Market Overview

15 November 2020 By PDSNETNow that the uncertainty of the US election is essentially over, it is perhaps a good time to step back and consider where we are and what is likely to happen next.

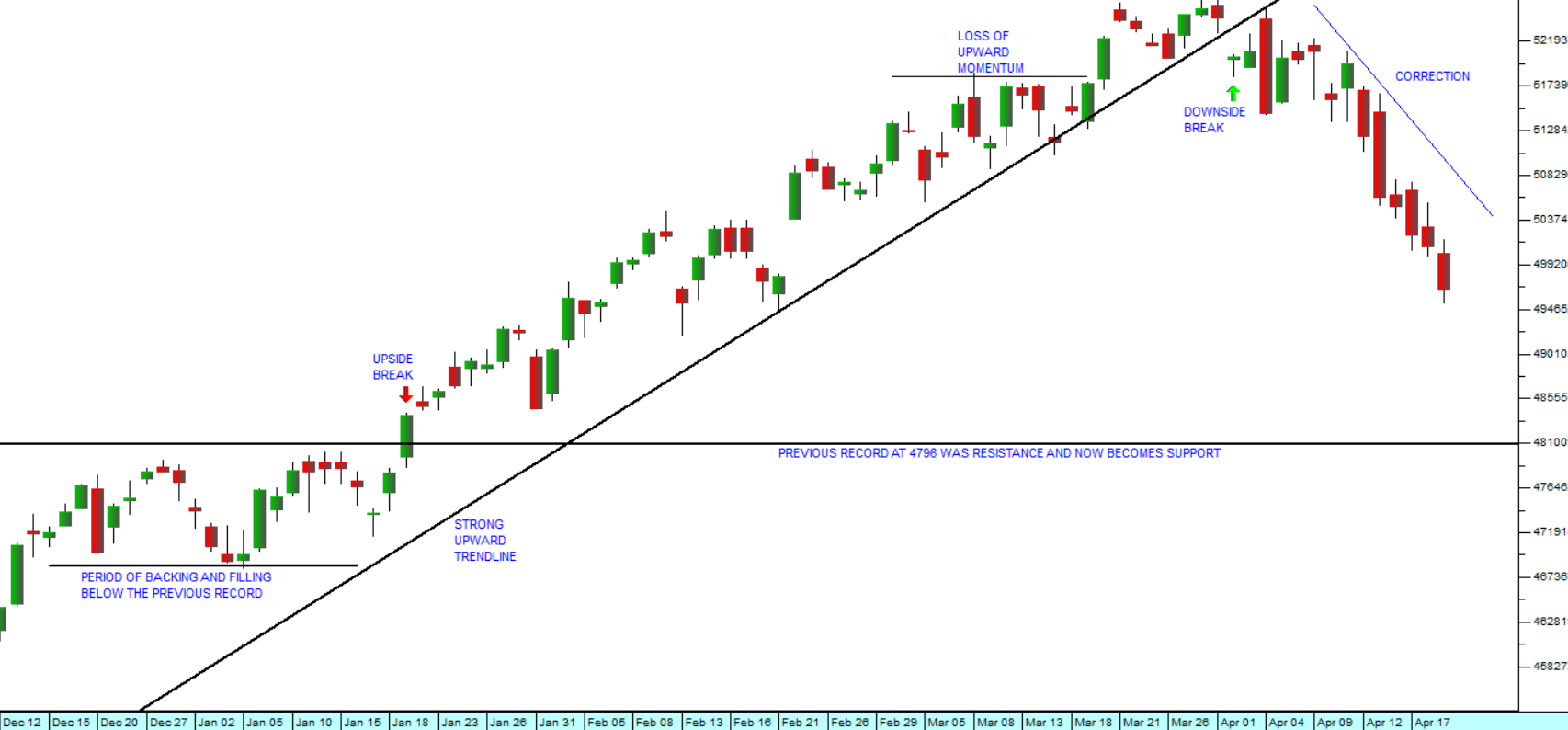

The S&P500 index, which is an excellent benchmark for trends in the international markets, appears to be breaking to a new record high – above the resistance at 3580. Consider the chart:

You can see here the downward spike caused by the pandemic which was followed by a rapid recovery to a new all-time record high at 3580. Notably, the downward spike caused by COVID-19 was not sufficient to cause the 200-day moving average to turn down significantly – a clear indication that the long-term bull trend was still intact.

The uncertainty around the US election and the second wave of COVID-19 in some first world countries has temporarily arrested the upward momentum and held the market in a sideways pattern between support at 3225 and resistance at 3580 since September 2020. On Friday (13-11-20) the market closed just above that resistance level and now looks set to begin a new upward trend. Obviously, investors are encouraged by the prospect of the second $2,4 trillion stimulatory package and the apparent imminent availability of a vaccine.

Our view has always been that the COVID-19 downward spike in markets was a technical aberration resulting from a “black swan” event. That event temporarily interrupted world economic growth, but was and remains completely unrelated to the underlying growth trends in the world economy. Now that investors are becoming confident that the pandemic is almost behind us and the uncertainties surrounding the US election are fading, they are driving markets upwards to new highs in anticipation of further stimulus.

