The Confidential Report - March 2026

America

Following the 5% correction late last year, and the subsequent new all-time record high the S&P500 index has become range bound. It is moving sideways between its new closing high of 6978.6 on the 27th of January 2026 and a low of around 6758 on the 18th of December 2025. Consider the chart:

This sideways pattern has been caused by investors rotating out of those companies which are seen as vulnerable to the disruptions of AI which may cause layoffs and lower profits. For example,

- Software companies were the first victims of this fear because of the launch of Claude Opus 4.6 by Anthropic which writes software more effectively than programmers can.

- More recently investors have become concerned that financial management companies like Morgan Stanley and Charles Schwab may be disrupted because financial analysis will in future be done by AI. A new tax planning tool can perform the work very quickly and replace tax advisors.

- Then the trucking and logistics business has been impacted by a new technology from Algorhythm Holdings which makes logistics more efficient and threatens to eliminate back-office functions.

- Even the real estate sector has been impacted by technologies which can streamline their business. Investors are rotating out of high-fee, labour-intensive business models viewed as potentially vulnerable to AI-driven disruption.

There can be little doubt that AI is beginning to reshape the US economy at a very deep level. Capital is being reallocated and industries which have been solid performers for generations are being replaced by new AI applications. The market is digesting and assimilating the scope and range of these changes and adjusting its investment decisions accordingly.

While AI appears to be eliminating jobs in some parts of the economy, it may be creating jobs in other areas. The January Jobs figures support this perception.

The US economy created 130 000 new jobs in January 2026 and the unemployment rate was slightly lower at 4,3%. These figures were better than expected by most economists who were looking for 55 000 jobs and an unchanged unemployment rate of 4,4%. The jobs number is a significant improvement on December’s figure of 48 000. Fears that the economy was possibly heading into recession were allayed.

At the same time inflation appears to be under control. The January 2026 consumer price index (CPI) came in at 0,2% for the month which portends an inflation rate of 2,4% per annum. Economists were expecting the inflation number for January to come in at 0,3% so this was a relief for those investors worried about any slowing down of the Fed’s interest rate cutting cycle.

So, the sideways movement on Wall Street reflects widespread investor uncertainty. In our view it will ultimately be resolved to the upside with the S&P making a series of further new record highs.

Look at the impact of this on the JSE Overall index:

The JSE Overall index’s rise to a new all-time record high on Friday last week (128456) shows how investors on our local market view these developments. South African investors seem to have very little doubt as to exactly how the current uncertainty in US markets will be resolved or what the direction of the trend is. We agree with them.

Trump's attack on Iran impacted Wall Street and markets around the world on Tuesday, the 3rd of March 2026, including the JSE, which fell sharply. We do not think this fall will be sustained, and if anything it represents a potential buying opportunity.

Of course, the figures coming out of the US will make the job of the in-coming Federal Reserve Bank Chairman Kevin Warsh easier. He is taking over an economy where inflation is relatively low and there is solid growth. Investors are still trying to figure out exactly how AI will impact the economy. It may be pushing unemployment higher while reducing inflationary pressures.

The Supreme Court’s decision to strike down Trump’s tariffs is further evidence of his declining influence and power in America. Wall Street was generally positive about the development because it will reduce import costs for a number of companies. Trump immediately imposed new 10% tariffs across the world which will be in force for 150 days before they will have to be approved by the US Congress.

We previously drew your attention to Professor Paul Krugman’s assertion that Trump’s influence is mirrored in the collapsing Bitcoin price. Consider the chart:

The downward trend has slowed down with Bitcoin now having found some temporary support at around $65000. This means it has off-loaded a considerable amount of its value in just four months. We agree with Krugman – this is a direct measure of Trump’s declining influence. So, we expect Bitcoin and other cryptos to continue falling in due course.

Nvidia’s results were much better than analysts were predicting with revenue of $68,1bn and earnings per share (EPS) of $1,62 per share. Analysts predicted $65,8bn in revenue and $1,55 in EPS. Despite this, the share price fell 5% on the day – confirming the old Wall Street wisdom that good news which is expected usually causes the share price to fall. In our view, the Nvidia results show that AI is still very much alive and well and driving forward.

The Chinese have been capitalising on Trump’s foolish trade tariffs and policies. They have been negotiating trade deals with countries all around the world. As one Chinese official said of Trump’s policies, “Don’t interrupt your opponent when he is making a mistake”. China has moved to consolidate more than 20 trade deals with a variety of countries impacted by Trump’s tariffs. The EU was amazed when China suggested the prospect of a free-trade deal with them. Tariffs are being negotiated between China and a variety of countries from Canada to the UK, Honduras, Peru, South Korea, Switzerland and, amazingly, Lesotho. The Chinese regard this as a golden opportunity to consolidate their trade dominance of the world. The Chinese economy has a GDP of around $19 trillion while the US has a GDP of about $30 trillion. It is quite conceivable that Trump has opened the way for China, which is running record trade surpluses, to become the largest world economy.

Trump is purportedly making various efforts to derail the US mid-term elections which the polls indicate he might lose. His efforts allegedly include:

- The nationalisation of voting, taking it away from the individuals states and making it a federal issue. The tenth amendment to the Constitution is clear that voting is done by the states and not the federal government.

- He has spoken about cancelling or delaying the elections on the grounds that there is an insurrection or that the country is at war with, for example, Iran. He could invoke the Insurrection Act (of 1807) to say there is a national emergency or a civil war in progress making elections impossible. The individual states will probably hold their elections anyway.

- It is reported that he is considering issuing an executive order to force people to prove their identity before they can vote. Less than 50% of Americans hold passports – which are time-consuming and expensive to obtain. If they are prevented from voting this will sharply reduce the participation on election day. But executive orders are for the executive branch of government and cannot be applied to the individual states.

- He may try to pass a Bill through congress which says that if your birth name is different from your current name then you can’t vote. 69 million women changed their names when they got married and so they would not be able to vote.

- He has tried to stop states from using voting machines or accepting mail-in votes. But there are some states where the only way to vote is by mail. The prospect of masked government ICE officers being deployed to important swing states on election day to harass or intimidate voters is a major concern.

Iran

Trump’s latest war in Iran has, of course, resulted in the oil price rising and has positively impacted on gold. Aside from that, Khamenei must be seen as the third Russian ally to be lost to Putin following the loss of Bashar al-Assad in Syria and Maduro in Venezuela. Russia has been powerless to intervene which shows how much international power it has lost. Putin must surely be concerned about his personal safety in this situation.

People are divided on whether the war in Iran is a good thing. On the one hand there can be little doubt that the Khamenei’s rule was repressive and that can be seen by the crowds of Iranians gathering in both Iran and America to celebrate his demise. However, the attack was made without the approval of Congress as required by the War Powers Act of 1973. This Act was put in place to curb the power of the US President to commit the country to war and Trump has now ignored it for the second time.

On the other hand, President Zelensky can only be happy because Iran has been supplying Russia with tens of thousands of Shahed drones and other missiles which have been used to attack Ukraine.

Ukraine War

If you ever needed any confirmation that Russia is an authoritarian dictatorship, the effort by Russia to shut down the last remaining free communications platform, Telegram, is it. Telegram has 90 million users and is most popular among young people from between 12 and 24 years old. The authorities want Russians to rather use the state controlled “Max” which comes pre-installed on all devices now. But Max allows the authorities to listen to what is being said near to the device on which it is installed – the microphone is always on and the camera will randomly switch on to watch users. This is close to George Orwell’s nightmare vision of “big brother’s watching you” – and Russians are complaining. The FSB gets to read everything you say and to watch what you do. The Russian government now has a “kill switch” which enables them to cut off the internet if there is a revolt against the Putin administration. Coming immediately after Starlink shut down for the Russian army, this also cuts off their one remaining communications mechanism. In our view this will have a materially negative impact on their ability to fight. Already, Ukraine has been taking advantage of it to make some gains on the front line.

The destruction of the southern branch of the Druzhba pipeline by Russia has given rise to a stand-off that has delayed funding to Ukraine. The damage is inside the Ukraine controlled territory and it prevents the flow of oil to Hungary and Slovakia – but it was done by Russia. Now those countries, and especially Hungary are vetoing the 90bn euro aid package agreed by European nations from reaching Ukraine. Hungary is demanding that Ukraine allow Russian technicians in to repair the damage and so restore the flow of oil. The stand-off overshadowed commemorations of the 4th anniversary of the Russian invasion of Ukraine in February 2022. The peace negotiations between Russia and Ukraine have stalled over land issues.

So, as the war enters its fifth year, both sides have sustained significant losses and are exhausted. We think it is unlikely that the war will still be in progress next year. Something has to give.

Political

President Ramaphosa, in his state of the nation (SONA) address stressed the need for unity in the Government of National Unity (GNU) and emphasised that, once appointed to the cabinet, a Minister is no longer working for his particular political party, but for the country as a whole. Partisanship must be set aside. In reply, the outgoing leader of the DA, John Steenhuisen, emphasised the party’s position that the government’s BEE policies must be replaced by merit-based appointments. He pointed to the DA’s Economic Inclusion for All Bill as the way forward. But the ANC and Ramaphosa have staked their political future on BEE which may well prove to be their Achilles heel in the municipal elections in November this year. The electorate is clearly indicating that they prefer the DA’s position. Ramaphosa says, “Now is not the time to abandon BEE” – which clearly defines the differences between the major parties within the GNU.

Aside from these differences, it is apparent that the GNU is working well, steadily implementing reforms which are having a positive impact on the economy. The overseas perception of our political stability has improved as evidenced by the increasing flows of foreign capital into the country. That is having the effect of strengthening the rand, which is in turn causing the inflation rate to fall even further. This is a virtuous cycle of economic improvement and rising living standards.

Economy

The Budget benefited from higher corporate taxes mainly due to the windfall in commodity prices and the lower cost of servicing the government debt. Instead of a R20bn tax increase, consumers will now benefit from tax reductions to accommodate fiscal drag. Importantly, the level of government debt is predicted to continue falling steadily which makes South Africa a less risky option for overseas investors. The budget deficit is expected to decline to as little as 3,1% of gross domestic product (GDP) by the 2028/29 financial year. In our view the Minister of Finance has used the tax overruns and the reduced cost of borrowing very sensibly to further stimulate consumer spending and continue with the government’s debt consolidation program. Mining tax collections rose by almost 30% giving an unexpected windfall to the fiscus – and one which may not last very long. The rand strengthened back below R16 to the US$ showing that the budget had been well-received by the international investment community. GDP is expected to have grown by 1,4% in 2025 and to grow by 1,6% this year and 2% in 2028. Much of that extra growth is expected to come from the government’s plan to spend as much as R1 trillion on infrastructure over the next three years. In our view these growth forecasts may well prove to be conservative. The South African economy has been described as a “light switch” economy – in other words, it is either off or it is on. In our view, this budget signals that it has been turned on again after the long recovery from COVID-19. With lower interest rates, inflation under control and an influx of foreign investment everything looks good for a strong recovery.

The International Monetary Fund (IMF) estimates that the President’s Operation Vulindlela could increase South Africa’s economic productivity by 9% in the medium term at the current pace of reform. Annual gross domestic product (GDP) growth could reach 3% if bottlenecks in logistics, electricity and the water supply are eliminated. The new inflation target of 3% is crucial to this performance with real incomes rising steadily. The level of government debt should also begin falling as tax receipts increase and the interest bill declines. All-in-all the IMF is very positive about the future of the South African economy and sees it catching up to the growth rates of other African and emerging market economies.

The consumer price index (CPI) came in at 3,5% in the year to end-January 2026 – down from December’s 3,6%. In January month it was 0,2% - the same as December. Lower food and fuel prices were the cause. Food inflation came in at 4,4% with cereal inflation down to 0,6%. Maize meal inflation fell by 2,6% - down from December’s figure of 9,5%. Dairy products and eggs were cheaper, but meat prices rose by 13,5%. The price of fuel fell by 3,7% over the year with petrol down 3,1% and diesel down 5,4% over the month. The low level of inflation means that real wages will continue to increase making consumers better off.

The unemployment rate fell in the last quarter of 2025 to 31,4% from the third quarter’s figure of 31,9%. Natal and Gauteng had the worst performance, losing 41000 and 54000 jobs respectively while the Western Cape added 93000 jobs. The Western Cape’s unemployment rate is just 18,1%. At the same time, the Gauteng population is growing by 2% per annum mainly because of illegal immigration. These figures underscore the shift away from the ANC and towards the DA. Almost everyone in South Africa, from the humblest squatter to the wealthiest businessman, understands two indisputable facts about the DA – they are not corrupt and they are very good at service delivery. The ANC is seen as the opposite and is steadily losing support across the country despite is role as the party which brought an end to apartheid.

The South African economy is beginning show signs of real growth and stability. Perhaps the most notable change has been the influx of foreign capital, especially into our bond market where the yield on the 30-year government bond has fallen significantly. The yield is now at about 8,68% having fallen from as high as 12,7% in October 2023. Part of the reason for this is our relatively low level of inflation which means that the real return on our government bonds is very attractive to overseas investors. Other reasons include the fact that the economy is being better managed with the potential for budget surpluses. The cost of borrowing has substantially reduced the government’s interest bill and should make it possible to consolidate government debt even further. The end of loadshedding and the improvement in Transnet’s logistics have helped as has our ratings upgrade by Standard & Poors. Of course, the budget that was tabled by the Minister of Finance in February shows a solid revenue over-run and the impact of that on the government debt. Low inflation has resulted in lower interest rates and hence a smaller debt-servicing cost for government. This combined with higher taxes from mining companies has boosted the budget substantially. In the first three quarters of the financial year, revenues have been running about 10,4% ahead of budget while expenditures have risen only 6% compared to the budgeted figure of 8,3%.

Standard Bank’s chief economist is bullish about the South African economy. He says that the decline in interest rates added to rising real incomes and lower unemployment is creating a positive economic environment. He says that South Africa, having already had one ratings upgrade, could experience more upgrades over the next two years leading ultimately to attaining the coveted “investment grade” status. A major factor has been the development of the government of national unity (GNU) and its relative success in introducing economic reforms. With the municipal elections in November he says the political scenario is likely to become even more fragmented with the smaller parties doubling their representation. Water shortages have replaced loadshedding as the primary concern and impediment to economic growth.

Manufacturing production fell by 1,3% in 2025 according to Stats SA. The only positive contributor was petroleum, chemicals, rubber, and plastics. Negatives were food, cars, and steel products. Obviously, motor vehicle production is being hurt by the surge of Chinese and Indian imports while the steel industry is negatively impacted by the high cost of electricity. In the last quarter of last year production fell by only 0,5%. The mining industry was up 2,5% over the year. Demand for South African products has been affected by increased protectionism worldwide.

The South African economy is vulnerable to shocks coming from inside the country or from outside. In the past our relative political instability and the general mismanagement of our economy has meant that most of those shocks were internal and of our own making. More recently, and especially after the end of loadshedding and the improvements in logistics, most of the threats are external. This is according to the IMF and their latest survey which was conducted in November and December of 2025. The international economy has become more protectionist due to Trump’s imposition of tariffs. The IMF says that the risks to the world economy have diminished since the beginning of the year but remain a potential problem for South Africa. Perhaps the greatest of these is the possibility that commodity prices could decline, which would starve the economy of much-needed foreign exchange and cause a loss of jobs in the mining sector.

Productivity is probably the single most important word in the New South Africa. Without productivity, our gross domestic product falls making everyone worse off. Also, we become less competitive on world markets. Without good productivity there are insufficient funds for government’s social spending programs. The productivity figures published show that in November last year productivity was down across 8 of the 10 divisions measured and that underutilisation has risen to 22,2%. This is not good news for the country and the economy. Notably, the figures for November 2025 only came out in February 2026 which indicates that Stats SA itself does not take this measurement very seriously.

According to Codera Analytics, SA’s productivity since 1990 has been stagnant leading to lower per-capita incomes. The stagnation has been mainly due to state-owned enterprises (SOE) whose performance has declined markedly. Electricity availability and cost have been a major factor. The inflation adjusted value of capital stock has not been growing and the performance of government entities has been inefficient. In 2025 investment in various projects increased by 16% over 2024, but government and Eskom infrastructure projects declined by R320bn. Codera suggests a “...shift back to meritocratic appointments in government” and the privatisation of failing government institutions.

South Africa remains primarily an exporter of raw materials and an importer of finished goods. We export large quantities of precious metals and base metals and minerals and we import manufactured goods. That is how our economy mostly works. The problem is that our policies do not encourage new start-up mining operations with the result that almost no mining exploration has been done for the past decade. It is estimated that, in the New South Africa, as much as 40% of a start-up’s budget is taken up just complying with all the administrative requirements and red tape. The effect is that only between 9% and 14% of the South African land area has been geo-mapped – meaning that there are almost certainly substantial unexploited mining opportunities out there. Small start-up companies are treated the same as the majors, but they do not have the same depth of capital. If we allow our mining to decline through inadequate exploration, in time we will face declining export revenues. We attract less than 1% of global mining exploration spend as it is – which contrasts sharply with other mineral-rich countries like Australia (approx.16%) and Canada (approx. 20%).

Eskom’s continuous and persistent price increases have already endangered South Africa’s smelting industries and our ability to beneficiate metals and minerals mined locally. It has also been making our textile industry uncompetitive. The rising cost of local manufacture has combined with a flood of cheap imported products to make it uneconomic to produce textiles inside South Africa – thus endangering tens of thousands of jobs. Imported clothing is now between 25% and 40% cheaper than that which is locally produced. The high cost of electricity in South Africa is estimated to have cut about 2% off gross domestic product (GDP) growth. Last year alone, manufacturing fell by 1,4% while vehicle and parts production fell sharply in response to cheap imports. Needless to say, the high cost of Eskom’s electricity is forcing businesses and consumers to switch to alternatives like solar power.

Sibanye has become the latest company to expand its use of renewable energy to reduce costs and improve reliability. It has signed a ten-year deal to build a mixture of solar and wind energy to supple 139mw of additional power to its local businesses. This will increase Sibanye’s renewable energy production to 765mw. Sibanye now produces roughly half of its local energy requirements from renewables. The pattern of large energy users like Sibanye moving away from Eskom and building their own supply is what will eventually destroy Eskom completely.

Blutel (BLU) received a licence from the National Energy Regulator (NERSA) to buy and sell power in direct competition with Eskom. This will enable it to make renewable energy contracts with leading municipalities to provide an alternative source of power. Bluetel, through its subsidiary, BluEnergy Trading, already sells power tokens to millions of people across the country so it is in a good position to exploit the licence. Obviously, this is a major step in the effort to break Eskom’s energy monopoly and bring power into the free market.

Water shortages are beginning to become a major problem for businesses across the country, but especially in Gauteng. This appears to be because of a lack of critical expertise on water boards. The Business Day recently reported that its research showed that only 16 out of 78 non-executive directors held engineering degrees and on the average 12-member board there are only 3 engineers. Obviously, qualified, experienced technical experts are needed to evaluate water infrastructure in order to ensure consistent supply. In smaller rural water boards, the lack of skills is even more severe leading to continuous water outages and a crisis management approach.

Seeff Property Group has reported that almost half of all home sales nationally are being executed by first-time buyers. This has obviously come about because of the decline in interest rates and the rising level of real incomes in South Africa. Competition between the banks has kept finance costs on a new mortgage bond tight, increasing affordability. This shows that the economy is recovering on a broad front. For a first-time buyer looking at a property with a value of 1,2m the monthly repayments are about R1200 less than they were when interest rates were at their highest.

Debtbusters, the debt counselling organisation, says that online gambling is very prevalent among people seeking debt counselling. The activity often diverts funds away from essentials like food, rent and debt repayments – and it increases reliance on credit. Consumers are facing high and rising costs. Over the past decade electricity has risen by 165% and fuel by 74%. The accumulated impact of Inflation over the decade is nearly 50%. Those people applying for debt counselling are paying over 70% of their income in interest. Take-home pay has fallen by more than half over the past decade after inflation.

The Rand

The rand is benefiting from a shift in overseas investment sentiment towards risk-on as well as the general perception that South Africa has become more politically stable and is implementing meaningful economic reforms. The currency has broken decisively down through R16 to the US dollar and is consolidating at these new lower levels. Technically, it has been forming a triangle or flag formation between two trendlines. Consider the chart:

This shows that the uncertainty that existed in January 2026 was gradually dissipating. Trump's attack on Iran has caused a sharp upside break, as sentiment shows, to risk off. Emerging currencies are taking a pounding.

In time we are confident that the rand will continue to strengthen. Trump will almost certainly back down in his war against Iran. The US dollar is still weakening, but, as we have pointed out before, the rand has also been strengthening against other hard currencies like the euro and the British pound,

Commodities

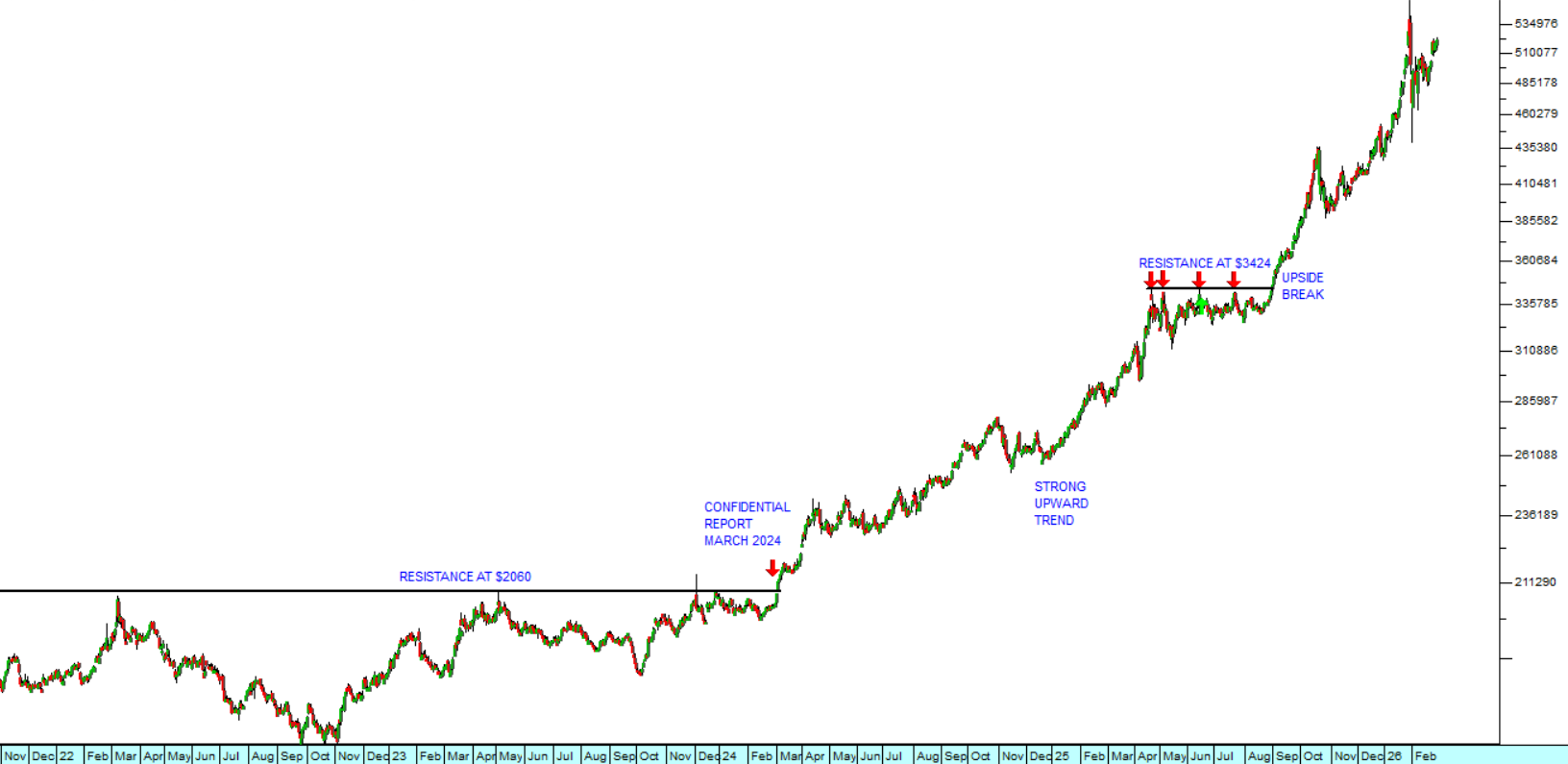

GOLD

Standard Bank is now predicting that the gold price will rise above $6000 per ounce this year and reach $7000 next year. This compares with and comes on top of 2025, when the gold price rose by 64,8%. Consider the chart:

The chart shows that gold broke above $2060 in March 2024 (reported in the Confidential Report of that month) and that since then it has been rising steadily. There was a short period of resistance again at $3424 in the middle of last year, but since the metal has been rising sharply. We expect this trend to continue.

Standard says that the money supply, meaning US dollars in circulation, increased by 50% over the last five years and now that interest rates are coming down gold’s disadvantage in offering no real return is declining. This means that the gold price is playing “catch-up”. The US Federal Reserve Bank’s efforts to reduce the size of its balance sheet by quantitative tightening (Q/T) is not sufficient to stop this process. Central Banks worldwide are buying gold rather than US Treasury Bills because they seem to offer better long-term security. Obviously, if the gold price continues to rise, South African gold mines will continue to produce super-profits and pay increasing taxes which benefits the fiscus and makes our national budgets much easier to balance. Precious metals shares dominate the Winning Shares List (WSL) at the moment and should continue to do so. Pan African’s surge in the last few days has taken its gain since being added to the WSL to above 800%.

The rising gold price reflects the general perception overseas that the US dollar is in decline and that the level of political uncertainty is on the rise. Obviously, developments like the bombing of Iran by Israel and the US add to the level of international uncertainty – making gold even more attractive. In our view, the gold price is likely to continue going up but will certainly experience periodic corrections. It is well to remember that gold does not offer investors any return and is always being measured against the government bonds of first world countries which do offer a return. The fact that investors are willing to forgo that return for gold’s better security speaks volumes about the level of international uncertainty.

OIL

Brent’s rise to above $82 per barrel since the beginning of the year is primarily due to Trump’s war-mongering in the Middle East. Consider the chart:

The recent oil price rise began with the riots in Iran and has escalated into a major threat of war with the bombing of Iran, with Israel capitalising on Trump’s new-found international confidence following the invasion of Venezuela. The US has been building up its military presence in the area, and the two sides are far apart on talks about Tehran’s nuclear program. A number of European countries have urged their citizens to leave Iran as the tensions have increased. The US and Israel previously bombed Iran’s nuclear facilities in June 2025. Trump is under increasing pressure at home from his involvement in the Epstein scandal and immigration activities which have seen him lose some of his MAGA support base. A Middle East war helps to distract people from these negatives. He is very aware that his declining popularity could easily lead to the Republican’s losing both the House and the Senate in November – which would inevitably result in his impeachment and removal.

Companies

The JSE Overall index (J203) rose by 37% in 2025 – adding about R4,7 trillion to its market capitalisation. So, 2025 was an excellent year for those private investors who were fully invested. This rise was partly a result of overseas investment and partly local, but the driving force was the economic reforms which have been implemented since the advent of the government of national unity (GNU). It is not an exaggeration to say that the South African economy is in a recovery phase with the end of loadshedding, rising precious metals prices and falling interest rates. A large portion of the rise in the index has coming from mining companies. Retail shares, like Clicks, Mr Price and Shoprite have been declining. However, we believe that, as real incomes continue to increase due to low inflation, consumer spending will inevitably pick up. In other words, the bull trend is not over.

CAPITEC

We added Capitec to the Winning Shares List (WSL) on 4th November 2023 at a price of 185496c. It closed on Friday last week at 474254c – a gain of 155,7%.

And it continues to perform. In its latest trading statement for the year to 28th February 2026 the company estimates that headline earnings per share (HEPS) will rise by between 20% and 25%. The Business Day suggests that Capitec’s profit will now be close to that of Nedbank – somewhere around R17bn. This milestone is impressive, but still less than half of Standard and FNB’s R40bn. If Capitec keeps growing at this pace it will ultimately become South Africa’s most profitable bank. The bank said,

“Income from value-added services and Capitec Connect continued to grow, supported by sustained growth in client adoption of these offerings. An improvement in the macroeconomic environment contributed to increased lending activity in Personal and Business banking”.

Consider the chart:

In our view, Capitec will continue to be an excellent long-term investment for private investors.

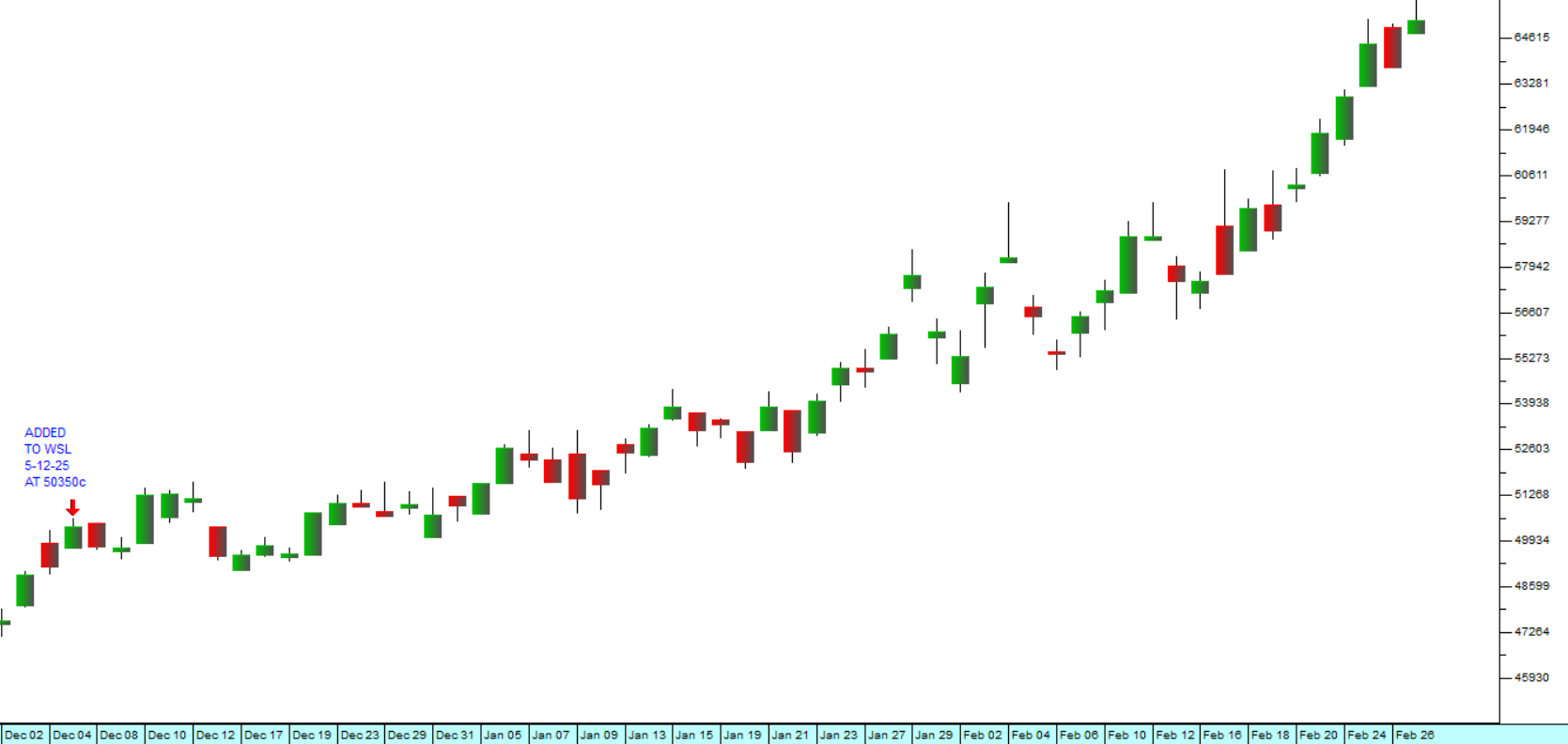

BHP

BHP’ business is about half copper and half iron ore. It is the world’s largest producer of copper and is currently benefiting from the surge in the copper price late last year which has continued this year. The company has copper operations in Chile, Argentina, Arizona and Australia and its production of the metal has increased by about 30% over the past four years.

In the six months to 31st December 2025 the company reported attributable profit of $5,6bn, 28% up on the previous comparable period. Gold and silver are by-products of BHP’s copper production. Production was up 33% and 29% respectively. The company paid out an interim dividend of $3,7bn which equates to 73c (US) per share. Consider the chart:

We added BHP to the Winning Shares List (WSL) quite recently on 5th December last year at a price of 50350c. It has since moved up to its close on Friday last week of 65224c – a gain of 29,5% in just under two months. We believe that it will continue to perform, mainly because of the continued demand for copper.

CLICKS (CLS)

Following up on our article of 26th January 2026 this share continues to be over-sold but has found some support in the range between its low of 31000c made on 26th January 2026 and about 31800c. It is in the process of forming an “island”. This type of formation is typical of the “bottom of the market” and usually occurs when the smart money begins getting back into a share after a significant fall. It is roughly in line with the intraday low of 31382c made on 7th April 2025 and the intraday cyclical highs made in early 2024. In our view, it is quite possible that Clicks has now passed its cycle low and is preparing for a new upward trend. Consider the chart:

Then on Tuesday the 3rd of March 2026, Clicks broke down sharply, through that resistance line, to a new low at 29922c. This was a direct result of Trump's Iran war. As a private investor you should definitely watching this share closely now. It is certainly oversold. The only real question now, is how much further it can fall before it begins to go up again?

It is notable that on 9th February 2026, that Clicks announced that Black Rock Inc. – the largest asset manager in the world with roughly $12,5 trillion in assets under management (AUM) – had increased its stake in Clicks to above 5% of the issued share capital. This shows that the Click’s oversold position is beginning to attract the attention of overseas institutional investors.

We believe that this share should be accumulated on exactly the type of weakness that it is currently showing.

REDEFINE (RDF)

Redefine is one of South Africa’s largest and oldest property listed companies (REIT). Prior to the outbreak of COVID-19 at start of 2020, Redefine was an institutional “darling” and its shares reached a high of 1198c on 20th April 2018. The, like all property companies it took a significant hit as the effects of the pandemic became apparent. Its shares eventually reached an intraday low of 139c on 24th March 2020.

From this point began a slow and volatile recovery characterised by an extended, 4-year period of sideways movement. The sideways market came to an end in the second half of last year and we added it to the Winning Shares List (WSL) on 18th July 2025 at a price of 480c. Since then, it has climbed to 693c – a gain of 44,4% in just over 7 months. Consider the chart:

In a pre-close presentation on 24th February 2026 the company’s CEO, Andrew Konig, said that the company was entering 2026 in the strongest position it had been in since the pandemic due to “...stabilised vacancy rates, strong retail and industrial rental growth, and increased business confidence”.

We believe that this share will return to its former glory and institutional patronage.

DISCOVERY (DSY)

This is one of South Africa’s leading financial services companies. Beginning in medical insurance, it has now moved into banking and a growing range of other financial products. It has also ventured overseas to become a significant international organisation. Consider the chart:

In early 2024, Discovery shares displayed a classic “reverse head-and-shoulders” formation. This is quite an unusual formation which normally signals the beginning of a new upward trend. We eventually added the share to the Winning Shares List (WSL) on 1st August 2024 at a price of 14280c. It has since climbed to 26136c (Friday last week) – a gain of 83% in just under 18 months.

Its recent trading statement for the six months to 31st December 2025 indicates that the company is expecting headline earnings to rise by between 27% and 32%. This is massive increase for such a large company, and the announcement caused the share price to climb 7,6% in a single day.

We believe that Discovery should be part of every private investor’s portfolio and should be accumulated on any weakness.

← Back to Articles