support Orban. The landslide result will have far-reaching consequences because Magyar has won sufficient seats to alter the Hungarian constitution. Hungary has now withdrawn its opposition to the EU’s 90-billion-euro support package for Ukraine. This will enable Ukraine to continue financing the war for a further two years – something that Russia and Putin cannot simply afford.

MAGA Republicans in America and especially Trump himself must now view this as a potential harbinger of what is to come in their November mid-term elections, especially because of Trump’s outspoken support for Orban and the fact that this is one problem that he cannot blame on the Democrats.

Orban’s catastrophic loss is also a serious blow to Russia and Putin, adding to the tally of close allies around the world lost to Russia in recent months. The problem for Putin is that, like Finland and Sweden, Hungary will now become a fully cooperating participant in NATO and the European Union. And it will certainly not be funnelling confidential NATO information back to Moscow.

Ukraine

The immediate consequence of Trump’s war in Iran has been that the war in Ukraine has taken a back seat. Most of the headlines are now focused on what is happening in the Middle East and attention has shifted away from Putin’s “special military operation” in central Europe.

There is growing evidence that Ukraine is winning the drone war with Russia. One of the most notable developments is the use of unmanned ground vehicles (UGV). In March 2026 alone Ukraine conducted 9000 missions using UGVs. Its goal now is to transfer up to 100% frontline attacks to unmanned robotic systems. To do this the country is contracting to produce 25000 UGVs in the first half of 2026 and as many as 50 000 in the full year. This signals an important shift in tactics and potentially eliminates Russia’s manpower advantage in the war. UGVs operating in conjunction with unmanned aerial vehicles (UAVs) have now successfully taken over Russian position on the frontline. Troop rotations and resupply are now increasingly being done by UGVs.

With the advent of the Magyar as the new leader of Hungary, Ukraine has re-opened the Druzhba pipeline to ship Russian oil to Europe and the 90bn euro financing deal for Ukraine has been approved. At the same time, Russia’s economy is running on fumes and cannot possibly consider maintaining the war for a further two years. Putin is in a corner and there seems to be no realistic way out of it, despite the sharp increase in the oil price since the start of the Iran war. The continuous destruction of Russia’s oil infrastructure and its oil export ports has seriously depleted its ability to generate oil revenues. Half of the new EU funding will become available this year with the balance coming through next year. This enables Ukraine to continue its very ambitious and effective drone production program.

In a new development, the head of the Russian communist party, Zuyganov, speaking to the Russian Duma, recently warned that the first quarter of 2026 was a disaster for the Russian economy and that the country would face revolution by August unless urgent steps were taken. He believes that the economy will inevitably collapse. He envisages a repeat of what happened in Russia in 1917. The Russian economy is running out of money because everything is being spent on the Ukraine war. More people are speaking out and posting their concerns online. In our view, the situation in Russia will come to a head this year.

It is also interesting that the Ukrainian Sky Map software has been implemented at the Prince Sultan airbase in Saudi Arabia which is used by NATO countries and America. Ukraine is now showing off its superiority in anti-drone technology to defend the assets of Arab countries and NATO military bases. Ukraine has begun exporting its technologies to friendly countries and it is now undisputably the world’s leading expert in modern warfare.

A clear indication of this is Ukraine’s strike over the weekend on Lukoil’s Perm refinery 1500 kilometres inside Russia. This refinery sits at a critical junction in the Russian oil pipeline system and processes 13m tons of crude oil per year. The two successive strikes have created a massive fire which will be very difficult to extinguish, and which is resulting in a continuous “rain” of oil on the residents of the city of Perm. This refinery pumps oil to ports like Novorossiysk and Tuapse in the Black Sea and also to Ust Luga and Primorsk in the Baltic Sea.

Political

The latest Ipsos polls show that the ANC only has support from 33% of eligible voters in SA. This is a sharp drop even from its disastrous performance in the last elections, where it lost its majority in Parliament and was forced to form a coalition with its arch-enemy, the DA. The accession of Geordin Hill-Lewis to the leadership of the DA promises to usher in a new era of reform and a strong push to increase the DA’s share of the government of national unity (GNU). Hill-Lewis has indicated that his goal is to take control of the GNU in the future, and the trajectory of the ANC indicates that this may well be possible. For private investors on the JSE and for the economy, the rapid decline of the ANC and the rise of the DA can only bode well. As the DA takes over more departments and cities, we can expect service delivery to improve and corruption to decline. Already this trend has been very evident in DA managed departments like Home Affairs.

The new draft rules for Black Economic Empowerment (BEE) amount to a further deep involvement of the government in the management of private enterprises and how they are run. Essentially, if implemented, they will make it much more difficult for businesses to take advantage of the massive R1 trillion infrastructure spending program which the government has proposed for the next 3 years. They make South Africa that much less attractive for overseas investors and open the door for further corruption. Perhaps the emphasis on tightening up BEE is an attempt by the ANC to bolster grassroots support, but in our view, it just adds a new layer of bureaucratic red tape.

Economy

The Reserve Bank’s leading indicator rose by 6,4% in February 2026 compared with a year ago and up 0,5% compared with January. Residential building plans and commodities were the largest contributors. This shows that prior to the hike in fuel prices due to the Iran war, the South African economy was growing steadily. With a further hefty fuel price hike in May, it is likely that the monetary policy committee will have to hike interest rates later this year and the level of economic growth will decline. It now seems likely that the price of North Sea Brent will remain high for at least the rest of this year.

The consumer price index (CPI) rose to 3,1% in the year to the end of March month, slightly up on February’s 3%, but this is before the impact of the jump in fuel prices. The impact of the jump in fuel prices will only be seen in the April CPI figures due to be published on 20th May 2026. And after that, depending on how long oil prices remain high, the secondary effects will feed through to food prices and other components of the inflation rate. The government will definitely step in once again to mitigate the impact of higher fuel prices, but consumers will bear the brunt and consumer spending levels will inevitably have to fall. Retail sales fell to 1,6% in February from January’s 4,4% and will probably fall further as consumers divert cash to their petrol tanks in May. We expect the economic fallout from Trump’s war in Iran to gain momentum as the year progresses.

The Reserve Bank says that the “near term inflation outlook has deteriorated significantly” because of the war in Iran and the sharp rise in fuel costs. They are predicting that inflation will be 4% this year but fall back to 3% next year on the assumption that the oil price will come down later in the year. At its meeting in March the monetary policy committee (MPC) kept rates unchanged at 6,75% but may now have to increase rates later this year to counter the impact of inflationary pressures. The Bank still expects gross domestic product (GDP) to grow by 1,4% in the 2026 year, fuelled by consumer spending, but this prediction looks unlikely in the face of the further increases in the price of fuel. Fortunately, thanks to our excellent Reserve Bank governor, Lesetja Kganyago, the country was in a strong position to meet this external shock with inflation running at just 3%.

Citi Bank has done an assessment of the impact of the Iran war and higher fuel costs on the South African economy. In their view, the higher cost of fuel, if it continues, could result in a trade deficit and an inflation rate of 4,9% in 2027. South Africa is a net importer of fuel, which makes it vulnerable to the international price of oil. The bank also expects that the Reserve Bank will be forced to raise interest rates by 0,25% in each of May and July of 2026. Fortunately, the resumption of the upward trend in share prices signals a shift back towards risk-on and a continuation of the rand’s long-term strength against the US dollar. This will tend to cushion the impact of higher oil prices on the economy.

The sharp 32% increase in the price of diesel is impacting the trucking industry in South Africa. Because of the bottlenecks and inefficiency of Transnet, a disproportionate quantity of South Africa’s bulk transport is done by road rather than rail. The economy is therefore exposed to the hike in the price of diesel. Trucking companies are already buying less bulk diesel at these prices and there will probably be more price hikes in May and June unless the war in Iran can be resolved. There are about 2500 road freight companies in the Road Freight Association (RFA), and many are now facing a major cost increase that some will not be able to afford. The higher cost of fuel is feeding through into inflation and will inevitably result in lower gross domestic product (GDP) and falling employment levels.

The under-recovery on diesel caused by the Iran war was R10 a litre – so the sharp hike diesel prices directly impacted people using illuminating paraffin as well as South Africa’s freight, mining and logistics sectors. Iran is allowing ships coming to South Africa to pass through the Strait of Hormuz, so there is no immediate supply problem. The problem comes from the much higher prices of oil on the international market. Diesel, which is not regulated, has already risen by R8 per litre.

Mining production rose by 9,7% in February 2026 mainly because of platinum group metals (PGM) which increased by more than half according to Stats SA. The price of platinum rose by 130% in 2025 on fears of shortages and a lack of new production. The manganese price rose by almost 18% and gold was up almost 13%. The increased production is having an impact on corporate tax collections from the mining industry and that in turn is helping with the country’s efforts to consolidate and reduce the national debt. Costs in the mining industry were lower, but these figures do not yet reflect the impact of the Iran war on fuel costs.

The decline in rail volumes from 226m tons in 2017 to 150m tons in 2023 is a matter of national concern. Rail transport costs about a quarter of road transport so the ineffectiveness of our rail system massively increases the costs of doing business throughout the economy. It also results in extreme congestion on our national highways and the deterioration of road surfaces in many areas. Transnet is trying to deal with the steadily declining quality of its track, equipment shortages and maintenance backlogs. There has been a 180 percent increase in security incidents and a ten-fold increase in cable theft over the last five years. Until these problems are resolved, it is difficult to see how the economy can grow significantly above current levels, especially with the higher price of fuel.

The cost of mining in South Africa is about to increase dramatically with a resultant reduction in profits and hence tax revenue. Mines are likely to have to pay about 50% more for fuel, with open-pit operations bearing the brunt. Then the second-round effects of the fuel price hike in inflation will come through in the coming months as the prices of food products and other products increase. All of this comes on top of Eskom’s 8,8% hike in electricity costs which came into effect from 1st April 2026. As the cost of mining increases, we can expect shaft closures and retrenchments. Tax revenues will fall as profits fall, leading to a more difficult fiscal situation.

One of the inevitable results of the war in Iran and the closure of the Strait of Hormuz is that food prices will increase. One aspect of this is the higher price of fuel, but another is the shortage of fertilizers. These two problems will push farmers’ costs up and they will pass that on to food manufacturers and, ultimately, the consumer will pay more for groceries. Roughly 35% of a farmer’s costs are fertilizers which will impact on the prices of food staples like sugar, grains and oil seeds. This country imports about four fifths of its fertilizer, which makes it very vulnerable to spikes in the international prices of these commodities. About one third of the commodities necessary to make fertilizers come from the Middle East. Higher fertilizer costs will be added to higher fuel costs. Fuel usually makes up about 13% of a farmer’s costs. The combined effect of these price increases will certainly impact food prices if sustained.

The cost-of-living report produced by the Competition Commission shows that electricity costs about 85% more than it did in 2020 and that water prices have risen by 65%. Over the same period inflation has risen by about 30%. This shows the inefficiency at Eskom and in the municipalities. Unfortunately, the poorest people in the country tend to carry a disproportionate amount of these increases. The same is true for food costs which are expected to rise sharply in response to the rising cost of fuel and fertilizers.

The Payinc index of transactions showed that the value of electronic transactions in South Africa rose by 0,9% in the month March 2026 and by 4,6% from a year ago. This shows that the South African economy grew over the year, but this precedes the impact of the Iran war on fuel prices. It is difficult at this stage to predict exactly how the jump in fuel prices will impact the economy. It really depends on how protracted the increases prove to be. Our expectation is that the oil price will remain substantially above where it was before the war began at least until the end of this year – but that the rand will resume its strengthening trend.

Manufacturing output fell by 2,8% in February 2026 which compares with a 1,4% contraction in December 2025. Food and beverages contracted 4,5% in the month. Given the jump in fuel prices in March due to the Iran war, it now seems inevitable that the quarter as a whole will see a decline in manufacturing. The figures are in line with ABSA’s purchasing managers index which fell to 47,4 in February showing that manufacturing continues to shrink. Even before the impact of the Iran war, 7 out of 10 sectors were down. A year ago South Africa was the 7th most attractive emerging market economy for investors. This year it has fallen to 12th position because of the decline in mining production late in 2025.

ABSA’s purchasing managers index (PMI) is quite volatile, but the trend since 2021 has definitely been downward – and the index has slipped below 50 which basically means that manufacturing is now contracting – and this is before the impact of the Iran war and the upward spike in the fuel price is considered. March month saw the index rise 1,6 points to 49. The higher fuel prices caused by the weakening of the rand and the jump in the price of imported oil are cutting into the profits of all manufacturers, no matter what they produce.

The pain which local car manufacturers have been experiencing because of the flood of imported vehicles from China and India may be beginning to pay off as Chery has made the decision to begin manufacturing inside South Africa. The Chery plant will assemble semi-knock-down (SKD) vehicles which is a big move from completely-knocked-down (CKD) vehicles. The plant is expected to employ about 3000 staff. Chery is now selling about 50 000 vehicles per annum in South Africa.

The Rand

The rand has been at the volatile whip-end of the war in Iran immediately discounting the sharp switch to risk-on at the war’s start and then the move back toward risk-off as markets discounted the effect of the higher price and focused instead on the compelling potential of the AI revolution.

The chart shows the weakest point in the rand on 9th April last year at R19.75 and then the steady appreciation to the resistance at R17,50. That resistance was then broken and became a support level as the rand’s strengthening path continued. Finally, the strongest point of R15,79 was reached at the end of January earlier this year when the war in Iran began to influence international investor sentiment. The subsequent weakening of our currency has, in our view, been very muted – mainly because of the Reserve Bank’s on-going and successful efforts to bring inflation in this country under control. Obviously, the hike in fuel prices is a major negative, but the rand is well positioned to “ride out the storm”. Inevitably, probably next year sometime, as oil prices return to their previous levels, we can expect the rand to continue its strengthening trend against the US dollar.

Commodities

ALUMINIUM

Since April last year the price of aluminium on world markets has been rising. It is used in transportation (aircraft, cars, ships), construction (window frames, roofing), packaging (cans, foil), and electronics. It is lightweight, corrosion resistant and strong. About 9% of global aluminium supply comes from countries around the Perian Gulf so supplies have been threatened by the war in Iran and Trump’s naval blockade. Consider the chart:

The chart shows the steady rise in the price of aluminium over the past year – a trend which accelerated from the beginning of this year and further when Trump began bombing Iran. In our view this essential metal which is primarily used by China will continue to be is short supply.

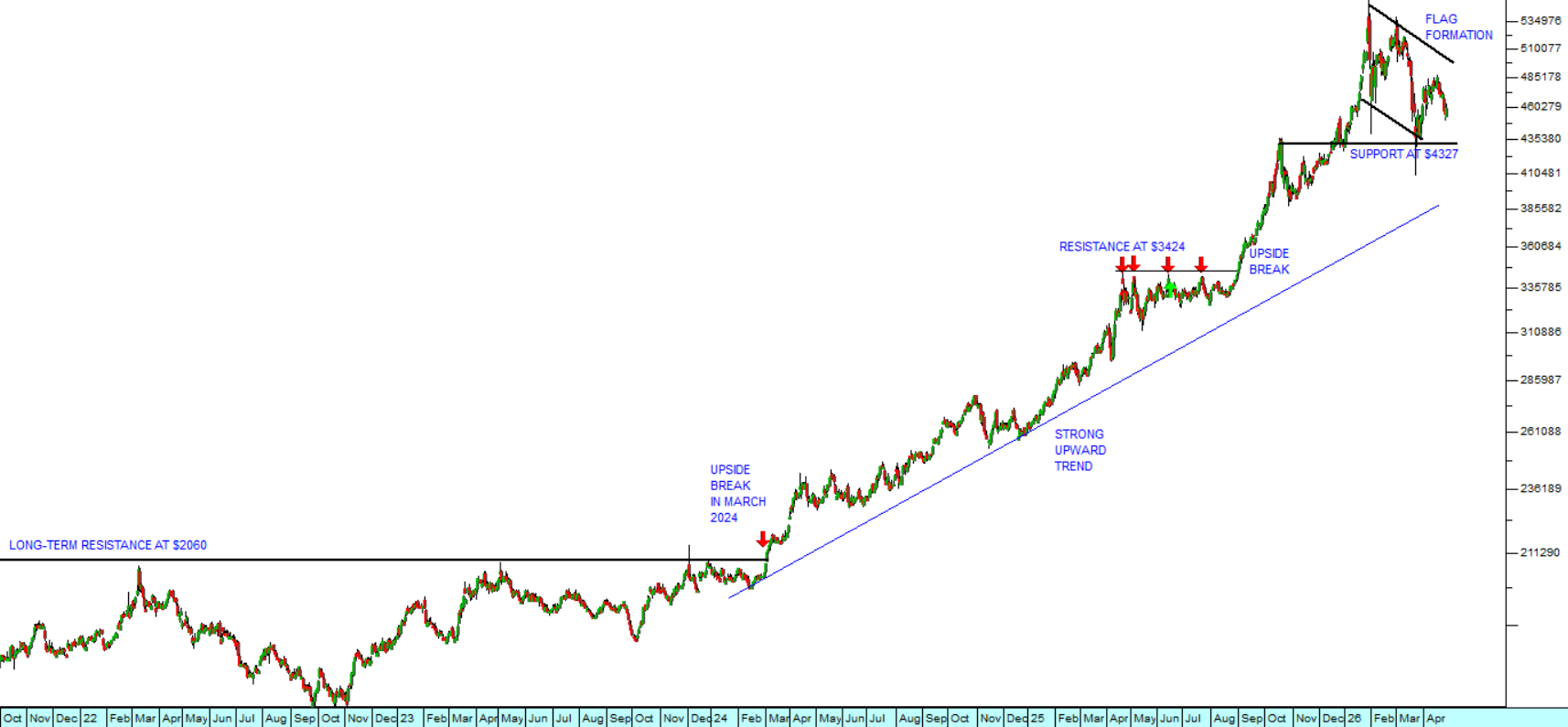

GOLD

Gold and oil have historically moved in tandem. This is because the oil price is directly linked to world inflation. When the price of oil rises it impacts on the price of almost every product in the world sooner or later because almost all products must be transported by a vehicle with an internal combustion engine at some point in their lives. Many products are also either made of plastic or contain a significant amount of plastic. Gold has always been the ultimate hedge against the weakness of paper currencies and political risk. So, it is surprising that the jump in the oil price as a result of the war in Iran has resulted in a decline in the gold price rather than the opposite.

The chart shows the gold price in US dollars going back to October 2021. At that time, gold had found long-term resistance at $2060 which was only eventually broken in March of 2023 when the current upward trend began. There was further resistance at $3424 last year, but that was convincingly broken in August and the price raced up to over $5300. At that point it was clearly overbought and some kind of correction was inevitable. That correction, beginning in February this year took the form of a flag or pennant formation which is still currently in progress. That formation has not been caused by or even much influenced by the war in Iran. Rather it is a natural result of the overbought record high in January. It does not signal the end of the upward trend in gold, but rather a regrouping and consolidation phase. We believe that gold will continue its upward trend in due course and that therefore this correction represents a buying opportunity for those investors not yet in the gold market and those who wish to increase their positions.

The World Gold Council reported that demand for gold ETF’s fell by 73% in the first quarter of 2026 and the demand for gold jewellery fell by 23%. Gold jewellery is now at its lowest demand level since the pandemic in 2020. Investors are worried that the rise in the oil price as a result of the war in Iran will trigger rising interest rates around the world and so make gold less attractive. Central banks have also been selling their gold holdings to create liquidity. We believe that the drop in the gold price is temporary and that in due course gold will return to levels above $5000 per ounce. The chart, however, shows a descending triple top formation which is usually bearish at least in the short term.

Companies

ADVTECH

ADvTECH is one of the largest education training and placement companies in South Africa. It supplies formal education from pre-primary all the way to post-graduate and both face-to-face and online and distance learning. The education business has the great advantage that traditionally customers pay for their education in advance. This means that ADvTECH does not have a significant working capital problem and has very strong cash flow. In its results for the year ended 31st December 2025 the company reported revenue up 10% and headline earnings per share (HEPS) up 17%. Technically, the share has been on an upward trend for the past two years. Consider the chart:

We added ADvTECH to the Winning Shares List (WSL) on 14th August 2023 at a price of 1975c. It has since more than doubled to 4265c. We regard it as a solid steady performer that continues to grow and benefits directly from the poor quality of government schools in South Africa. We see the share currently in a correction as recovering in the coming months and going on to further new record highs.

SPEAR

The property sector has staged a strong recovery from the COVID-19 pandemic of 2020 and 2021. Spear is a real estate investment trust (REIT) which has the distinction of being the only REIT listed on the JSE which specializes in property in the Western Cape. The company has a diversified portfolio of industrial, retail, commercial, and mixed-use properties. During the ten months to 31st December 2025 the company acquired properties worth R1,1bn at a yield of 9,54%. The company’s loan-to-value ratio (LTV) is just 25% - which means that it is a very low-risk investment and has plenty of head-room for further acquisitions. Technically the share has been in a steady upward trend for the past two years – a trend which we see continuing. Consider the chart:

Property shares are typically slower moving investments, but they have the great advantage of being almost risk-free, especially where, like Spear, they have a very modest and conservative LTV. We added Spear to the Winning Shares List (WSL) on 26th June 2024 at a price of 888c. It has since risen to 1296c, and we expect it to continue to be a steady performer.

QUILTER

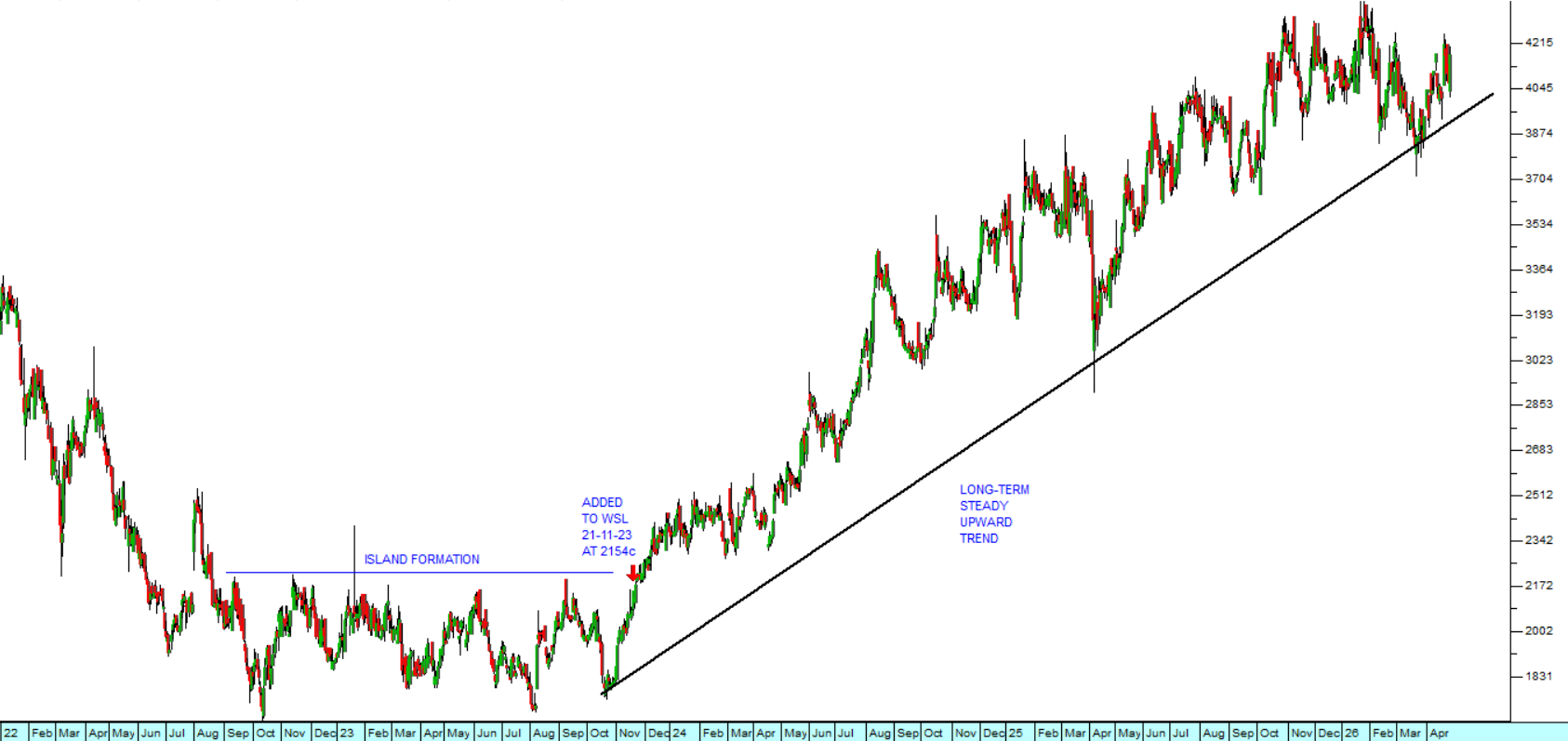

Quilter Plc (QLT) is a company spun out of Old Mutual as part of that group's "managed separation" process. It was admitted to trading on the London Stock Exchange (LSE) and has had a secondary listing on the JSE from 25th June 2018. Its main business is asset management, and it had assets under management (AUM) of £141.9 billion (R3,2 trillion) at 31 March 2026. Consider the chart:

In the first quarter of 2026 the company reported core net inflows, exceeding £3 billion for the first time. Q1 core net inflows increased 35% on the prior year period and represented 9% of its AUM. Clearly the company is also benefiting directly from the new record highs on Wall Street and other leading stock exchanges. Technically, you can see that after an extended period of sideways movement from September 2022 to the end of 2023 the company broke out of this island formation and began a strong new upward trend. We added it to the Winning Shares List (WSL) on 21st November 2023 at 2154c. It has subsequently risen to 4182c. It is obviously a rand hedge and we expect it to continue to perform well and to offer local investors a hedge against any weakness in the rand.

PSG FINANCIAL SERVICES

This company may be known better to some as PSG Konsult (KST) and was the subject of our article published on 20th April 2026. Its business consists primarily of asset management and insurance. In its results for the year to 28th February 2026 the company reported R540bn of assets under management (AUM), up 20% from the year before. It also reported its gross written premiums up 5% to R8bn. The company’s core income increased by 22% to R8,28bn and its recurring headline earnings per share (HEPS) rose by a whopping 34%. These are excellent results. Consider the chart:

We added KST to the Winning Shares List (WSL) on 23rd May 2024 at a price of 1610c. It has subsequently risen to 2825c, and we expect it to continue performing well. You will note that the share came off quite sharply over Trump’s war with Iran at the beginning of March 2026 and so offered a great opportunity to execute a TACO trade. It should reach a new record high in the next few months.

DATATEC

Datatec (DTC) is an international IT and telecommunications company operating in more than fifty countries. It operates in the United States, South America, Europe, Africa, the Middle East, and Asia. Its business is divided into three main divisions - technology distribution through Westcon International, integration and managed services through Logicalis, and consulting and financial services through Datatec Financial Services and Analysys Mason.

In a trading update for the year to 28th February 2026 the company reported gross profit up 10% to $998m. Like many international companies, Datatec fell quite heavily at the start of the Iran war. Consider the chart:

You will note that from April 2023 to October 2024 this share was moving sideways. Then in October 2024, it began to perform and entered a new upward trend. We added it to the Winning Shares List (WSL) on 26th October 2024 at a price of 3950c and it did very well until Trump attacked Iran. That brought the share down sharply and it has only just begun to recover. It has broken convincingly out of the Island formation that it has been in since mid-March 2026, and we believe that it will now enter a new upward trend that will see it rise to a new record high in a month or so.

From Jack:

I am available to discuss any of these shares or other share market-related questions you may have. I am available on WhatsApp at this number: 071 502 2383.

← Back to Reports