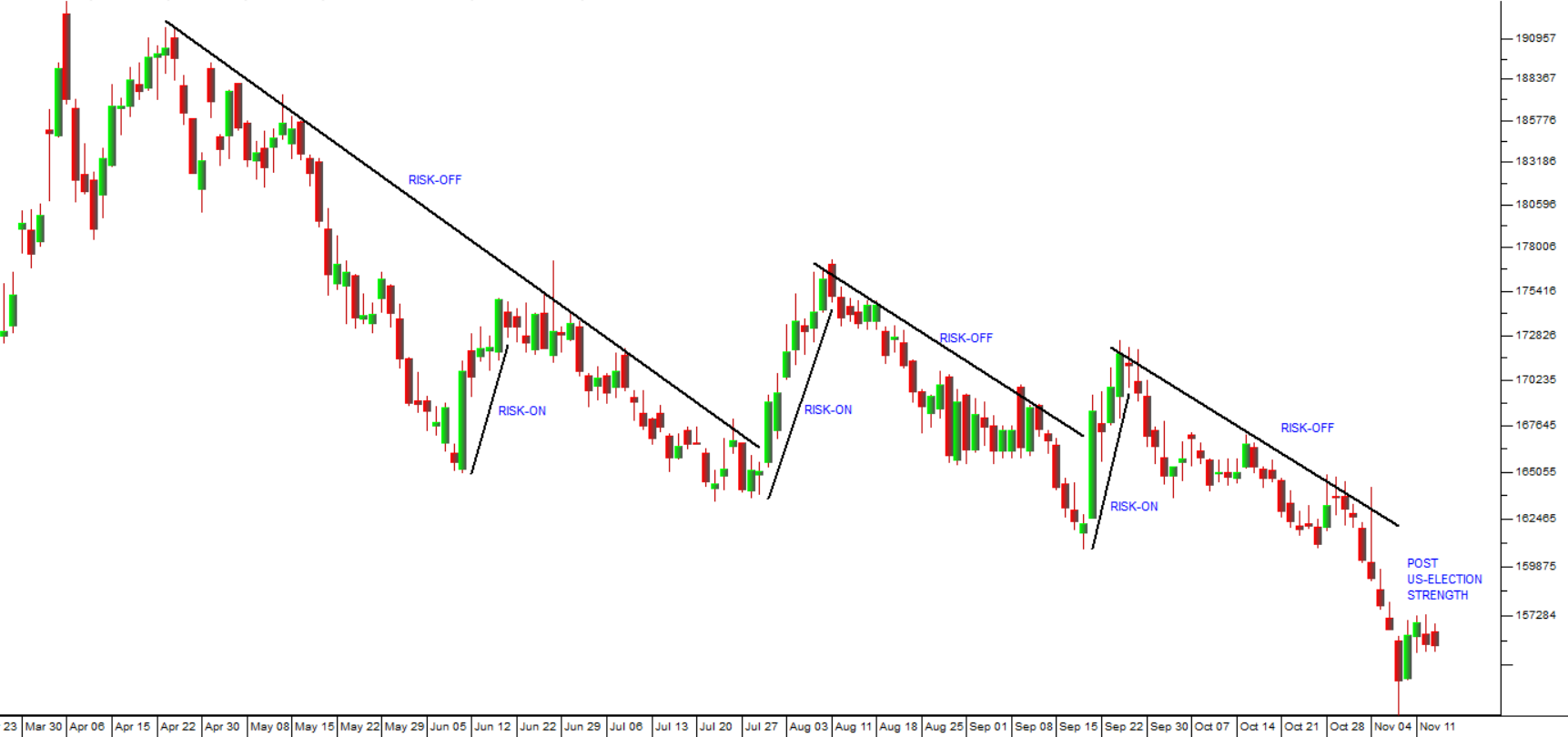

The impact of this on the JSE is obvious. International investors are rapidly shifting from a mood of “risk-off” to “risk-on” – which is making our high-yielding government bonds very attractive. This, in turn, is driving the undervalued rand upwards against the US dollar as overseas funds pour into the country. Consider the chart:

We have long believed that the rand was materially undervalued against hard currencies and that continued strength was likely. We see the rand continuing to gain ground against first world currencies. This is combining with the weakening oil price should portend a significant drop in petrol prices in South Africa in the coming months.

As a private investor you should be aware that time is running out to buy those high-quality blue-chip shares which are still trading at significant discounts. The strength of the rand will make the traditional rand-hedge shares less attractive and companies with a locally based income more attractive. The expected drop in fuel prices will add to other local stimulatory measures to help the recovery of the economy. It will also increase the downward pressure on the inflation rate making further monetary policy options possible.

Our view remains that the South African economy will recover more rapidly from the pandemic than most economists are expecting.

DISCLAIMER

All information and data contained within the PDSnet Articles is for informational purposes only. PDSnet makes no representations as to the accuracy, completeness, suitability, or validity, of any information, and shall not be liable for any errors, omissions, or any losses, injuries, or damages arising from its display or use. Information in the PDSnet Articles are based on the author’s opinion and experience and should not be considered professional financial investment advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional. Thoughts and opinions will also change from time to time as more information is accumulated. PDSnet reserves the right to delete any comment or opinion for any reason.

Share this article: