Mining

12 October 2018 By PDSNET

So gold mining began just south of Johannesburg, where the lip of the sea bed broke the surface, and then progressed towards the south, going deeper and deeper giving higher grades, but becoming progressively more expensive and difficult to mine. By the early 1930’s, it was generally thought that the gold mining industry in South Africa was reaching the end of its economically viable life, but then a new, far cheaper, method of extracting gold from the ore, known as “heap leaching” was invented. This technique gave mining a new lease on life and made it economically viable to mine ore at much greater depths. Today, once again, deep-level gold mining is reaching the end of its economic viability. However, South Africa still has more than 40% of the world’s known underground reserves of gold – but most of it is just too deep to mine economically with current technologies.

The Bushveld Igneous Complex is an extraordinary igneous intrusion, by far the largest of its kind in the world, where molten lava was forced up between layers of sedimentary rock where it cooled and solidified about 2 billion years ago. It has a surface area of 66 000 square kilometers and is shaped like a ragged four leaf clover with its stalk pointing towards Tshwane (Pretoria). It is one of the great treasure houses of the world which includes platinum group metals (PGMs), gold, chrome, copper, nickel, tin, iron, fluorspar and vanadium.

As ore bodies of precious metals became deeper and less viable, base metals and minerals have taken their place as the most profitable mining ventures in this country. Mining technology is always developing and improving, which means that precious metals might once again dominate South African mining at some time in the future.

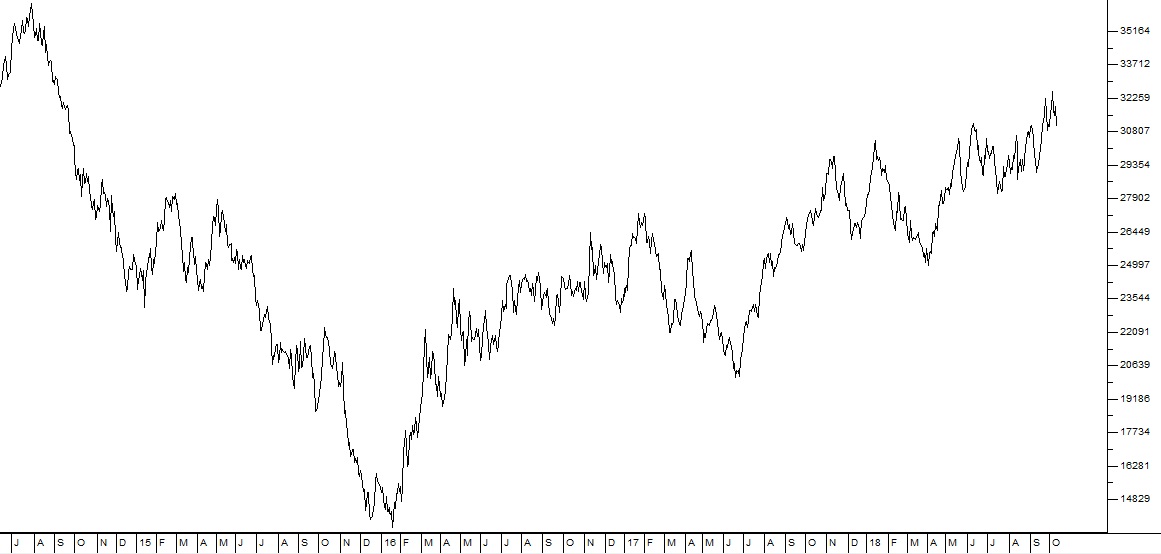

Until the start of 2016, the mining sector was suffering from low commodity prices. But in January 2016, that cycle turned (following a “double bottom”) and the prices of metals and minerals began to rise. Since then, mining companies have been doing better. Consider the chart of the JSE Mining index: