The Confidential Report - April 2026

Iran War

At the last Confidential Report on 4th March 2026, Trump’s Iran war was just a few days old and consisted mostly of American and Israel bombing key military targets inside Iran and killing Iran’s leadership. Since then, the war has progressed into a very expensive stalemate where Iran has rapidly replaced its fallen leadership and effectively closed the Strait of Hormuz. This has pushed the oil price to above $110 per barrel while America now has to consider the dangerous step of putting boots on the ground.

There is little doubt that Trump did not think carefully about the ability of Iran to close the Strait of Hormuz before he decided to start the war. The strait is very narrow and difficult to protect. To take a convoy of ships through there would require air-defence destroyers operating along the Iranian coast and taking down any missiles and drones that were fired at passing shipping. It would also require air support to destroy any targets inside Iran that could fire at shipping. The alternative would be to use the pipeline between Abqaiq and Yanbu on the Red Sea. Unfortunately, that pipeline cannot carry the amount of oil required and it still leaves the problem of getting the oil out of the Red Sea.

The oil then has to go out though the Suez canal, which is too shallow to take very large crude carriers (VLCC) or ultra large crude carriers (ULCC), or out through the Bab el-Mandeb strait which can be attacked by the Houthis who are an ally of Iran and have now apparently joined the war on Iran’s side by launching attacks against Israel. About 15% of all the global trade goes through the Bab el-Mandeb strait which the Houthis can easily close off. This would effectively give Iran a second stranglehold on world trade and pile even more pressure on Trump.

Then there are the attacks on America’s KC135 tanker aircraft located in Saudi Arabia at the Prince Sultan airbase. These tanker aircraft enable US fighter jets to refuel in midair – which then allows fighters to make more sorties without returning to a base to refuel. Early reports indicate that in the latest attacks Iran may have destroyed 3 of these refuelling aircraft and damaged others. If this turns out to be true, then it is undoubtedly Iran’s most effective strike so far against America.

An interesting result of all this is that the new Chairman of the Federal Reserve Bank, Kevin Warsh, may have to hike interest rates in America as his first act when he takes office in mid-May 2026 – which is exactly the opposite of what Trump has wanted to do.

Trump and the Republicans face the mid-term elections on the 3rd of November 2026 – in just over seven months. Early indications are that they could easily lose both the House and the Senate. Early in 2026 the betting markets in America had odds of 80% that the Republicans would retain the Senate in November. With the latest developments in the Iran war that Senate is now seen as 50/50 bet – in other words, it is a toss-up. The $4 per gallon cost of petrol in the US is clearly hurting the Republicans at every level and they now desperately need a resolution to the Iran war to retain their narrow 53-47 margin in the Senate.

At the same time, despite Trump’s statement to the contrary, the possibility of a peace deal with Iran appears very remote. The new Iranian leadership under the slain Ayatollah’s son is even more hardline and extreme than the previous leadership. Iran has a massive stockpile of drones which the American and Israeli air strikes have been unable to completely locate and destroy. Estimates are that they still have two-thirds of their stocks. This means that bringing ground troops into the war will inevitably result in a steady flow of body bags going back to America. And yet ground troops are apparently the only practical way that the Strait of Hormuz could be re-opened to traffic again.

Obviously, the price of oil is now causing several mitigating effects around the world. The existing oil producers are all beginning to pump and export more oil while the move towards renewable energy, particularly solar, is receiving a massive boost. In effect, the world is being forced to reduce its reliance on oil much more quickly than it had planned to do. The shift away from oil will, however, take time and in the short term the oil crisis will persist. It will almost certainly not be satisfactorily resolved before the critical November US elections. Trump is faced with Hobson’s choice – a humiliating withdrawal from the war that he started, or a costly and dangerous escalation. He is very aware that if the Republicans lose both Houses, he may possibly be impeached. Then, reduced to just being a US citizen, he would have to face an array of criminal and civil consequences.

So, the tankers and other commercial shipping continue to pile up near the Strait of Hormuz. The war in Ukraine has shown that control over a corridor at least 30km wide along the Iranian coast of the Strait will be needed to ensure that shipping in not subjected to constant drone and missile attack. In our view, that could only be achieved by land forces. In the meantime, Trump is having to face the consequences of high oil prices at home and the impact which that it is having on his popularity. The recent attack on Kharg Island followed by Iran’s attack on the Qatar gas plant takes the war to a new level and may make the possibility of peace even less likely. Both Trump and Iran have been exchanging threats and ultimatums making markets very nervous. Over 2000 people have so far been killed, most of them in Iran with more than a dozen American casualties. The price of gas in Europe has risen by 35% and the price of North Sea Brent remains stubbornly above $100.

Iran is at least considering the latest peace proposal by America and has not rejected it out of hand. Pakistan is trying to broker a peace deal between the two countries, and the 15-point plan is part of that. According to a senior Iranian official the peace talks, if they occur, could be held in Turkey or Pakistan. Oil prices fell slightly and stabilized for a few days because of the peace initiative, but in our opinion the hardline Iranian government clearly has the upper hand because of its stranglehold on the price of oil – at least in the medium term.

There have been a number of other direct impacts of this new war. Many shares on the JSE, especially banking shares, have fallen sharply in response and the rand has fallen back to over R17 to the US dollar. The fall of the rand combined with the rise in the oil price means that fuel prices here have risen sharply (as much as 26% from the 1st of April 2026) and, if sustained, that will have a knock-on impact on our inflation rate. Fortunately, our fiscal position and especially our inflation rate are in a good position to withstand this type of external shock. The new leader in Iran, Mojtaba Khamenei, has vowed to keep the Strait of Hormuz closed to sea traffic and to force the international price of oil above $200 per barrel.

The probability of a further rate cut here in South Africa has also had to be put on hold with ramifications for GDP growth. There may even have to be an interest rate increase in the coming months if the situation persists. Obviously, the rising oil price has been benefiting shares like Sasol which we added to the Winning Shares List (WSL) on the 19th of February 2026. Paul Hanratty, CEO of Sanlam, has warned that if the war continues and oil prices remain elevated it would have a devastating impact on the SA economy. We are not fully in agreement with this. We believe that while the impact will certainly be negative, our economy is fairly well placed to absorb the immediate impact. We also do not believe that oil prices will remain high for long, mainly because we see Trump being forced to back down at some stage.

One of the consequences of the higher oil price will be a sustained drop in consumer spending as consumers worldwide are forced to allocate a larger percentage of their budget to transport and other oil-related expenses. The medium-term impact of this will be to reduce world gross domestic product (GDP) and hence international trade. The prices of export commodities will inevitably come down, including the raw material exports which the South Africa economy is dependent on. Combined with higher local fuel prices this could be sufficient to put our economy into a recession.

So now oil has become the most important commodity in the world for the moment. Consider the chart:

This shows that prior to Trump’s ill-advised war with Iran and the closure of the strait of Hormuz, the oil price was declining steadily. It was testing support at the $60 per barrel level. Now it is approaching double that price – and all because of the Israeli/American intervention. This is one problem that Trump definitely cannot blame on the Democrats because he is the indisputable cause of it.

Precious metals have already come off their highs in anticipation of a world recession. Notably, Bitcoin has also fallen back to below $66000, showing that it is not in any way a hedge against political risk.

America

In our view, the war in Iran cannot be resolved by Trump and the current US administration. If Trump were no longer President, then there would be a possibility that his successor, Vance, could possibly negotiate a resolution. So, we believe that the price of oil will remain high for the immediate future - which is highly negative for stock markets around the world. However, most of that negativity has already been discounted into share prices. What is interesting is that all this chaos has only brought the S&P down by 8,86%. The reason for that is that it is being countered by the on-going positive news about the productivity gains resulting from artificial intelligence (AI).

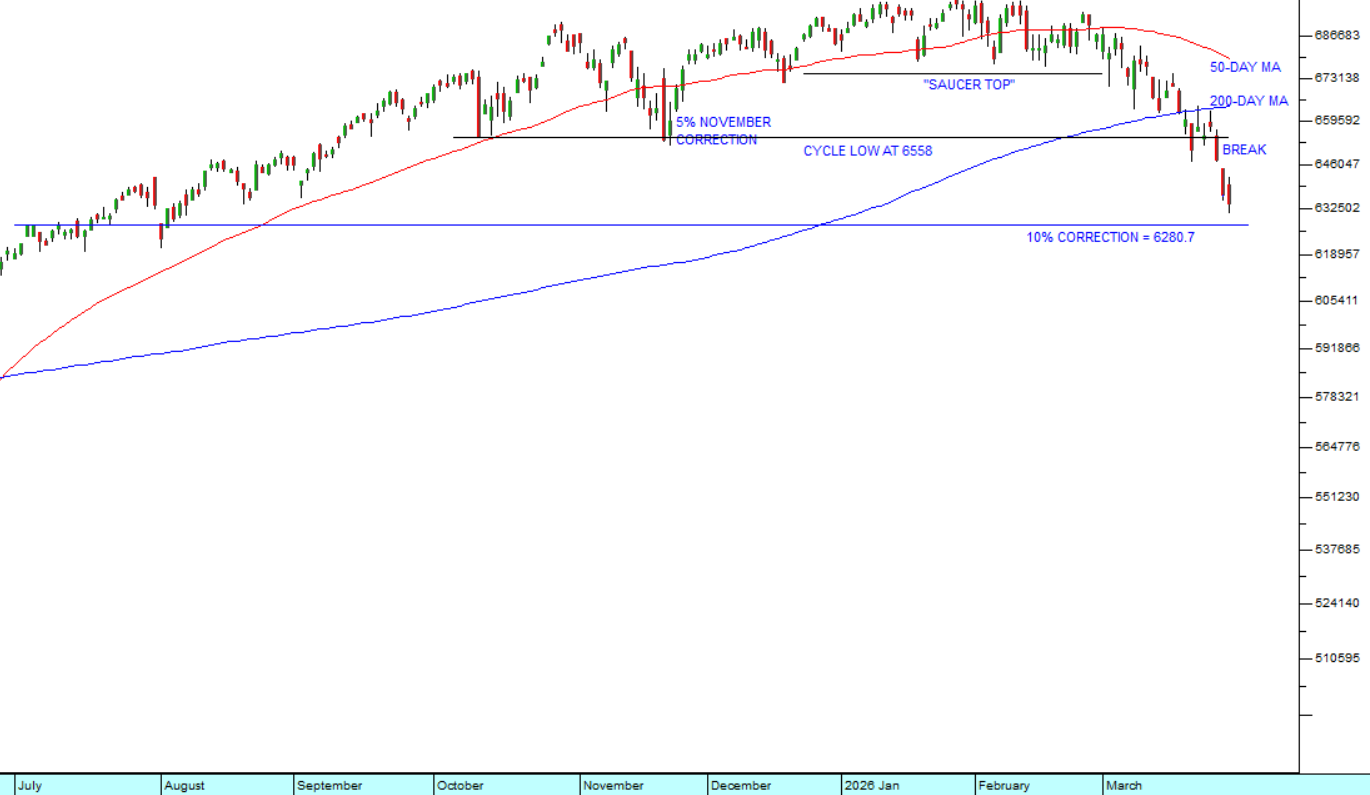

The chart below shows the progress of the S&P500 index from August last year to date. As you can see, the index has completed what technicians call a saucer top formation, part of which was a relatively weak head-and-shoulders formation. You will notice that the previous cycle low, after last November’s 5% correction, created something of a support level at 6558. That was smashed in the last two days of last week when Trump doubled down on his aggression toward Iran and investors began to realise that the war there would go for much longer than was originally expected.

Consider the chart:

I have put in a horizontal blue line on the chart to show where the S&P will be down 10% from its all-time record closing high of 6978.6 on 27th January 2026. If it falls below that level (6280,7), the downward trend will officially become a correction. Given the sharp rise in the oil price, it is very surprising that the S&P has not fallen further and faster. The JSE, for example, has already fallen 13%. In our view, AI is a major positive force in the market, and it is countering the effect of the falling price of oil. These two primary forces are battling it out for dominance in the market, and we believe that in the end AI will prevail.

Artificial intelligence is having a major impact on the US jobs market with many large companies announcing layoffs. Meta is planning to retrench 20% of its staff and Amazon has already laid off 16 000 employees. Nike has laid off 775 staff while Morgan Stanley has cut about 3% of its workforce. Judging from the jobs numbers, these layoffs have been absorbed by other parts of the economy indicating that the effect of AI at this stage is a massive restructuring rather than the cause of a significant loss of jobs. This supports our view that the medium-term impact of AI is going to be one of massively increased productivity rather than a collapse of the labour market.

The price of gas (petrol) in America is a major problem for MAGA supporters. Some, who voted for Trump on three separate occasions despite the fact that he is a convicted criminal, a rapist, closely tied to Epstein’s child porn ring, motivated an insurrection and that he tried to subvert an election, have now decided that $4 petrol is the last straw. Those same MAGA people are turning against him because since he started the war with Iran, the price of petrol in America has gone up by more than $1 per gallon. In our view this might just be the one thing that topples him from power.

The SAVE America Act supported loudly by Trump is struggling to get through the Senate. Trump has urged Republicans to support the Bill on the grounds that it will deliver a guaranteed win for them in the November mid-term elections. The Bill requires voters to prove their identity when they register to vote. This means that they will need either a valid passport or birth certificate to register. Other forms of ID such as a driver’s licence or ID document may be insufficient. The irony is that the Bill, if passed, may actually benefit the Democrats because a much higher proportion of rural voters do not have passports while people with higher education who typically have passports tend to support the Democrats.

Ukraine

There can be little doubt that Ukraine is steadily winning the drone war against Russia. With drones now being produced at factories inside European countries where Russian cannot touch them and with European funding, Ukraine is gradually gaining an edge. Their technical expertise and innovation have allowed them to produce drones that can strike almost any target inside Russia at will. Ukraine’s new technologies have enabled them to expand the kill zone to about 150 kilometres from the frontline, which has made it almost impossible for the Russians to amass weapons or troops for any kind of strike. At the same time Ukraine is becoming less and less reliant on imported weapons. In a single year they have moved from producing just 46% of their requirements to producing 82%. This is a monumental achievement which is giving them greater dominance in their war against Russia.

This has had the effect of stalling the planned Russian spring offensive before it even got started. Russia has found it very difficult to accumulate troops and equipment for their offensive. In the past week, as part of its offensive, Russia has been attacking all along the frontline but has taken thousands of casualties. In the first week they lost about 6000 troops, killed or wounded, without gaining any ground at all. At the same time, in February 2026, Ukraine took back, for the first time, more territory than it lost in the war.

Obviously, the spike in oil prices following the start of the Iran war is a boost for Putin and Russia, but that will take time to directly impact the war. In the meantime, Russia is shutting off access to Telegram which will deprive 90 million Russians of their access to the Internet. There are already protests inside Russia about this. There is now no mobile internet in Moscow and St Petersburg. Russians in these cities cannot even access their banking apps – and the loss of Telegram is a major problem for the frontline troops.

In a demonstration of the superiority of its drone technology, Ukraine has now struck the Primorsk and Ust-Luga oil terminals in the Baltic Sea in effort to prevent Russia from capitalizing on the higher oil price. At the same time, it has hit the Kirishi oil refinery south of St Petersburg and destroyed an ice breaker ship in port. These strikes signify a major shift in the war and threaten Russia’s remaining export avenue through the Baltic Sea, preventing it from loading oil onto its shadow fleet. Ukrainian drone strikes have now prevented about 40% of Russia’s oil exports according to Reuters. Since roughly 25% of Russia’s budget income comes from oil and gas, these strikes are becoming a very significant problem for the prosecution of the war. Right now, Russia has more-or-less doubled its income from oil due to the higher price resulting from the closure of the Strait of Hormuz and also because of US sanctions being lifted. The Ukrainian drone strikes are designed to effectively counter that windfall.

It is clear that Russia will soon be forced to conduct another mass mobilization if they want to continue this war. Russia has been losing about 35 000 soldiers a month on the frontline, most of them to drone attacks. This means that they are now losing troops faster than they can replace them. It seems highly likely that after the 9th of May WWII Russian celebrations, Putin will announce another conscription to put at least 300 000 more men into the army. These would be men who have so far resisted the temptation to take Putin’s massive signing up bonuses. If we are correct, this new conscription will be a very unpopular move and will undoubtedly cause massive protests throughout the country. Perhaps this is why Putin is trying to close internet access so that protestors cannot use channels like Telegram to organize protest rallies. In our view, Putin is beginning to lose control over the general population despite all his repressive measures.

On the night of the 24th of March 2026, Russia launched 426 missiles and drones into Ukraine. Ukraine managed to intercept and destroy 92% of these before they could hit their targets. Unfortunately, 33 managed to get through the defences and found their mark – apartment buildings, private houses, shops and motor vehicles. This has become Russia’s only effective means of attacking Ukraine and the Ukrainians are slowly developing technologies to counter it. Then on 26th March Russia sent 556 drones and Ukraine was able to shoot down 97% of them.

Russia launched its spring offensive on the 17th of March 2026. They lost 1710 troops on that single day in what has been described as a “turkey shoot” along a 100-km front in the Donetsk and Zaporizhian regions. They were mostly taken out by SBS or Magyar drones. This shows how the war has changed dramatically since Russia’s previous spring assaults. The Russians did not take a single square meter of territory this time.

SA Political

The arrest of three of the highest ranked police officers and 11 other senior police officers will come as no surprise to the public at large. Most people are aware that the police force in South Africa is corrupt at almost every level. Certainly, we are all very aware that they are very ineffective at the job of policing in the country and preventing crime. The President is now forced to appoint someone in an acting role until this matter is resolved. It is also interesting that in this matter, Vusimusi Matlala is being held without bail, indicating the seriousness of the crimes that he is accused of. The others have been granted bail pending the hearing. It is also notable that these arrests come immediately after the appointment of a new head of the National Prosecuting Authority (NPA). Obviously, the level of crime in South Africa has been a major impediment to business in the country as well to foreign direct investment (FDI). An example of the ineffectiveness of policing in this country is the murder of Chinette Gallichan in a daytime hit in downtown Johannesburg. It has all the trademarks of an organized crime assassination. She was representing Sibanye in a labour dispute matter. The police are investigating, but no arrests have been made.

America is deliberately trying to exclude South Africa from international forums such as the G20 and the G7. Last year South Africa chaired the G20. This year it is chaired by America and South Africa has not been invited. Now South Africa has also been excluded from the G7 which is being chaired by France this year, probably because of pressure from America. The Trump administration has been unhappy with South Africa’s supposed bias against and treatment of Afrikaans farmers. South Africa’s membership of the BRICS alliance and its relationships with Russia and various Middle East countries have also not helped. In any event this latest exclusion from the G7 meeting shows that the ANC’s stance on foreign policy could have a potentially negative impact on the economy.

South Africa has about 420 government departments and the Auditor General has just reported that only just over one third of them achieved clean audits in the year to the 28th of February 2025. This is a very slight improvement over last year, but still a horrendous figure. However, fruitless and wasteful expenditure was down sharply at R1,4bn from last year’s figure of R3,5bn and there were 161 material irregularities. Notably, those departments that did achieve a clean audit only account for about 12% of the total national and provincial expenditure. This shows the extraordinary degree of corruption and mismanagement which currently exists within our government.

Economy

As expected, the monetary policy committee (MPC) has kept interest rates on hold instead of reducing them because of the massive hike in fuel prices as a result of the Iran war. The governor of the Reserve Bank, Lesetja Kganyago, warned that the inflationary outlook had deteriorated and that interest rates would probably remain where they were for the rest of this year. He says that fuel inflation would be as much as 18% in the second quarter of 2026 causing inflation this year to reach 4%. The MPC believes that the sudden hike in energy prices will be gradually unwound in the coming months as businesses and consumers around the world adjust to higher oil and gas prices. If the oil price does not come down, it may be necessary to increase interest rates later this year.

With the spike in oil prices and the weakening of the rand since the start of the Iran war, the under-recovery is roughly R4.75 per litre of petrol and R7,75 per litre of diesel. Inflation fell to 3% in February – down from January’s 3,5% - but it could rise to over 4% if the Iran war continues. While this will have a negative impact on consumers and businesses, the country is well positioned to manage such an external shock, even if the government does not step in to offer some temporary relief. There is great pressure on the government to suspend the fuel levy or to substantially reduce it to cushion the effect of the increased fuel prices in April. Right now, the road accident fund and the fuel levy add well over R4 a litre to the cost of fuel in South Africa. The ANC is very aware that the sharp rise in the price of fuel and hence taxi fares will have a negative impact on its popularity in a critical election year – so a mitigation strategy appears likely. In recent years South Africa’s refining capacity has halved, leaving it more vulnerable to the cost of the imported fuel.

Payinc’s net salary index, which includes the salaries of over 2 million people earning between R5 000 and R100 000 a month, was slightly higher in March than in February 2026 – and 2,2% above the same month last year. Obviously, the war in Iran and the sharp rise in the price of petrol and diesel will have a direct impact on the economy and hence on salary levels. Inflation, which has been low and falling, will spike upwards now and continue rising in the coming months unless the situation in the Middle East is resolved quickly and the oil price drops back to the levels it was at before the Strait of Hormuz was effectively closed. PayInc’s index of transactions passing through its system shows that in February 2026 the figure rose by nearly half a percent and is now 3,5% above where it was a year ago. However, the company warns that the war in Iran could easily derail this fragile recovery in the economy by forcing the inflation rate up to 4.4% and pushing interest rates up.

In South Africa the average worker lives about 40km away from his/her place of employment – which means that they spend as much as 40% of their income on transport. At the same time, the cost of petrol and diesel comprise about 4,5% of the inflation rate. The massive hike in the price of fuel from the beginning of April this year will push up the cost of riding in a taxi substantially and force many people to walk. Consumer spending will drop as people spend more on fuel and transport. Overall, the rise in the cost of fuel will cause a further drop in fuel purchases which may impact on the viability of some of South Africa’s 4600 petrol stations.

The Bureau of Economic Research (BER) manufacturing survey of 700 companies in South Africa showed that manufacturing slowed sharply in the first three months of 2026, mainly because of a slow-down in the world economy and export sales following the start of the Iran war. Export sales and prices fell sharply showing South Africa’s vulnerability to external shocks. The drop in confidence impacted on all sectors except transport. The survey follows Stats SA’s report that factory output contracted in January after reporting lower GDP growth of 1,1% in the full year of 2025. The cost of electricity for Eskom’s direct customers increased by 8,76% on 1st April while municipal customers will pay 9% more from 1st July. Both companies and private electricity users continue to invest in renewables to get away from Eskom.

The combined effect of rising oil prices and the fall of the rand back to around R17,10 to the US dollar since the start of the Iran war has the potential, if sustained, to impact the price of food products in South Africa. Right now, the products which are still on supermarket shelves have not been affected, but the longer the war goes on the more likely it becomes that food inflation will begin to rise. This will obviously have a negative impact on the poorest households. The price of fuel is rising rapidly, and this has a direct impact on many agricultural inputs such as the price of fertilizer. Fortunately, due to the Reserve Bank’s efforts to contain inflation, food prices are relatively low and stable, so South Africa is coming off a very low base. It may become necessary for the government to subsidise some food staples.

Manufacturing production fell 0,7% in January month due to weaker performance from wood products, printing and publishing (down 11%) and iron and steel (down 5,7%). Production was down 1,7% in the three months ending 31st January 2026. This comes on top of and contributes to the relatively weak growth figure of 1,1% for 2025. Manufacturing contributes about 13% to gross domestic product (GDP). Obviously if North Sea Brent oil remains above $100 for any length of time due to the war in Iran it will have a sharply negative impact on manufacturing and the SA economy.

Gross Dometic Product (GDP) grew by 0,4% in the last quarter of 2025 – above the third quarter’s 0,3%. This means that growth for the whole of 2025 was 1,1% - which compares with 2024’s 0,5% but is below the Treasury’s estimate tabled in the February budget of 1,4%. The production side of the economy was broadly weaker, which dragged the number down. Into this mix, the war in Iran is likely to have a further negative effect as oil prices spike upwards. The Minister of Finance predicted growth of 1,6% this year, rising to 2% by 2028. This prediction is now in jeopardy due to the external shocks caused by Trump’s latest escapade. If the war is prolonged and the oil price remains high, we can expect much lower growth. The consolidation of the government’s debt will also be negatively affected, and interest rate reductions could be stalled.

Edward Kieswetter, the Commissioner for SARS, says that the illegal industries in cigarettes and alcohol in South Africa are worth between R800bn and R1,2 trillion which is costing the fiscus between R200bn and R300bn in lost tax revenue. He recommends that the President leads a crack-down on these illegal industries. Another similar industry which is having an increasing impact is illegal online gambling. Kieswetter proposes dedicated prosecution teams and courts to process those involved as well as cooperation between various government departments. These black-market activities certainly undermine the rule of law in South Africa and have become an unspoken ratification of corrupt activities in this country.

The President’s State of the Nation (SONA) speech appears to have had a positive impact on business confidence with the Bureau of Economic Research’s (BER) confidence survey showing that it climbed further in the 4th quarter after its climb in the 3rd quarter. It appears that the combination of lower fuel prices, falling interest rates and rising real incomes was having a positive impact on businesses across the country. Trump's war in Iran will have a negative effect, as can be seen in the price of fuel and the Reserve Bank's decision not to reduce interest rates. This year’s budget was much better than last year’s, leading to further business optimism. The strength of the rand has been a positive factor but the rand has weakened on news of the war in Iran.

The FNB/BER consumer confidence index shows that confidence improved slightly in the first quarter of this year, mainly as a result of improved confidence among high-income earners (earning more than R20 000 a month). Middle-income earners (R5 000 to R20 000) also showed some improvement, while low-income earner confidence fell further. The survey, of course, was done prior to the advent of the Iran war and so does not reflect the impact of the sharp rise in the oil price and collapse of the rand that resulted.

The Reserve Bank’s leading indicator rose by 4,8% over the year to end January 2026 and by 0,4% in the month itself. This shows that the economy was on a growth path prior to the start of the Iran war and the jump in fuel costs. The indicator is designed to predict economic activity, and the improvement was driven by the recent increase in commodity prices and the rise in business confidence before the Iran war. If the war is protracted then obviously, economic activity will slow down radically, and commodity prices have already been falling. If, on the other hand, the war is resolved and the oil price returns to where it was, we expect the steady improvement in the SA economy to continue.

The worsening water supply situation, especially in Johannesburg and Durban, is a direct threat to business and economic growth. Johannesburg loses about 35% of its water to leaks while Durban is losing as much as 50%. Business Leadership South Africa (BLSA) says that the problems is water supply are a result of mismanagement, noting that Johannesburg cannot even afford to transport workers to sites to fix water leaks. Only 41 of the 257 municipalities had clean audits in the 2023/24 tax year showing that there is widespread corruption and incompetence. There is an almost complete lack of planned maintenance with politicians opting for short-term fixes in an election year. Cape Town has spent 94,1% of its water and sanitation budget this year compared with the national average of 8 metros which is just 31,5%. This comparison shows the DA’s relative governance and service delivery capabilities.

Our Minister of Electricity, Kgosientsho Ramokgopa, has announced that the government will reduce its tariffs on electricity for smelters in South Africa by 54% to make them profitable again. Out of the 66 smelters we have, only 11 are still operating because of the rising cost of Eskom’s electricity. He aims to have as many as 45 smelters back online by the end of this year. Of course, this means that ultimately, the taxpayer will be subsidizing Eskom as well as Glencore and Samancor.

The 75% tariff imposed on Chinese structural steel coming into South Africa will have the effect of protecting our sole producer of mainline rails in this country. The investigation by the International Trade Administration Commission found that imports had surged by 19-fold in 2024 and that 65% of the steel consumed here was imported. Obviously, their cheaper steel undercut the local industry, but it also provided local steel users with a cheap commodity, reducing their costs and supporting their businesses. The move will make structural steel much more expensive for the government, which has just announced a R1 trillion spend on infrastructure over the next three years. The question should be asked, “How is it possible for the Chinese to produce steel and ship it here for less than AMSA can produce it here?” Perhaps our local steel industry is inefficient.

Parks Tau’s decision to require Chinese importers to produce a certificate of conformity will add a layer of complexity and expense for businesses that import and sell Chinese products in South Africa. The certificate is designed to ensure that imports conform to the SA Bureau of Standards (SABS) requirements that protect local consumers from sub-standard, counterfeit or dangerous products. The ruling applies to hundreds of products from bicycles to gas stoves and plumbing components. Obviously, this will make Chinese imports more expensive for local consumers and give local producers of competitive products an advantage. At the moment all these products are unregulated. China is our biggest trade partner and a fellow member of the BRICS alliance so this could have some foreign relations impact as well. It may also help to reduce the significant trade deficit that SA has with China.

Eskom’s municipal debt position is becoming unsustainable. In an update to parliament, the company has reported that by the end of March 2026 it would be owed R116,2bn and that the figure could rise to over R350bn in the next five years. The debt has increased by 23% or R16bn in the past year alone. The maladministration and corruption at South Africa’s 257 municipalities has directly affected service delivery in many parts of the country. This in turn has had a negative impact on the ANC’s support and could be a major factor in the November elections.

The Post Office’s business rescue practitioners have at last recommended that it be liquidated unless the government is willing to inject the funds necessary to re-capitalise it. Predictably, the unions in the form of COSATU have rejected this finding describing it as “ludicrous” because it will result in 5700 employees losing their jobs. The Post Office is one of those government functions that has been replaced by private enterprise in the form of Post Net and the advent of e-mail and other electronic communications. It clearly does not fulfil any important function in the SA economy any longer.

The closure of the Strait of Hormuz has had the effect that many ships are choosing to go around the Cape resulting in an increase in shipping along the South African coast. Ships are re-fuelling and resupplying at South African ports. The Cape Chamber of Commerce is reporting a 112% increase in diversions. The increase in port activity may be temporary, but right now, at least in the short term, the altered shipping routes are benefiting us and many other ports in Africa.

South Africa’s spending on gold mining exploration has dropped from $900 million in 2006 to just $43 million in 2026 showing the collapse of the industry and the ANC’s efforts to attack the mining industry in this country. South Africa now produces less than 90 tons of gold per annum – which compares with just over 1000 tons in 1970. The effect of this extraordinary underinvestment has been that the country has hardly benefited from the 150% surge in the gold price over the past two years. A large percentage of all the gold ever mined in the world came from the Witwatersrand basin and that is the site of the only new gold mine to be launched in this country for the last 15 years (Qala Shallows). The problem is that it takes about 3 years to bring a new gold mine into operation and by then the gold price could be at any level, making it very risky.

It is an extraordinary fact that South Africans spent as much as R1,5 trillion on gambling in the year to the end of February 2025. Many individuals have come to regard gambling as a way to enhance their incomes or to repay debt – which, of course, is fallacious. Many people on social grants of one sort or another are spending their grant on gambling. The gambling expenditure has already been impacting on consumer spending and has been noted by some of the large retail outlets. Now it is apparently beginning to impact the banking sector with Old Mutual reporting that about 40% of South Africans gamble frequently. The commercial banks now take a person’s gambling habits into account before granting loans. Banks report that gambling generally increases as a person’s debt position deteriorates. Clearly, money spent on gambling is not productive and can worsen the already high levels of poverty in South Africa.

The Rand

At the time that Trump decided to attack Iran, the rand was in a steady strengthening pattern against the US dollar. It has been strengthening for nearly a year from its weakest point at R19,75 to its strongest point at R15,79 – a gain of 20%. There was a key resistance level at R17,50 which had been convincingly broken and became the new support level. Consider the chart:

As you can see the area around R16 to the US$ was a critical area and a triangle formed. This triangle was broken when the war with Iran began. As you would expect there was a rapid move away from risk-on and towards risk-off with international investors dumping emerging market assets and moving into safe havens like the US dollar. The rand weakened breaking out of the triangle – but not as far as you would expect. It was protected to some extent by the underlying pattern of strength which had prevailed since April 2025. So far it has not even penetrated the support line at R17,50 and is showing great resilience.

In our view, the underlying pattern of strength remains in place and will enable South Africa to “ride out the storm”. This strength is entirely due to the progress which has been made by the Government of National Unity (GNU) and the relatively low levels of inflation which have become the norm in this country. The work of the Reserve Bank and Lesetja Kganyago (the Governor) have really made and will make a huge difference to the way we meet this external shock.

We have often said that keeping inflation under control in South Africa is without a doubt the ANC’s greatest achievement in its 32 years in power. Kganyago is, in our view, the unsung hero of the ANC and ironically, the ANC continues to ignore his monumental achievements. If our inflation rate had not been as tightly controlled as it has been, the jump in the oil price and the fall of the rand caused by the Iran war would have devastated the economy. As it is, it will certainly have an impact – but that impact will be far milder than that faced by other emerging market economies.

GOLD

Some investors have become confused about the sharp drop in the gold price since the start of the Iran war. Wars are usually good for gold because they cause investors to seek safe haven assets and gold is the ultimate safe haven. This war is different mainly because of the impact that it is having on the oil price, and world trade. A rising oil price threatens growth worldwide and that has the temporary effect of forcing people to liquidate some of their gold holdings to meet margin calls on other securities like shares.

Generally, when growth stalls the demand for gold tends to stall as well. Add to this the fact that gold was heavily overbought when the war began and you have the recipe for a correction. But that’s all that this is – a temporary correction and therefore potentially a buying opportunity. Consider the chart:

The chart shows the pattern of the gold price over the last five years:

- First the break above $2060 which we reported in our Confidential Report of March 2024

- Then the strong upward trend to new resistance at $3424

- Finally, the break above $5000 per ounce and the triangle formation

This has now been broken by the initial impact of Trump’s war with Iran, but the gold price will certainly recover from its current correction in time. It remains the world’s foremost security asset and should be accumulated on any weakness.

Companies

Property shares have taken a hit from the war in Iran. The property index (J253) has fallen 11,28% in the last month. But prior to that it was in a strong bull trend which began in October 2023 as the sector recovered from COVID-19. We suggest that property shares are probably oversold at this point and that this correction represents a buying opportunity.

In February month alone (before Trump went to war with the Iranians) the index gained 8,2%. Money was pouring back into property as the big institutions recognized that it still had some distance to go to recover from the 2020 pandemic.

We have the following property shares on the Winning Shares List (WSL)

- Resilient added on the 19th of June 2024 at 4842c – now up 64%

- Vukile added on the 7th of December 2023 at 1410c – now up 58,3%

- Redefine added on the 18th of July 2025 at 480c – now up 23,3%

- Growthpoint added on the 31st of May 2025 at 1349c – now up 19,6%

- FTBPROP B added on the 21st of May 2024 at 392c – now up 34,9%

Consider the SAPY index chart:

The property index began to show signs of life in October 2023 and has been trending up since then. Obviously, the pattern of falling interest rates has helped, as has the advent of the government of national unity (GNU) and the strength of the rand.

The war in Iran has been a set-back because it threatens to push interest rates up again and because it undermines the slow growth in consumer spending. In our view, however, this represents an opportunity to get into the property sector if you are not already there – or to increase your holdings.

Property is generally a very slow solid investment that appreciates over time. This makes it far less risky than other sectors on the JSE.

MTN

This company describes itself as a “pan-African mobile operator”. South Africa is its third largest market, but it has operations in many African countries. This naturally increases the risk of investing in its shares because it is subject to the vagaries of African politics and political instability. Despite this it is a highly successful business which is growing steadily.

In its most recent financials for the year to the 31st of December 2025, it reported that service revenue was up 22,9%, data revenue up 37,7% and fintech revenue up 30%. Headline earnings per share (HEPS) rose 67% and the company increased its subscriber base by 5,6% to over 307 million.

Consider the chart:

As you can see, MTN broke up out of an extended sideways pattern at the beginning of 2025 and has been trending up since then. We added it to the Winning Shares List (WSL) on 15th January 2025 at a price of 9729c. It has since risen to 19460c – in other words the share price has doubled in about 15 months.

We believe it still has upside potential.

SASOL

Of all the shares listed on the JSE, Sasol has probably benefited the most from the war in Iran. About 42% of its business still consists of making fuel from South Africa’s coal reserves and it supplies about 30% of our domestically consumed fuel. This fuel is produced at Sasol’s Secunda plant and the Natref refinery. It is the world’s only industrial scale oil-from-coal facility.

In view of this, we added Sasol to the Winning Shares List (WSL) on 18th February 2026 just as the war was beginning. At that time its shares were trading for 12838c. Since then, they have moved up to 21777c – a gain of almost 70% in 38 days. Consider the chart:

While we expect the price of oil to remain relatively high for some time, we believe that it will stabilize and then begin to fall as the world economy adjusts to the closure of the Strait of Hormuz and the war in Iran.

Obviously, Sasol is still substantially a commodity share and hence risky.

← Back to Reports