The Confidential Report - June 2026

America

Since the last Confidential Report on 6th May 2026, the S&P500 has moved further up, recording its 9th consecutive week of gains and reaching an historical price:earnings ratio (P:E) of 32.67. This P:E is well above average and the upward trend on Wall Street is rapidly becoming exponential. Consider the chart:

The chart shows the correction resulting from Trump’s war in Iran and the point where he began to back down, creating a classic TACO trade at the beginning of April 2026. Since then the market has been accelerating to a series of new record highs culminating in last Friday’s closing record at 7580.

Note the hammer formation on 7th April 2026 which gave a strong bullish signal immediately before the S&P “gapped up”. Hammer formations are often a very good short-term indicator of strong bullish market sentiment. The previous high of 6978.44 was quickly reached and exceeded as investors realised that the impact of AI was far more powerful as an economic force than the price of fuel. The bet was always that Trump’s bravado would be short-lived.

So now we expect that the market will continue to make new record highs. Obviously, nothing in the markets moves in a straight line so the experienced private investor will already be looking for and expecting the next correction. The bull trend however remains firmly in place, and we do not see it ending any time soon. Ed Yardeni, founder and CEO at Yardeni Research, and a highly respected analyst, increased his prediction of where the S&P will be by the end of this year to 8250.

The driving force behind this bull market is the profits coming through from biggest tech companies. The 30 largest companies in the S&P500 index now represent about two-thirds of the index’s market capitalization while the smallest 100 account for less than 1%. The Magnificent Seven grew 61% in the first quarter of 2026 – nearly four times as much as the remaining 493 companies in the index.

In the first quarter of their 2027 financial year, NVIDIA reported $81.6bn in revenue, up 85% over last year, with its Data Centre segment contributing $75bn and networking revenue surging almost 200%. The CEO, Jensen Huang, said “...the buildout of AI factories is the largest infrastructure expansion in human history.”

The rising stock market is in direct contrast to collapsing US consumer sentiment. Consumers are particularly depressed because of the increase in the cost of fuel and fears of the second-round inflation working its way through the economy. The cost of living continues to be a major concern for consumers with 57% spontaneously mentioning that high prices were impacting their budgets, which is up from 50% a month ago. Lower-income consumers and those without college degrees (in other words, Trump’s MAGA support base) posted particularly strong declines in sentiment. These people are far more sensitive to increases in the cost of “gas” and other essentials.

The worries about future inflation have been pushing bond yields up and that tends to be negative for stocks in the longer term. The yield on the 10-year Treasury Bill climbed briefly to 4,7% before falling back to 4,4% by the end of the week. All over the world, bond yields are being pushed higher by the fear of incipient inflation and the prospect of rising interest rates.

The immediate driver of the new record highs on Wall Street is the draft deal which has apparently been agreed between Iran and the US to extend the ceasefire for a further 60 days. The deal still has to be accepted by Trump. Optimism about this has seen the oil price (North Sea Brent) drop as low as $84. Clearly Trump is desperate to bring the cost of fuel down in America before the mid-term elections in November.

Jobs numbers for April came in at 115000 jobs created following March’s revised figure of 185 000. The April number was double economists’ expectations of 62 000 and it indicates that the economy is still growing. It also indicates that AI is not yet resulting in the massive unemployment that some analysts have been predicting. The US gross domestic product (GDP) grew by 1,6% in the first quarter of 2026. This is slightly above the 1,4% growth in the last quarter of last year.

Inflation in America rose to 3,8% in the year to the end of April 2026 and was 0,6% for the month. Core inflation which excludes the cost of food and fuel rose by 2,8% in the year and by 0,4% in the month. This is obviously well above the monetary policy committee’s (MPC) goal of 2%. A wide range of consumer products and services went up driven by the cost of fuel. Fuel increased by 3,8% in the month and accounted for 40% of the rise. Energy prices are up almost 18% so far this year with gasoline rising 28,4% per annum. Airline fares were up 2,8% on the month and 20,7% for the year. At the end of April, the MPC kept interest rates unchanged, but they may be forced to begin increasing rates at their next meeting unless fuel prices come down dramatically. The US producer price index (PPI) jumped by 6% in April 2026 – up from March’s figure of 4,3%.

Iran War

Pakistan is continuing efforts to negotiate a ceasefire between Iran and America, beginning with a temporary ceasefire for 30 days until more permanent peace negotiations can begin A deal has now been drafted, but not signed, for that ceasefire to be extended for a further 60 days. The initial impact of the ceasefire has been to bring the price of North Sea Brent oil back below $100, but there are doubts that it will be sustained. In our view the price of Brent is likely to remain high until at least the end of this year. Hundreds of ships are still waiting to pass through the Strait of Hormuz. The conflict is linked to Israel’s attack on Hezbollah in Lebanon which is on-going. Right now, the Strait remains effectively closed. As the market adjusts, Iran’s influence will decline, so they need to strike a deal sometime this year. Trump is also motivated to bring the price of gasoline down before the mid-term elections.

Ukraine

In our view, Ukraine is steadily gaining the upper hand in its war with Russia mainly because of its drone technology which appears to be well ahead of Russia’s. The ability to strike targets deep inside Russia has effectively curtailed the money from Russia’s oil industry which it was using to fund the war. At the same time Ukraine has begun to make incremental gains on the battlefield, using a combination of unmanned ground vehicles and overhead FPV drones. Since Putin’s dismal 9th May parade, the opposition to his war with Ukraine appears to be gaining momentum inside Russia. His ability to conduct a further conscription to replace losses on the frontline seems to be doubtful.

As Putin’s situation becomes more desperate, he has been casting about for alternative ways to gain some initiative including his recent visit to China and more recently the idea of drawing Belarus into the war. President Zelensky had talks with Sviatlana Tsikhanouskaya, the exiled Belarusian opposition leader. He is clearly concerned about Putin’s efforts to drag Belarus into the war. Putin hopes to open a second front against Ukraine as he loses ground in the Donbas and other captured areas. Lukashenko who is the Russian puppet leader in Belarus has so far resisted entering the war, a move which would be very unpopular with the Belarusian people, but Putin is becoming desperate to regain the initiative on the battlefield and Lukashenko remains one of his last options. Ukrainian intelligence suggests that there has been a build-up of forces along its border with Belarus and that some kind of action in a clear possibility. Lukashenko is very aware of his unpopularity in Belarus and that engaging in a war could easily cause a serious uprising.

China

In the past month Xi Jinping, President of China, has met separately with first Trump and a week later with Putin. Neither Trump nor Putin emerged from their meetings with notable gains and it is clear that, at least where Putin is concerned, the Chinese President now views him as the junior partner. He is very aware of the fact that the Ukraine war has degraded both the Russian military and its economy to the point where it is now relying heavily on Chinese funding to keep the war going. In the long term, we believe that China is intent on taking territory from Russia in the East. There can be little doubt that China has benefited directly from Trump’s foolish tariff policies and entrenched its position even further as the major world trading partner. At the same time there have been joint nuclear exercises conducted by Russia and Belarus – which can be interpreted as further Sabre rattling by Putin whose position is becoming increasingly tenuous.

Political

As the country moves closer to the November municipal elections, the ANC and the DA are trying to put on the best showing that they can. The elections are likely to be fought on two major fronts – corruption and service delivery. In both areas, the DA has a significant advantage. They have no significant track record of corruption while the ANC is generally seen as being riddled with it. Secondly, the DA has established a solid record of service delivery, especially in the Cape Town area, while the ANC’s record in this regard is very bad. This was recently underscored by the DA’s historic win in the Evaton by-elections. Evaton is a pure township ward and the fact that the DA narrowly beat the ANC is seen as very significant for the November election.

Of South Africa’s approximately 60m people, only about 28m were registered to vote in the previous election and of those only 16,2m actually voted. This means that over 11,5m registered voters chose not to vote for some reason. About 20% of the population is between the ages of 18 and 29 and less than half of them are on the voting register. These are the people who are also most impacted by South Africa’s high unemployment rate. The Independent Electoral Commission (IEC) is continuously encouraging people to register or record their change of address - and giving them opportunities to do so. The local government election is now set to take place on 4th November this year, and it is likely to further change the political landscape. Polling suggests that the ANC will lose further ground to the other parties.

A major factor for voters on 4th November will undoubtedly be the municipal system in South Africa which has become a major problem with most of them insolvent and poorly managed. The municipalities derive their income from a government grant, property rates and electricity surcharges. It has now been proposed that, instead of the government grant, they receive part of VAT income, which is raised in their area, which would give them an income which is directly linked to the growth in that area. In our view the main problem with the municipalities is that they have been the main avenue for ANC nepotism and employment of ANC cadres. This has meant that skilled people have been replaced with party members, leading to poor systemic governance. Changing the way that they receive their income is unlikely to change that. [BD15] Most of the municipalities have failed their audits and have been unable to improve services. Irregular, fruitless and wasteful expenditure by municipalities has risen to R268,1bn in the 2024/25 financial year, which is up from the previous year’s R264,1bn. Clearly many South Africans have become disenchanted with the ANC’s continued inability to provide services as well as its on-going corruption.

Fitch Solutions, a subsidiary of the international ratings agency, has estimated that the ANC will get between 30% and 40% of the vote. This perception is supported by the most recent Ipsos polls which show ANC support at around 35%. The DA should benefit from this to some extent because of their track record of excellent service delivery and a lack of corruption.

President Ramaphosa’s Phala Phala case has become a problem for the ANC since the constitutional court referred it back to parliament for an impeachment review investigation. Ramaphosa has been defiant in the face of the decision refusing to resign. Obviously, the decision has exposed the persistent divisions within the ANC. Those who oppose Ramaphosa are calling for him to step down. Resigning would have left him with all his retirement benefits as a past president, but his decision not to resign may now mean that the impeachment hearing will go ahead and he may lose all those benefits. The timing of this development can only be bad for the ANC coming immediately before the November municipal elections. It underscores their reputation for corruption at a critical time. A parliamentary committee with 31 members has been established to determine whether there is sufficient evidence for the impeachment process to proceed. The ANC has 9 committee members while the DA has 5.

President Ramaphosa’s decision to remove Sisisi Tolashe as Minister of Social Development shows the divisions appearing within the ANC. Tolashe was also president of the ANC Women’s League. The Women’s League is an important element of the ANC’s support base. Ramaphosa himself is also now back in the spotlight for corruption over the Phala Phala issue. None of this is good for the ANC’s prospects in the coming election and we predict that they will lose further support.

The Constitutional Court’s confirmation that the “certificate of need” for health professionals is irrational and unconstitutional is a major blow to the National Health Insurance (NHI). The ANC has been trying to downplay the significance of this apex court judgement, but it is definitely a setback for their plan to introduce the NHI. The NHI was always a populist play by the ANC, and it now appears to be bogged down in litigation, if not completely stalled. The Certificate of Need would have allowed the Minister of Health to determine where doctors and other health professionals could practice and where private hospitals could install new wards.

Eskom’s notice to the City of Johannesburg that it will implement power cuts because of the persistent non-payment for electricity throws the mismanagement of the city into sharp relief. City Power owes Eskom at least R5,3bn and the city itself owes a further R1,6bn. This makes the DA’s effort to get Helen Zille elected as mayor of Johannesburg critical. If there are widespread power outages in the city this winter because of Eskom cuts, then the DA might even win a clear majority and not just the dominance of a coalition. The mayor, Dada Morero, has said that he will meet with Eskom to try to settle the matter before the lights are turned off. In addition, the city has a backlog of infrastructure maintenance worth about R220bn. With all of this, the city is technically insolvent and has recently over-spent by agreeing a R3,9bn increase in employee wages and salaries among other expenses. Poor revenue collection has contributed to the problem.

Economy

The Monetary Policy Committee (MPC) raised interest rates by 25 basis points as a direct result of the worsening inflation situation caused by Trump’s war in Iran. The move has been made in anticipation of the longer-term second-round effects of the higher fuel prices. The MPC is still focused on its goal of keeping inflation at the target rate of 3%. The producer price inflation rate (PPI) increased sharply in April to 4,8% from March’s figure of 2,3%. Oil prices have come down a little as hopes of a resolution to the conflict in Iran gained momentum – but the price of Brent is still high. The Reserve Bank is now estimating that inflation in South Africa will reach 4,4% in 2026. The MPC decision to raise rates was split with 4 members voting for the increase while 2 voted to keep rates unchanged. The Bank has also cut its forecast of GDP growth for this year to 1,2%.

The R3,27 per litre hike in the petrol price and the R6,19 hike in the diesel price on 6th May has impacted the inflation rate and, if they are sustained for any length of time, the damage to the economy will get worse. However, it is our belief that the price of fuel will begin to fall quite sharply in the coming months because of the strength of the rand and falling oil prices. The inflation picture has worsened considerably, but fortunately South Africa was in a great position to absorb this blow relatively easily - because of the work that the Reserve Bank did to bring our inflation rate down to 3%. The government has spent R17,2bn to keep the price of fuel down over the two months, but it will not be able to do this indefinitely.

The consumer price index (CPI) rose to 4% in April 2026 – up from March’s 3,1% reflecting the massive fuel price increase because of the Iran war. This is at the top of the Reserve Bank’s new target range of 2% to 4% and may well result in the monetary policy committee (MPC) raising interest rates. The cost of transport rose 4,9% while housing and utilities were up 5,2%. Inflation for the month of April was 1,1%. The MPC will mainly be concerned with the longer-term second-round effects of the fuel price increase as it filters through to other prices. Even though core inflation, which excludes food and fuel costs, was lower at 3,6% in the year to end April, the Reserve Bank will be concerned that fuel prices will cause inflationary pressure. Taxi fares and bus fares have had to be increased by about 10% to recover the costs of fuel. The MPC will have to assess whether the higher fuel prices are likely to persist through the rest of the year when deciding if it is worth hiking rates by 25 basis points at their July meetings. The Treasury predicted growth of 1,6%, but that will have to be revised down. The IMF has already reduced its prediction for SA growth to 1% from 1,4%. Businesses generally are expecting costs to rise and trading conditions to become more difficult. This is impacting on employment levels with retrenchments and business closures.

Payinc’s Index of Salaries which includes 2,1m salary earners shows that in April 2026 salaries declined by 0,6% in nominal terms from a year ago. If the index is inflation-adjusted, then real salaries fell in real terms by 2,7% over the year. The deterioration is due to the sharp increase in the price of fuel and the resultant increase in the inflation rate. South African’s are having to spend more on fuel and so have less to spend on other things. The second-round impact of the fuel price rise has not yet been filtered through to all aspects of the inflation rate, so we can expect the real take-home pay to fall even further before the end of the year. Rising inflation has also had the effect of causing interest rates to rise and more rises can be expected later this year. This will make mortgage bondholders worse off. Altogether South Africans are being forced to tighten their belts to pay for Trump’s war in Iran.

South Africa plans to increase infrastructure spend from the $19bn spent in 2024 to $26bn in 2050 – a 40% increase but off a very low base. The increased spending is planned to cover transport, resources and power, but is generally reckoned by economists to be insufficient to create significant growth in the economy. The lack of planned maintenance over the past two decades has left the country’s infrastructure in very poor condition which has resulted in a low level of investment by businesses. Businesses will generally only invest if they see that the infrastructure is adequate for their needs. The key is private sector involvement. That has turned the electricity generation sector around and is in the process of improving rail transport and ports. It now needs to be applied to the water infrastructure. A major impediment is the poor state of South Africa’s municipalities.

Stats SA reports that electricity generation in South Africa declined by just over 7% and consumption fell by 3,5% in the year to 31st March 2026. Loadshedding has not been a major factor for the past year as Eskom’s supply situation has improved, but unfortunately Eskom’s prices went up again by more than inflation. Eskom supplies about 86% of the country’s electricity, mainly from coal-fired power stations. Independent power producers now generate between 10% and 15% of the country’s power.

The international ratings agency Moodys has given South Africa a positive assessment based on its Central Bank and the management of its economy. Moody’s has the country two levels below investment grade, on a stable outlook. They say that our government debt position remains too high, but that it should improve as reforms are implemented. They approve of the new 3% target for inflation which is expected to reduce the cost of government borrowing in time. Moodys says that the fiscal and monetary management of South Africa means that it is well-placed to absorb the external shock of higher fuel costs due to the Iran war.

Only about 6% of South Africans retire with sufficient assets to allow them to survive without working. The new twin-pot retirement plan is designed to increase that percentage to closer to 20% over time. It does this by allowing participants to withdraw funds from their savings pot – which means that they no longer have to resign early to get access to their savings when they are in distress. By the end of February 2026 almost R80bn had been withdrawn from their retirement plans by 5,6m people – but this has resulted in far more people leaving their retirement savings in place if they change jobs instead of cashing it out. Old Mutual says that the number of people leaving their savings intact has doubled since the system was introduced. Withdrawals are being made because of emergencies, to make repayments of debt or to meet living expenses, but withdrawals no longer require the person to resign their jobs or to take out everything. The two-pot system is another step towards making South Africans a nation of savers rather than spenders.

South Africa is one of 20 countries that have been given free trade status by China. This will give exporters more opportunities to increase exports to China’s growing markets. China is already our largest trading partner and trading with them has been increasing steadily in recent years. We mainly export commodities and agricultural products to China. The change will encourage more Chinese companies to establish production facilities inside South Africa with the objective of exporting back to China. Obviously, the move is designed to enable China to benefit from Trump’s absurd tariff policies by improving trade relations with countries across the world. South African manufacturing has been declining for years, and South African companies will find it difficult or impossible to compete with Chinese manufacturers, partly because of the high cost of electricity in this country.

The ABSA purchasing managers index (PMI) strengthened surprisingly in April 2026 to 52,6 from March’s 49 – indicating that manufacturing is once again expanding. Business activity and new sales orders were stronger. The additional demand could be coming from people buying up products before they go up in price as a result of the hike in fuel prices. The strength was from local demand, while export demand continued to fall.

The agriculture sector is likely to have a more difficult year this year with higher fuel and fertilizer costs combined with the return of El Nino weather conditions which portend drought conditions. The sector has been a major positive contributor to gross domestic product (GDP) in recent years due to the exceptional rains associated with the La Nina weather conditions. South Africa is no stranger to droughts, but we should expect food inflation to rise together with poverty levels as subsistence farmers battle to produce enough to feed their families. The return of El Nino is now considered to be above an 80% probability.

South Africa’s 8 ports handled 300m tons of imports and exports in the most recent year (2025/26) which is a substantial improvement on previous years. There was a 9% increase in the number of ships calling in at the ports with the motor industry accounting for most of the increased traffic (13,3% gain) because of imports from China and India. Container volumes were up 7,1% because of a 22% surge in citrus fruit exports. Clearly the efforts to improve port functionality are paying dividends, especially at Durban. This obviously has positive ramifications for the entire economy.

The unemployment rate rose to 32,7% in the first quarter of 2026 compared to 31,4% in the final quarter of last year. In the 15- to 34-year-old group the unemployment rate was almost 46%. Obviously, most people will blame the ANC for this situation since they have been running the country for the last 32 years. The figures are likely to have an impact on ANC support in the November municipal elections. In our view, these official unemployment figures do not take sufficiently into account those employed in the informal sector which has become the largest employer in this country.

Manufacturing output which accounts for about 13% of gross domestic product (GDP) increased by just 0,9% in March 2026. This follows February’s contraction of 2,3% and was mainly caused by a decline in food and beverage production. The raised price of fuel and fertilizer means that food costs will continue to rise as the year progresses. Overall, the manufacturing picture in South Africa remains depressing.

Transnet is trying to increase its rail volumes from the current level of about 160m tons per annum to as much as 250m tons per annum. To do this it has identified 11 commercial companies to help it operate its rail network. Agreements will allocate the five rail corridors which Transnet operates. The fact that these companies have been officially identified will help them to raise the necessary funding from banking institutions. Obviously, as the efficiency of the railways improves it will reduce the load on South Africa’s road system and boost the economy substantially.

The local steel industry has been one of the major casualties of Eskom’s persistent above-inflation increases to the cost of electricity. Highveld Steel went into liquidation years ago and ArcelorMittal has now been forced to close its long steel plant. The situation has been exacerbated by the import of cheap steel from China and other Eastern countries. Now finally, the International Trade Administration Commission (ITAC) has approved a range of new tariffs on imported steel products designed to make the local industry more competitive. These tariffs will have the effect of making a wide variety of steel products more expensive locally and hopefully they will protect the jobs of the remaining workforce in the steel industry, which is estimated to have lost about 25000 jobs since 2009. In general, it is not good for the economy to protect local industries from international competition because it causes wide-spread inflation, but there can be exceptions in strategic industries or where the tariffs are designed to protect nascent industries.

The rand

A month ago, the rand was feeling the full effects of the risk-off sentiment following the start of the Iran war. Then it became obvious to most serious investors that the impact of AI was more important than the oil price. Risk-off became risk-on and the rand began to strengthen. Indeed, its strengthening trend ran parallel to the strengthening trend which had been in place last year.

Last week, the rand broke below the lower trendline and reached a new strong point at R16.21 to the US dollar. We fully expect it to continue strengthening and even to break below its previous strongest point (R15.79 on 29th January 2026). Of course, the relative strength of the rand is helping to take some of the sting out of the higher oil price for South African consumers. We expect the local petrol price to begin coming down again in the next couple of months.

Commodities

OIL

There are now hundreds of ships stranded because of the blockade of the Strait of Hormuz. Of those, between 160 and 180 are oil tankers including about 50 very large crude carriers (VLCC). The price of North Sea Brent has come down steadily from its peak of $118 on 30th April 2026. This is partly because of hopes over the US/Iran peace talks and partly because oil is being re-routed and companies around the world are looking for alternative energy sources. Consider the chart:

As you can see from the chart, Brent was in a steady downward trend in the last six months of last year and fell briefly below $60 per barrel in December. The riots in Iran caused the price to move up, but when the bombing by Israel and the US began in March 2026 the price took off and ultimately reached a high of $118 at the end of April. At that point Trump began to realise that the war would not be over quickly despite all his bluster and that gasoline above $4 per gallon was really hurting his MAGA support base. Pakistan stepped in and began to broker a deal which ultimately resulted in the ceasefire which has now been extended to allow peace talks to reach a conclusion. With the mid-term elections just a few months away, Trump is in a very weak bargaining position. To have any hope of retaining control over the Senate (the House will almost certainly be won by the Democrats), he has to get the price of “gas” down.

As far as the economy is concerned, the higher price of oil has caused US inflation to rise and it will obviously reduce consumer spending, but by way of compensation, the US is also an exporter of oil so the higher prices will have helped that industry.

We expect the oil price to continue to fall as the world economy adjusts to the new reality.

Companies

NEW LISTINGS

Canal+ is planning to begin a secondary listing on the JSE on the 3rd of June 2026 with a value of over R50bn. The listing will involve 991,9m shares at a value of 412c. The shares’ code will be CNP. Canal+ is already listed on the London Stock Exchange (LSE). Canal+ is a 40-year-old French channel TV provider which has grown into an international media giant in Europe, Africa and Asia. It has 18 million subscribers in 12 countries. The company acquired and then delisted Multichoice last year. In our view, this will become a massive institutional share and a rand hedge.

TSIKO – A rail operating company is looking to possibly list on the JSE following its win of more than half of the rail contracts offered by Transnet to private companies. The company is looking to raise capital for “long-term institutional and industrial impact” according to the Business Day and it intends to have operations in other African countries. The contracts begin in September 2027 and the CEO, Pregasen Naidoo, says the company will begin operating immediately by transporting various base metals and minerals such as chrome and coal as well as agricultural products like sugar. The Tsiko subsidiary Barberry already manages 15 rail sidings in South Africa. Its objective is to acquire 60 locomotives and 2500 wagons.

OMNIA

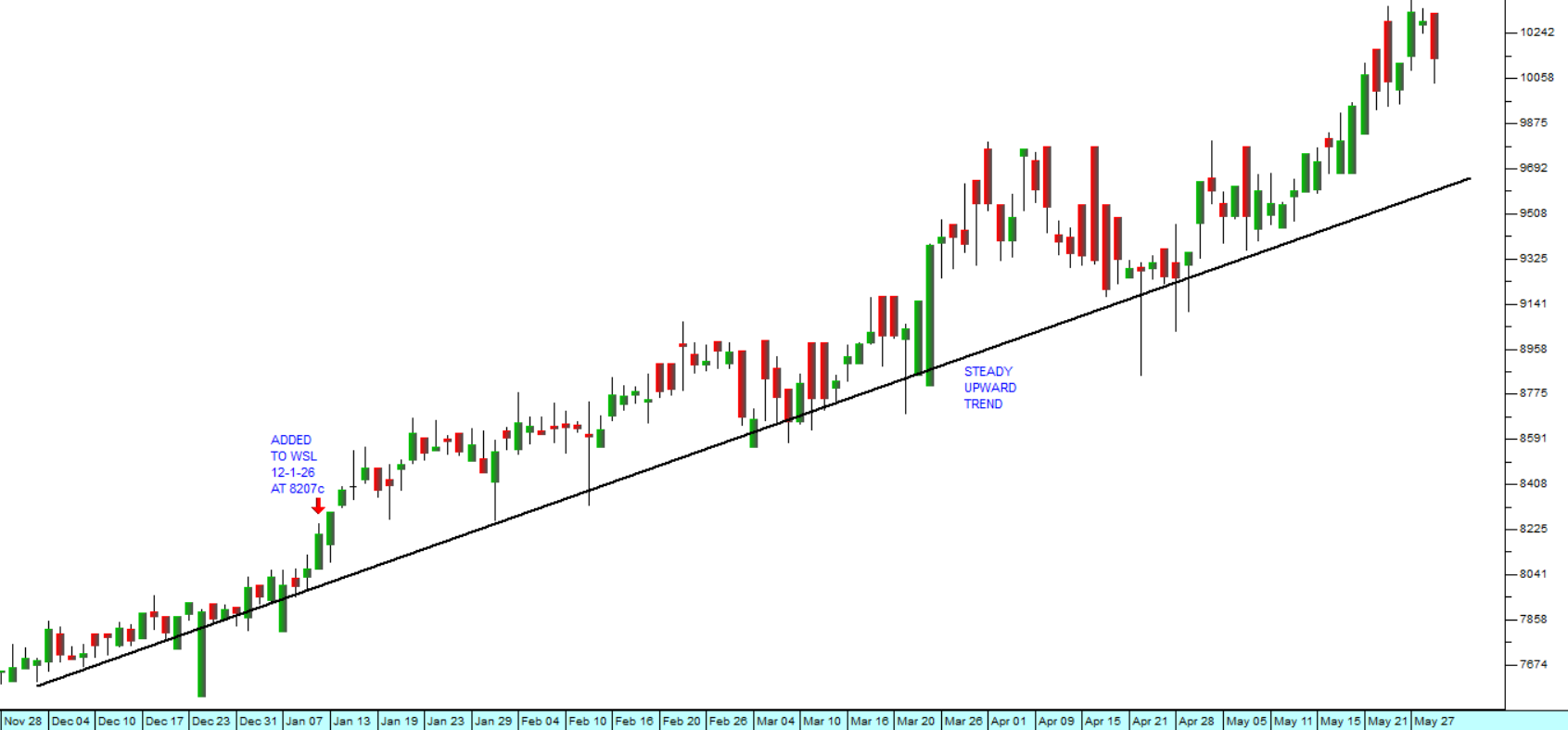

Omnia is a diversified chemicals company supplying products to the agricultural, chemicals and mining industries in South Africa and 48 other countries. Six years ago, it appointed Seelan Gobalsamy as CEO and he is responsible for the company’s turnaround and the significant improvement in its balance sheet. The crisis in the Strait of Hormuz has meant that some of the key raw materials which Omnia relies on to produce fertilizers and explosives have been in short supply on world markets – but the company has assured analysts that it has adequate supplies. It can therefore benefit from the higher prices which explosives and fertilizers are commanding since the war in Iran began. Consider the chart:

In a trading statement for the year to 31st March 2026 the company estimated that headline earnings per share (HEPS) would increase by between 17% and 23%. The chart shows the progress of Omnia shares since the beginning of this year. It has been trending up steadily and was added to the Winning Shares List on 13th January at a price of 8207c. It has subsequently climbed to 10142c – a gain of 54% in 127 days. We believe it can go higher.

BALWIN

Balwin is a property developer that was in a downward trend until October 2024. At that point the share was trading at a fraction of its net asset value (NAV), and we recommended that investors pay attention to it. A new upward trend began in April 2025, and the share was added to the Winning Shares List (WSL) on 26th August 2025 at a price of 269c. It has subsequently risen to 414c – a gain of 70% in 9 months. Consider the chart:

The chart shows the steady upward trend of this share. Recently the share has jumped up on the announcement that the company has received a firm offer from Bidco. This is probably a result of the share still trading well below its NAV and therefore representing very good value.

LEWIS

Lewis is an old favourite of ours and was first recommended by us way back in September 2020 immediately following the COVID-19 crisis at a price of 1772c. It was subsequently added to the Winning Shares List (WSL) on 1st December 2023 at a price of 4150c, mainly because it was at the bottom of a correction. It has subsequently risen to 8810c, and we believe it can go higher. Consider the chart:

Lewis is a retailer of furniture and white goods mainly to the lower income groups. The company has become a master of managing its debtors' book and at making solid strategic acquisitions. In its latest results for the year to 31st March 2026 the company reported revenue up 11,1% and headline earnings per share (HEPS) up 18,3%. The company opened 58 stores in the year bringing its total to 976 and its debtors book grew by 15,2% to R9,2bn. This is a share which is benefiting from the reforms being made in the South African economy by the government of national unity (GNU) and by our low inflation rate. The current downtrend has been caused by the increase in the price of fuel, and we do not expect it to last long.

Southern Sun Limited

Southern Sun hotel group operates 95 hotels and resorts across South Africa, the broader African continent, the Seychelles, and the Middle East. It has been impacted by major geopolitical events beginning with COVID-19 and including the wars in Ukraine and now in Iran and, of course, Trump’s erratic tariff policies. In its latest financials for the year to 31st March 2026 the company reported income up 9% and headline earnings per share (HEPS) up 20%. The share has been in a steady upward trend since forming a solid support base in 2020. Consider the chart:

We added it to the Winning Shares List (WSL) on 17th May 2024 at a price of 555c. It has since risen to 1013c – a gain of 82% in two years. So, this is a solid steady performer, but not very exciting. It should continue to perform well.

4 SIGHT

This company specialises in investing in 4th Industrial Revolution companies and technologies. The first industrial revolution is seen as that which was involved in mechanisation with water and steam power, the second came about when products were mass-produced, the third was the advent of computers and automation and the fourth is what are called cyber physical systems such as cloud computing and the internet of things. We first saw potential in the share back in the second half of 2023 when it broke out of a sideways pattern that it had been in for a while. We added it to the Winning Shares List (WSL) on 4th August 2023 at a price of 31c. It then shot up to a high of 110c over the next 4 months before settling back into a new sideways pattern with support at about 60c. Now it appears to be finding new traction and perhaps increased institutional support. Consider the chart:

In its results for the year to 28th February 2026 the company reported revenue up 16,3% and headline earnings per share (HEPS) up a whopping 46,1%. In our view this share is proving its management expertise and its capabilities. It is simply a matter of time before it begins to gain further institutional interest.

Follow-up

STEFANUTTI (SSK)

This share has been on the WSL since 22nd June 2024, and it has performed very well. In the past two weeks the share has been falling back on profit taking. We regard this as a buying opportunity.

The construction sector has been gaining some momentum with the government’s announcement of major new infrastructure spend programs. We believe that Stefanutti is well positioned to take advantage of any construction work that becomes available.

← Back to Reports