Human Behaviour

20 September 2021 By PDSNETInvesting in shares is about predicting the future. When buying a share the buyer is saying that he expects its price to rise, while the seller, by his sale, clearly has the expectation that it will fall. Of course, only one of them can be right and whomever is right will take money away from whomever is wrong. And the outcome depends entirely on the accuracy of their predictions at the moment when the transaction takes place.

Since the future is inherently unknowable, every investment prediction is made with a degree of risk. Indeed, investment is never about certainties – it is always about probabilities.

It is our considered observation that the prices of shares do not move entirely at random. While they certainly may include a random element, there is an undeniable relationship between today’s closing price and that of tomorrow.

For example, if Anglo American shares close at R560 today, what is the probability that they will trade tomorrow at R1? We think very close to zero. If Anglo shares moved randomly, then they could go from R560 today to R1 tomorrow - and then to R10 000 the next day. A random series can do that, but common sense tells us that Anglo shares can never do that – and so their movement can never be characterized as truly random.

And if they are not random then their price movements must contain patterns. It remains to find the mathematical tools that will enable us to isolate and identify those patterns so that we may use them to improve our probability of being right when we buy or sell shares. Investors call those mathematical tools “technical indicators”.

So, if there are patterns in the movements of share prices, where do those patterns come from? The simple answer to that question is that they are a consequence of the behavioural characteristics of the investors who make up the market. Thus, the humble moving average exploits the fact that human beings generally have difficulty in adjusting their perceptions of value quickly.

If I told you that your house was worth nothing you would have a great deal of difficulty in accepting that – even if I was right. The most traumatic experience is to write off a motor car – because what was worth a quarter of a million rand a few minutes ago is suddenly a useless heap of scrap metal. This difficulty that people have in adjusting their perceptions of value causes share prices to move in broad sweeping trends – and to the extent that they do, the moving average gives profitable buy signal and sell signals.

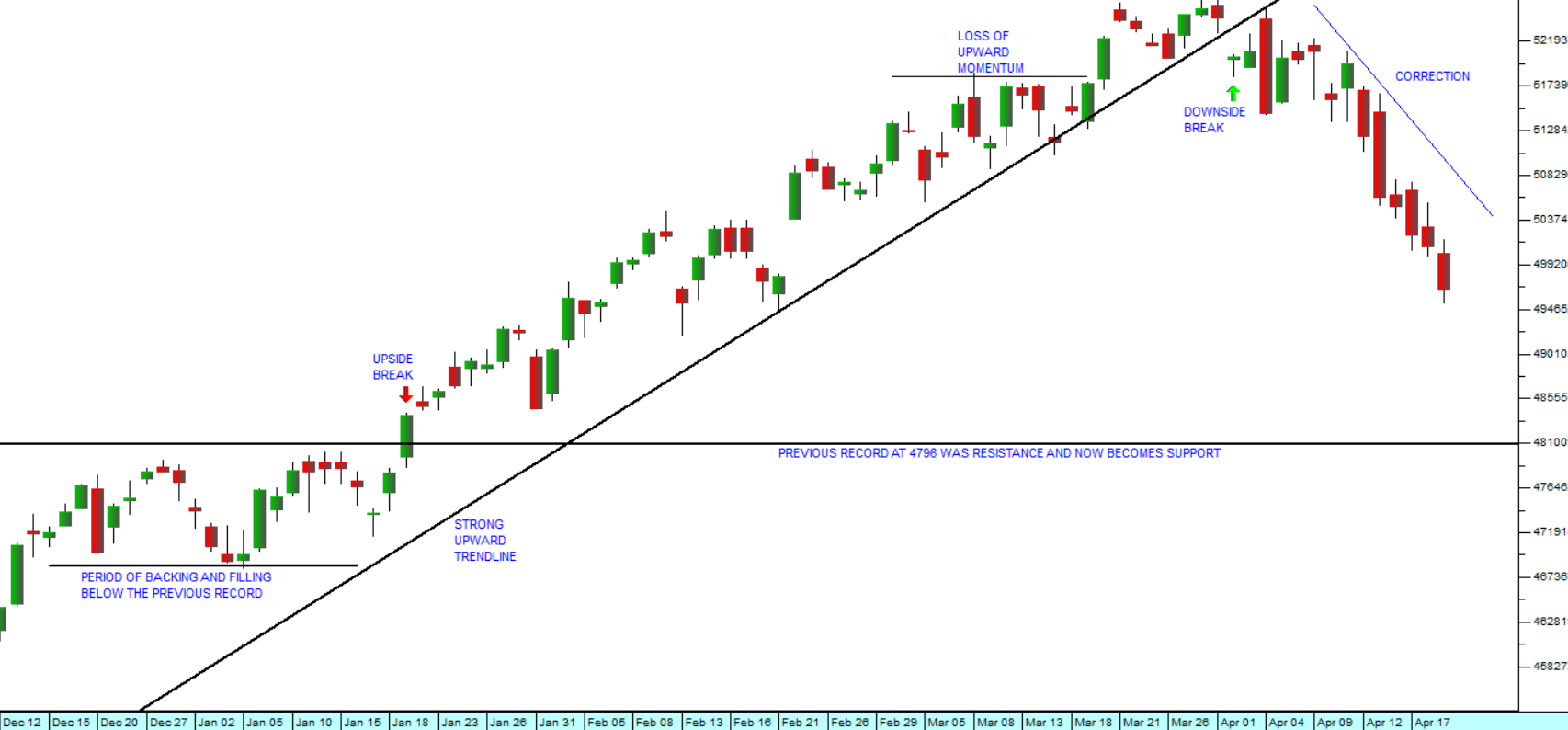

Consider the example of Lewis with a 200-day moving average superimposed:

.png)

You can see here that in the early part of 2020, the impact of COVID-19 took some time to be fully appreciated by Lewis investors. From late January 2020 until the middle of March, Lewis shares drifted down as the extent and import of the pandemic became more and more widely accepted. But Lewis shares had already given a clear sell signal on 23rd January 2020, at a price of 3156c.

In the downtrend that followed they reached a low of 1222c seven months later on 20th August 2020. From that time onwards, the perception that the virus would be brought under control began to grow. On 11th November 2020 the share gave a clear moving average buy signal at a price of 1800c – and it has been rising ever since.

The fact that Lewis is an exceptional retailer that not only survived the pandemic, but actually exploited it to extend its hold over the market was slowly understood by more and more investors. The company is completely debt-free and even now trades on an absurdly low price:earnings (P:E) multiple of just 6,97 with a mouth-watering dividend yield of 6,10%. This means that it still has some distance to run before we would consider it to be “fully priced” – even though it has already more than doubled since it gave that buy signal back in November last year.

We can only think that those investors who are currently selling Lewis do not fully grasp the value of what they are selling – or maybe they bought when it was R18 a share and are happy to take profits now, to more than double their money. Nonetheless, we can easily see the shares of this remarkable company doubling again from current levels – and the moving average is confirming that opinion.

DISCLAIMER

All information and data contained within the PDSnet Articles is for informational purposes only. PDSnet makes no representations as to the accuracy, completeness, suitability, or validity, of any information, and shall not be liable for any errors, omissions, or any losses, injuries, or damages arising from its display or use. Information in the PDSnet Articles are based on the author’s opinion and experience and should not be considered professional financial investment advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional. Thoughts and opinions will also change from time to time as more information is accumulated. PDSnet reserves the right to delete any comment or opinion for any reason.

Share this article: