The Debtors' Book

A BIT OF HISTORY

Many years ago, in 1982 when I started this business (which became “PDSnet”), I ran advertisements in both the Rand Daily Mail (RDM) and in the Star – which were the two most widely read newspapers in Johannesburg at the time. At that time, we were a very small business and had no credit rating at all. Despite this the RDM immediately

WeBuyCars - Results

The financial results of companies show how profitable they are and give a good indication of their share’s risk and potential return. WeBuyCars (WBC) is a recent listing which came to the JSE on the 11th of April 2024. Unlike other listed motor vehicle companies, it is a company which specialises in the purchase and sale

Choosing Winners

We are often asked how we go about selecting the shares to put on to the Winning Shares List (WSL). Right now, there are 102 shares on the list with 5 having gone down since they were added, 94 are up and 3 are unchanged. On an annualised basis, 24 of them are performing at above 100% per annum.

As a private investor,

Kore Revisited

Kore (KP2) remains at once the most exciting and most risky investment on our Winning Shares List (WSL) at the moment. We originally added it to the list just over a year ago on 16th May 2024 at a price of 20c. It subsequently rose to a high of 83c on 3rd October 2024 and we published an article

Rand Strength 2025

The strength of the rand is both a critical and a complex issue for private investors on the JSE. Our currency is influenced by two primary forces:

- Our local economy’s prospects

- The rand’s role as a leading emerging market currency

These, in turn, are

Sibanye Revisited

In these uncertain times, when nobody really knows to what extent Trump will back down on the international trade war which he has initiated, many investors are moving into precious metals as a hedge against the weakness of paper currencies (especially the US dollar) and paper assets like equities and bonds.

The problem

Smart Local Investors

The last two months have been wild on the markets – mainly because of Trump’s ill-advised, on-again, off-again tariff policies. The issue now is:

Will this morph into a full-blown bear trend? Or is this correction almost over?

From his election victory on the 6th of November 2024,

Jerome Powell

The Federal Reserve Bank (“the Fed”) is completely outside the control of the President and Executive Branch of the US government. The chairman of the Fed is appointed for a renewable 4-year term by the President. The President cannot remove the Chair without cause. The current chairman, Jerome Powell was appointed by Trump during his first term as President and reappointed by

Uncertainty Soars

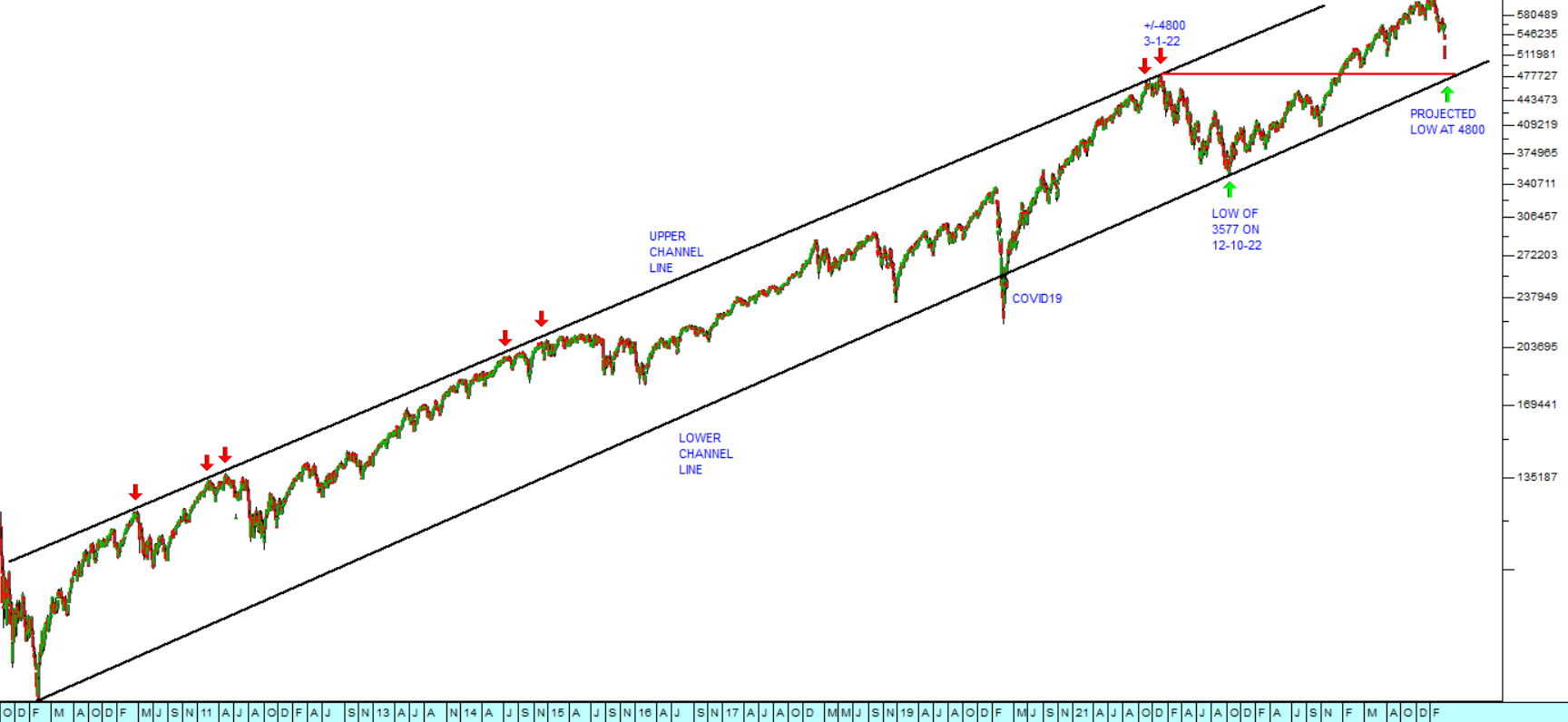

Investors are by their very nature risk takers, but they are always trying to reduce the risk which they have to take to a minimum. Donald Trump, with his threat of an international trade war and his on-again, off-again tariffs has significantly increased the level of risk in markets across the world. This can be seen in the extraordinary volatility in the S&P500

Liberation Day

Trump has done the unthinkable. He has deliberately engineered the collapse of the US and world stock markets in the nonsensical belief that somehow an international trade war will make Americans richer. Nothing could be further from the truth. His actions have taken the S&P down from its all-time record high of 6144.15 on 19th February 2025 to Friday’s