Stadio

5 July 2020 By PDSNETWhen it listed on the JSE, Stadio was one of those shares which was widely perceived to have almost unlimited “blue sky” potential. Riding on the back of Curro’s success and Chris van der Merwe’s (the CEO at that time) reputation, it was thought that Stadio would do as well as Curro, if not better. Like Curro, it was thought that there was a virtually no limit to Stadio’s potential to expand into every avenue of tertiary education. This perception propelled the share to an unheard-of price:earnings multiple (P:E) of over 300 on 4th September 2018 – surpassing even Curro’s December 2015 record of 245.

At the time we suggested that such multiples were simply unsustainable, no matter how good the potential, and advised clients to stay away. Over the next two-and-a-half years, the reality gradually manifested in the share price as it sank back to more reasonable and believable levels.

Most of the very enthusiastic investors of late 2018 eventually gave up on Stadio and took their money elsewhere. But the irony is that Stadio’s “blue sky” potential is still there. There is a massive shortage of high-quality, career-enhancing tertiary education in South Africa. Our state-funded universities and other tertiary colleges simply do not offer the quality of education that they once did – leaving a gaping opportunity for the private sector to step into the gap.

But what has really revived Stadio is the sudden realization that about 80% of its students are educated online. Of its 31000 students, 25000 do not attend any brick-and-mortar campuses. They get their courses online. This has a special relevance in the post-COVID-19 society that we live in today. Thousands of people have lost their jobs and are looking to up-school themselves so that they can earn a living.

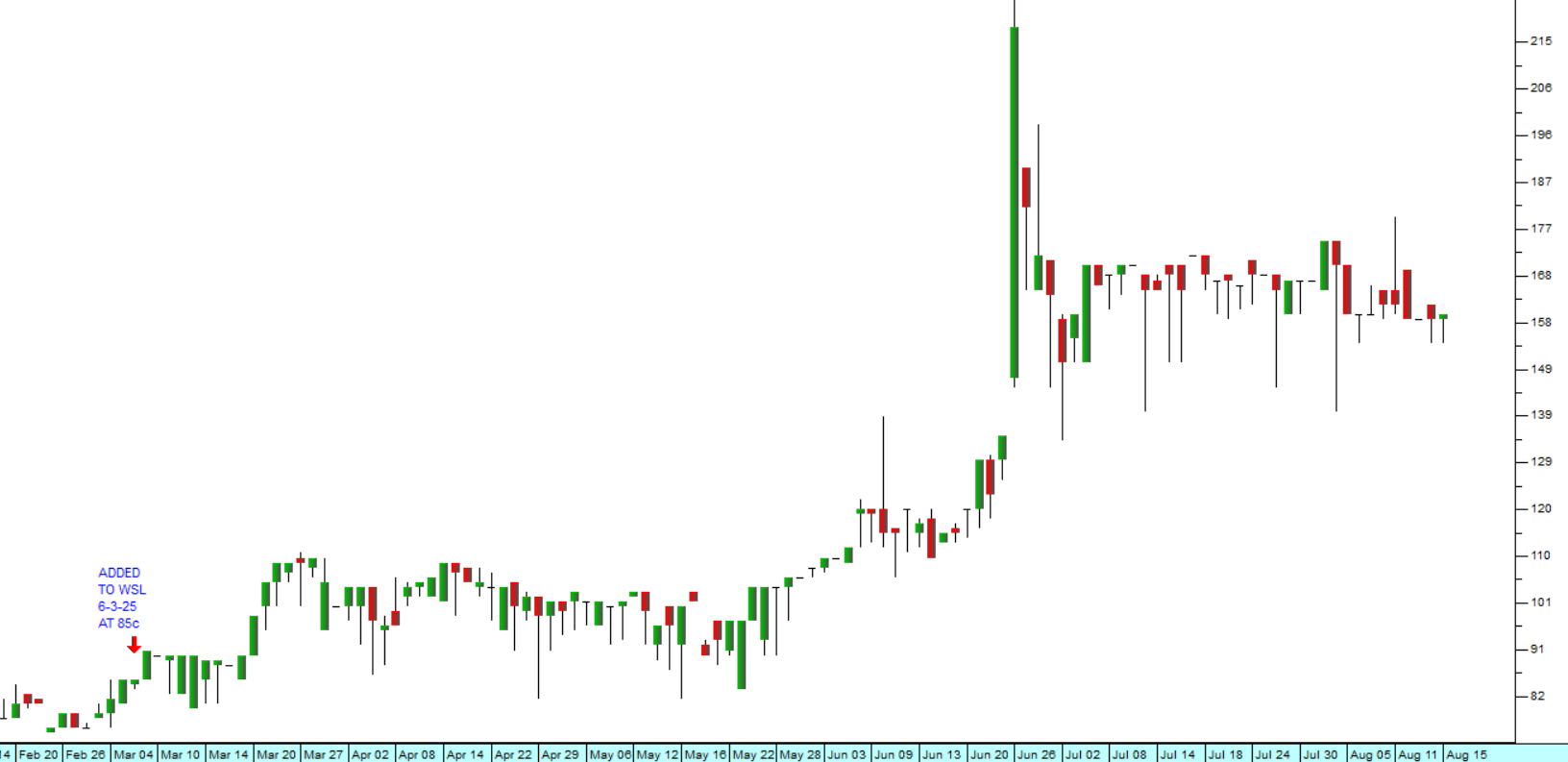

In its recently published trading statement for the six months to 30th June 2020, Stadio reports a sharp increase in the number of students enrolling for its Post-Graduate diploma in accounting through its subsidiary CA Connect. Consider the chart of the share’s price:

Here you can see the extraordinary heights which Stadio reached in September 2018 at a P:E of 300, and how the share drifted down to a more a much more reasonable P:E of around 10 following the initial scare of the pandemic in March 2020. That was followed by the share breaking convincingly up through its long-term downward trendline, a break that was confirmed by its trading statement of 1st July 2020.

We believe that the share, even at a P:E of over 23, is underpriced because it is uniquely positioned to benefit from the post-COVID-19 situation.

DISCLAIMER

All information and data contained within the PDSnet Articles is for informational purposes only. PDSnet makes no representations as to the accuracy, completeness, suitability, or validity, of any information, and shall not be liable for any errors, omissions, or any losses, injuries, or damages arising from its display or use. Information in the PDSnet Articles are based on the author’s opinion and experience and should not be considered professional financial investment advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional. Thoughts and opinions will also change from time to time as more information is accumulated. PDSnet reserves the right to delete any comment or opinion for any reason.

Share this article: