We have never liked Bitcoin or even regarded it as a true investment. As Charlie Munger famously said about those who buy cryptocurrencies, “...somebody else is trading turds and you decide I can't be left out.” More recently, the esteemed Professor Paul Krugman has linked the price of Bitcoin directly to the political influence and dominance of Trump. He described its value as nothing but “technobabble”.

We have always advised people not to invest in it and to sell it if they had it. We hope that you took our advice. Our main reason for not considering it to be an investment is that it offers no return. It generates no interest, dividends or rent – meaning it lacks fundamental value. So, its value really only exists in the minds of the people who buy it and as they come to realise their mistake, the price will inevitably decline.

At one point there was the suggestion that cryptocurrencies were somehow digital gold, but nothing could be further from the truth. The truth is that the demand for cryptos is much more similar to the demand for tulips in Holland in the seventeenth century. It exists only in the minds of a relatively few individuals who have been swept away by the rapid advances in technology in the modern world. Cryptos lack universal appeal. By contrast, gold has been known and prized by every human being on earth for millennia no matter what their culture, creed or background.

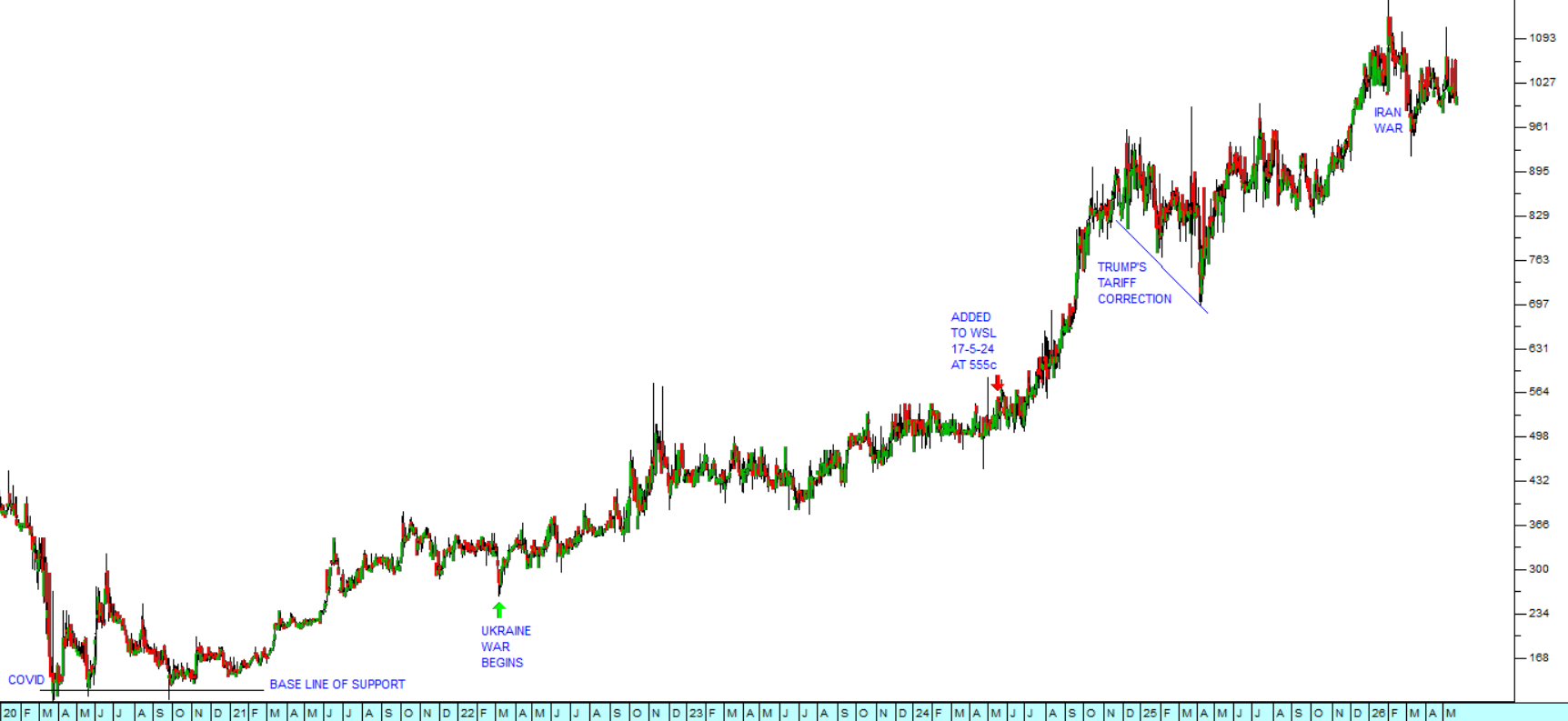

In any event we will let the chart tell the story.

Bitcoin : April 2025 - 12th of June 2026. Chart by ShareFriend Pro.

Bitcoin : April 2025 - 12th of June 2026. Chart by ShareFriend Pro.

The collapse of Bitcoin from its peak in October 2025 has been dramatic. Its value has more than halved through a series of cycles. The cycles are caused by the “stale bulls” who simply refuse to acknowledge that Bitcoin’s popularity is now permanently and irreversibly damaged. The Bitcoin price is falling just as Trump’s popularity and political clout are falling.

The effect of Trump’s ill-advised decision to go to war with Iran and the consequent jump in the price of fuel worldwide can be clearly seen. His popularity has nose-dived. Even hardline MAGA supporters who remained loyal through all his other obvious problems found the jump in the price of “gas” just too much to stomach.

From a technical perspective Bitcoin has broken down through a series of key support levels. Firstly, it found support at $83268 – the cycle low of November 2025 and that was followed by quite a significant “stale bull” rally. The rally came to an end when Bitcoin broke below that support level in February 2026 and then smashed down through the earlier cycle low at $77380 established in April 2025.

When Trump began bombing Iran, a new low point was established on 24th February 2026 at $64 000 and again the stale bulls motivated a rally which took the crypto briefly back above $80 000. However, Trump’s continued unpopularity and the growing evidence that he may be suffering from some kind of dementia has resulted in Bitcoin breaking decisively below $64 000 – which has now become a technical resistance level.

While we see Wall Street recovering from the current correction, we do not see Bitcoin recovering. As Trump inevitably descends into political oblivion, so too will Bitcoin. Already it is an investment sideshow used primarily by organised crime to move money with impunity.

From our very first article on Bitcoin in December 2017, The Bitcoin Bubble, we have always advised investors to stay away from it. Our advice remains unchanged:

“If you have it, sell it. If you don’t have it, don’t buy it”.